Circle Oil is incorporated in Ireland and is involved in oil and gas exploration, development and production in the MENA region. It sells oil and gas to the government in Egypt and sells gas to a small number of industrial customers in Morocco. It is listed on the AIM market and they have now released their final results for the year ending 2013.

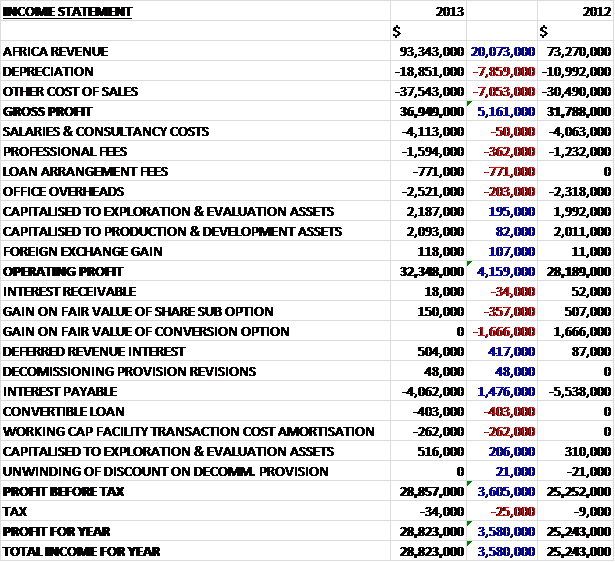

All revenues are currently made in North Africa and during the year they increased by $20.1M as the volume of both oil and gas sales increased along with increased prices achieved for gas sales in Morocco. Cost of sales and depreciation also increased to make gross profit some $5.2M higher than last year. Operating and admin costs increased, predominantly due to a $771K loan arrangement fee with smaller increases in professional fees and salaries, so that operating profit was $32.3M, a growth of $4.2M. The major change in finance costs was a $1.5M fall in interest payable offset by the lack of a $1.7M gain in the fair value of the conversion option and tax during the year was minimal so the overall profit for the year was $3.6M higher than 2012 at $28.8M.

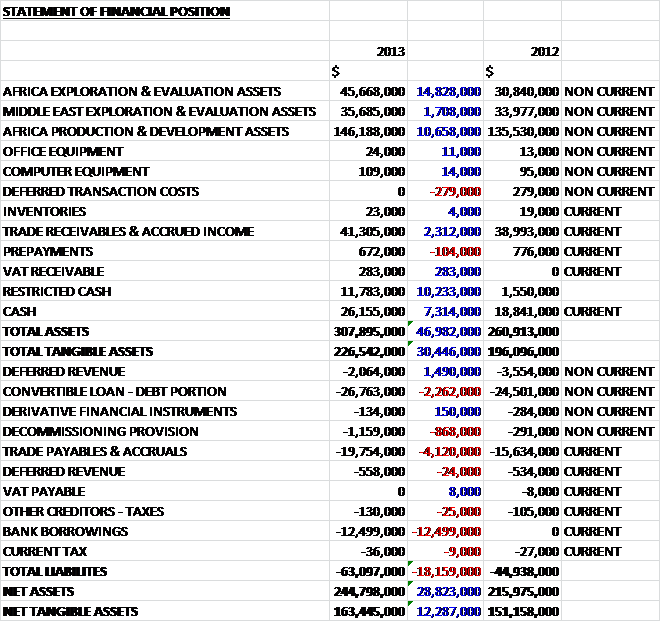

When compared to the end point of last year, total assets increased by $47M. The growth was driven by an increase in cash, with restricted cash up $10.2M and non-restricted cash up $7.3M; a $16.5M growth in exploration and evaluation assets; and a $10.7M increase in production and development assets relating to well appraisal and development costs at the NW Gemsa concession in Egypt and the Sebou Permit in Morocco. Liabilities also increased due to a $12.5M hike in bank borrowings, a $4.1M increase in trade payables & accruals and a $2.3M growth in the debt portion of the convertible loan. The overall result was a $12.3M increase in net tangible assets to $163.4M and I have to say that the balance sheet looks fairly strong here.

