Dechra Pharmaceuticals have now released their interim results for the year ending 2018.

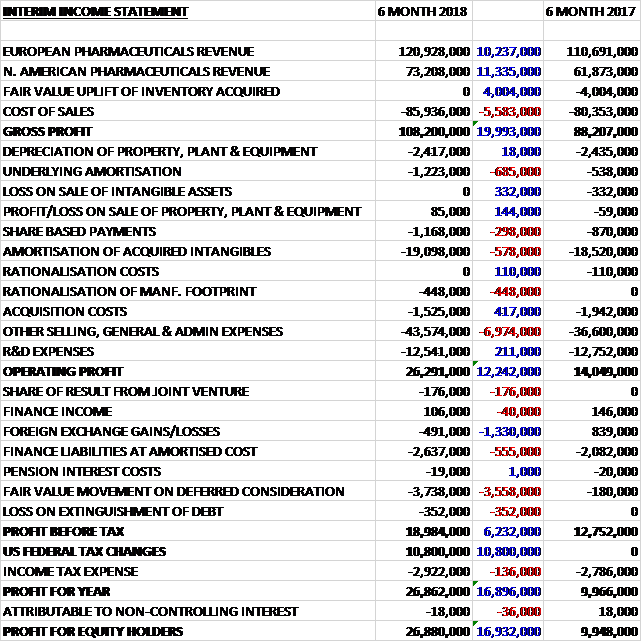

Revenues increased when compared to the first half of last year with an £11.3M growth in North American sales and a £10.2M increase in European sales. Cost of sales increased by £5.6M but there was no fair value uplift of inventories acquired which cost £4M last time. This meant that the gross profit was £20M higher. There was a £685K increase in underlying amortisation, a £578K increase in the amortisation of acquired intangibles and a £6.9M growth in other general costs to give an operating profit £12.2M higher. We then see a £1.3M detrimental movement to a forex loss and a £3.6M fair value movement on the deferred consideration to give a pre-tax profit £6.2M higher. There was a £10.8M one-off gain from the US tax changes which meant that the profit for the period was £26.9M, a growth of £16.9M year on year.

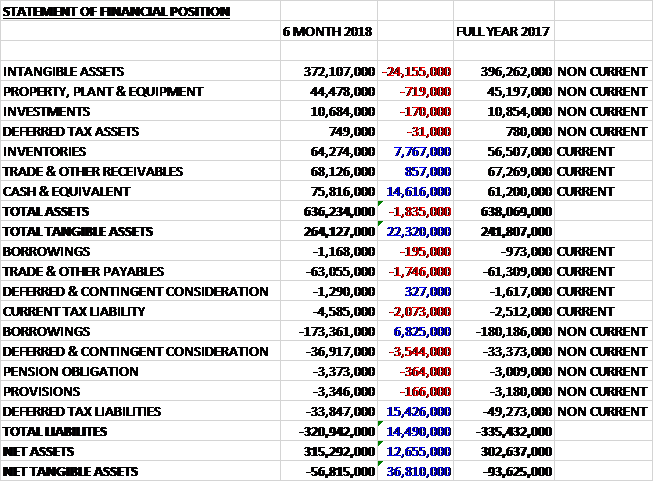

When compared to the end point of last year, total assets decreased by £1.8M, driven by a £24.2M fall in intangible assets, partially offset by a £14.6M growth in cash and a £7.8M increase in inventories. Total liabilities also declined during the period was a £3.2M growth in deferred consideration, a £2.1M increase in current tax liabilities and a £1.7M growth in payables was more than offset by a £15.4M decrease in deferred tax liabilities and a £6.6M reduction in borrowings. The end result was a net tangible asset level of -£56.8M, a growth of £36.8M over the past six months.

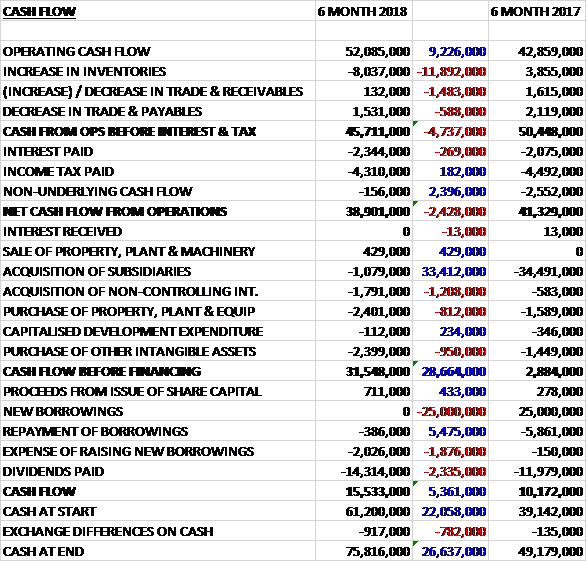

Before movements in working capital, cash profits increased by £9.2M to £52.1M. There was a cash outflow from working capital due to an increase in inventories and despite a £2.4M reduction in the non-underlying cash outflow, there was a net cash flow from operations of £38.9M, a decline of £2.4M year on year. The group spent £1.1M on acquisitions, £1.8M on non-controlling interests, £2.4M on fixed assets and £2.4M on intangible assets to give a free cash flow of £31.5M. They also spent £14.3M on dividends and £2M on raising new borrowings to give a cash flow for the period of £15.5M and a cash level of £75.8M at the period-end.