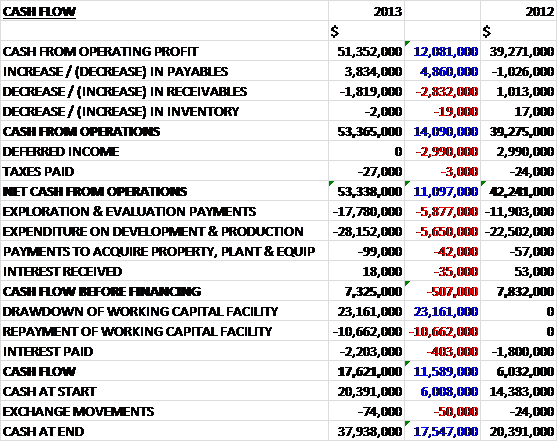

Before movements in working capital, cash profits were $12.1M higher at $51.4M before an increase in payables improved this to $53.4M, a growth of $14.1M. After the negligible tax, the net cash from operations was $53.3M, an increase of $11.1M on 2012 which seems like a good result. The bulk of this cash was spent on exploration and development costs with $17.8M and $28.2M respectively on each. This still left a free cash flow of $7.3M, slightly less than last year due to the higher capital expenditure. After interest was paid, the cash flow was still positive but a big drawdown on the working capital facility meant that the cash inflow for the year was $17.6M.

In Morocco, gas production averaged 1,069 bopd during the year and the group supplied three companies in the Kenitra industrial zone. Preparation for a twelve well drilling campaign for the Sebou and Lalla Mimouna permits continued with the wells being planned with the purpose of confirming the viability of additional reserves and increasing the gas production supplies. The most recent CPR completed by Bayphase in the Sebou concession suggests a 2P Gross Remaining Reserves pf 2.98 MMboe net to Circle and 4.72 MMboe of 3P Remaining Reserves net to the group. At the Sebou concession, they have a 75% controlling interest with ONHYM, the Moroccan state oil company having the remaining 25% share. At the Oulad N’zala concession, Circle has a 60% share with ONHYM having the rest. Both concessions include the right of conversion to a product license of 25 years, plus extensions in the event of a commercial discovery.

In Egypt the NW Gemsa concession contains the Al Amir SE and Geyad fields where production averaged 10,443 bopd and 11.4 MMScf/d during the year. Development drilling continued throughout the period with six producers and one injector in Al Amir and one exploration well, Shebab-2X. The completion of the new gas export line from the Al Amir facilities to the SUCO terminal Zeit Bay is helping the export of current production and the extraction and sale of condensate and LPG is providing further income. Five infill production wells were successfully drilled and completed during the year as well as the AASE-16 water injection well to complete the initial development plan for the field. The Shebab-2 exploration well was drilled in 2013 to test an uppdip exposure from the Shebab-1 well but the target Kareem sands were found to be water bearing. The well did encounter a potential gas bearing interval in the upper Rudeis limestones but a hydraulic fracturation was unsuccessful with no flow to surface and the well has now been temporarily abandoned.

Gas production through the pipeline from the Al Amir facilities to the SUCO terminal started up in February and gas processing is providing an additional two tonnes per MMscf of LPG and 9 barrels of condensate per MMscf. The most recent CPR estimates suggest that the NW Gemsa Concession 2P estimated ultimate recovery is 18.29 MMBoe of oil and raw gas net to Circle and following this year’s production, the gross remaining reserves are estimated to be 29.75 MMboe, of which 11.9 MMBoe is net to Circle. The same report estimated that 3P remaining reserves net to the group was 19.73 MMBoe.

During the year, the group significantly increased its asset base in Tunisia. As well as participation in the Ras Marmour block, they have obtained a 100% share of the Mahdia block and have farmed into the Beni Khaled block to earn an initial 30% interest. In addition, the company has also been awarded the Takelsa permit with a 100% interest. Activity during the year involved seismic survey planning, acquisition and interpretation plus well location and rig planning. Over the Mahdia permit, interpretation of the seismic data meant that the El Mediouni prospect was fully delineated as the drilling target and a rig was contracted to be able to drill the commitment well in Q2 2014. The prospect has numerous fields and discoveries in proximity so this should be an interesting drill. The permit only runs until July 2014, however, after a year extension was granted. The group have now applied for a further six month extension to complete their understanding of the well results.

The Ras Marmour permit in the SE of Tunisia is located in an area with several on shore oil fields. The group owns a 23% interest and the operator is Exxoil. A well is planned to be drilled in 2014 on a nearby prospect but the Ras Marmour partners are still awaiting the final drilling permit with little prospect of much changing despite some site visits from the relevant authorities. The Grombalia permit was awarded to Circle during the year and the board see this as a key award towards increasing the value of the company. The license area includes existing oil and gas field concessions and other discoveries within or close to the block and planning for the first exploration phase of three years of work commitments is in progress, including the drilling of four exploration wells.

At Beni Khaled, the group has acquired a 30% farm in interest in exchange for funding a 50 square km 3D seismic programme and one well, which is expected to cost about $5M. The agreement allows Circle to increase its share to 50% in two equal stages by funding one well in each stage. The farm in will be funded from existing cash flow and Exxoil will continue as operator. The license currently produces about 80 to 100 bopd of light oil from one well and contains additional possible fault bounded extensions to the oilfield itself. The well has so far produced 1.2 MMbo and estimates suggest it now has just 0.25 to 0.5 MMbo remaining to be produced. The licence itself has a remaining term of 19 years so there is plenty of headroom in that respect. The license also contains well BDR-1, the undeveloped Bir rassen discovery which in tests in the early 90s flowed at a rate of 23.5 MMscf/d of gas and 28 bocd. Initial estimates indicate most likely recoverable resources from the Bir Drassen discovery of 47 to 50 bcf of gas and 6 MMbo of oil. Additionally there are also two further undrilled leads that have been identified within the license to be confirmed by the seismic survey.

In Oman, the group acquired additional 2D seismic which has now been interpreted alongside an earlier 3D survey to define a drillable prospect in the SE part of the Block 49 permit and planning is underway to drill an exploration well in the prospect in the second half of next year. Additionally, a further seismic survey was conducted offshore block 52 and the results are now being interpreted with the farm out process still continuing with the objective of finding a partner to drill an exploration well.

In summary then, the group has continued the appraisal and development of the NW Gemsa fields in Egypt and the gas export line continues to supply gas to industries in Kenitra. In addition, the new gas export line in Egypt from the Al Amir facility to the SUCO terminal was completed with gas production starting in February. The 2014 CPR shows little change from the 2013 values in Morocco and the Egypt estimated ultimate recoverable resources showed a slight increase due to a small deepening of the AASE oil-water contact from additional well data. In Morocco, more wells are being drilled to grow the reserves base by adding additional gas discoveries through the third drilling campaign in 2014 and beyond.

Oil exploration efforts continued in Tunisia with the interpretation of the Mahdia 3D seismic and the well proposal for the offshore El Mediouni prospect which has recently spudded. This is a large prospect with game changing potential. Planning of a new 3D seismic acquisition over the newly farmed in Beni Khaled block is advancing. In Oman, a commitment well on onshore block 49 is being planned for 2014 and at offshore block 52, three sizeable leads were identified in the shallow water area on the existing seismic with a re-invigorated farm out process being started. The group achieved an average price for oil of $104.40 per barrel in Egypt, a small decline on the $107.37 achieved last year. In Morocco, the average gas price achieved was $10.34 per Mscf against $9.40 in 2012.

At the end of last year the group agreed a $12.5M secured revolving working capital facility with Ahli United Bank Egypt which has a two year term. The facility attracts interest at LIBOR plus 4.25% which doesn’t sound particularly cheap and is used to fund ongoing expenditure in respect of the NW Gemsa Concession in Egypt. The $11M of restricted cash relates to repayments due under this facility.

As far as risks are concerned, these are similar to most oil explorers and producers. Working in North Africa comes with considerable political risk, particularly in Egypt where the majority of the group’s oil is sold to the government. Well over half of receivables are past their due date with over a third over 120 days late, the vast bulk of which is due from EGPC in Egypt. Payments have been received over the past year and the board believe the money will be received but having so much of the group’s receivables overdue by such a degree from the Egyptian government is a clear potential risk. The group is also susceptible to exchange rate risk and a 5% fall in the USD against the Euro, Sterling and the Moroccan Dirham would reduce profits by $429K with the reverse also being true.

During the year the group appointed Steve Jenkins as chairman after Thomas Anderson stepped down after 10 years in the role. It should be noted that the largest shareholder of the company, with 17.75% of the total issued capital, is Libya Oil Holdings. After the revolution there, this holding has been frozen, what will happen to it is anyone’s guess.

At the current share price the shares trade on a rather ridiculous P/E ratio of 3.8 which increases to a similarly cheap 4.3 on next year’s forecasted earnings. Overall then, this seems like a good update from a decent small oil producer. Profits were up, there is a strong and improving balance sheet and the company is free cash flow positive. There seems some potential for uplift through increased reserves in Morocco and the board certainly seem to see Tunisia as having good potential. I have been burned by companies like this before though, and the unstable situation in Egypt, including the late payments from the Egyptian government is just enough to keep me out of the shares for now. I will keep a keen watch, though.