All product categories delivered growth at constant exchange rates. Companion animal revenue was up 18%, equine increased by 19%, food producing animals revenue was up 3% and nutrition also increased by 3%.

The operating profit in the European pharmaceuticals business was £34.2M, a growth of £3.4M year on year. Treating Apex on a like for like basis, at constant currency, the increase was £1M. CAP continued to be the main growth driver with sales increasing in all of the focus therapy areas. They have delivered FAP revenue growth of 3.7% in a market still experiencing pressure to reduce antibiotic usage. Nutrition is recovering with a growth of 3% following the resolution of historic supply and palatability problems, and is in the process of being relaunched with new packaging and improved palatability. Despite the increasing market penetration of Osphos, equine sales were down 4.3% due to generic competition to Equipalazone.

The operating profit in the North American pharmaceuticals business was £25.5M, an increase of £7.4M when compared to the first half of last year despite distributors selling white label goods to compete with Carprovet and the fact that trading was disrupted by two hurricanes. There was good growth from CAP and equine, with the latter mainly from Osphos. These are the only two areas the group is active in the region. Investment continues to be made in the US sales team where they have increased the reporting regions from four to six, adding two regional managers.

Several new product registrations were achieved in the period. In European FAP, registrations included Solacyl Water Soluble Powder, a line extension of an existing product for turkeys; Diatrim, an antibiotic for cattle mastitis; and Avishield IBH120, their second EU-registered poultry vaccine developed in Croatia. Numerous international registrations were also achieved, including products for New Zealand, Thailand, Kazakhstan and Australia.

In North America they have extended the range of their Vetivex critical care fluids and have launched all dosage sizes of AmoiClav tablets. In Mexico they have launched Osphos, Vetoryl, Cyclospray and several products from their dermatology range. In addition, they have acquired the following new products from licensing deals: Redonyl Ultra, a dermatology supplement from Premune; Vetradent, a water additive to combat biofilms from Kane Biotech; and Bioequine, an equine herpes vaccine from Bioveta. They also continue to work with Animal Ethics to accelerate the global registration of Tri-Solfen.

During the period there was the inclusion of an exceptional tax credit of £10.8M which arose as a consequence of the reduction in the US federal tax rate.

In December the group acquired RxVet, a sales and distribution business based in New Zealand. The total consideration was £333K and the acquisition generated goodwill of £57K. The business contributed a loss of £5K since acquisition but had it been part of the group for the whole period, it would have contributed profits of £51K. The business has been the Dechra distributor in New Zealand since 2010.

In February, after the period-end, the group acquired AST Farma and Le Vet for a total consideration of €340M funded through a placing of 5,121,952 new shares to institutional investors, the issue of 3,670,625 new shares to the vendors and a drawdown of €150M under a new banking facility. AST Farma strengthens the group’s position in the Dutch market and provides them with a direct to vet relationship with the potential to increase sales of their existing brands. Le Vet strengthens their product portfolio across Europe with 60 generic registrations that can be sold through existing networks. The initial phase of integration is progressing to plan.

Going forward, current trading continues in line with management expectations and the initial phase of integration of the AST Farma/Le Vet acquisition is progressing well. Competition from US distributors private label products has increased and they continue to experience direct competition on a number of products in the European portfolio. Despite this, the board are confident of meeting their expectations for the year.

After a 20% increase in the interim dividend, the shares are yielding 0.8% which increases to 0.9% on the full year consensus forecast. At the current share price the shares are trading on a PE ratio of 100.2 which decreases to 36.8 on the full year forecast. At the period-end the group had a net debt position 98.7M compared to £120M at the year-end.

Overall then this has been a good half year for the group. Profits increased, as did net tangible assets, although they were still negative. The operating cash flow deteriorated somewhat but this was due to working capital movements and the cash profit increased with a decent amount of free cash being generated. The North American division performed very well, but there is more competition from white label products; and the European division put in a solid performance, although equine products saw a decline due to generic competition.

The big event after the period-end was the acquisition of Le Vet and AST Farma which seems to be integrating well. All of this good performance is in the share price though and a forward PE of 36.8 and yield of 0.9% makes the shares look rather expensive. Nonetheless I continue to hold.

On the 10th July the group released a trading update covering the year as a whole which was in line with management expectations. Reported group revenue was up 14% at constant exchange rates. European pharmaceuticals was up 11% (4% on an organic basis) and North American pharmaceuticals increased by 18%. This has been driven from the core portfolio, good market penetration and recent pipeline launches. In addition the acquisition of the AST Farma, Le Vet and RxVet businesses have all grown strongly in the year since acquisition.