Circle Oil has now released its interim results for the year ending 2014.

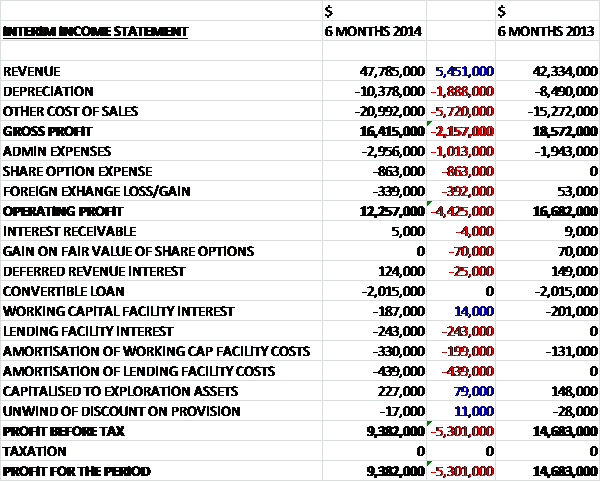

When compared to the first half of last year, revenue was some $5.5M higher at $47.8M consisting of $37M in Egyptian oil sales, $1.4M in gas sales in Egypt and $9.4M in Moroccan gas sales with the increase coming from an increase in the volume of oil sold in Egypt, but a $1.9M increase in depreciation and a $5.7M growth in cost of sales meant that gross profits were $2.2M lower than last time. Admin expenses also increased, primarily due to the drilling activity in Tunisia and there was a one-off share option charge so that operating profit, at $12.3M, was some $4.4M lower than in the same period of last year. Finance costs also increased, mainly due to amortisation of various borrowing costs and with no tax charges, the profit for the period fell $5.3M to $9.4M.

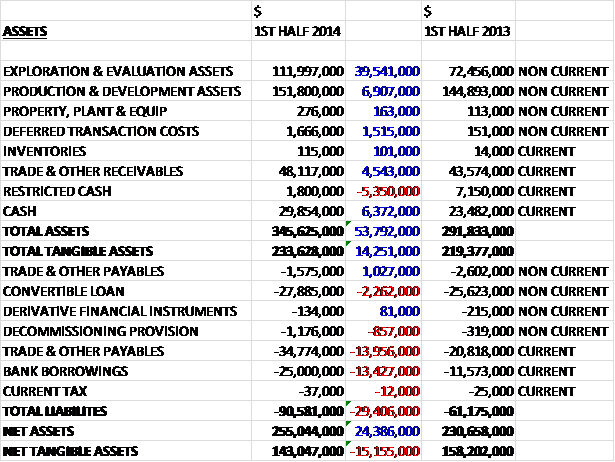

When compared to the half year point of 2013, total assets increased by $53.8M, driven by a $39.5M hike in exploration assets, a $6.9M growth in production assets, a $6.4M increase in cash levels and a $4.5M increase in receivables, somewhat offset by a $5.4M decline in restricted cash. Liabilities also increased over the year due to a $13M growth in payables, a $13.4M increase in borrowings and a $2.3M increase in the convertible loan. Due to the fact that most of the increase in assets came from the intangible exploration assets, net tangible assets fell by $15.2M but the balance sheet still looks rather strong.

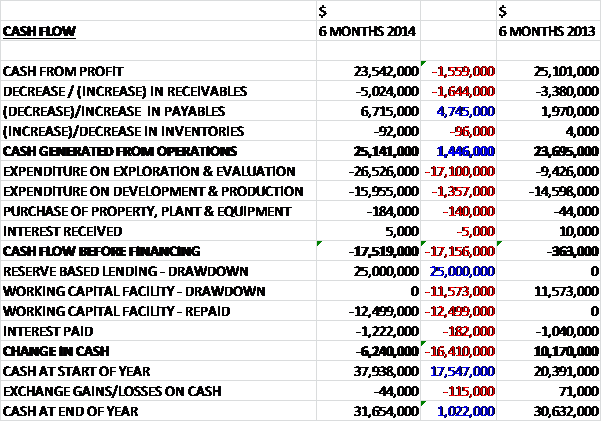

Before movements in working capital, cash profits fell by $1.6M to $23.5M but an increase in payables meant that cash generated from operations actually increased by $1.5M at $25.1M. All of this cash was then spent on exploration and evaluation with an extra $16M spent on development and production. There was a new $25M drawdown on a reserve based lending facility which meant the group could pay back the $12.5M working capital facility and cover the development expenditure. The end result was a $6.2M cash outflow which meant that cash levels at the end of the year were $31.7M.

In Morocco several potential drilling locations in both the Sebou and Lalla Mimouna permits have been delineated using the available seismic coverage. Drilling activity started in the Sebou permit with the SAH-W1 well in May but the rig had to be released to another operator before the well could be fully tested, which is a bit of an oversight but wireline logging confirmed the presence of three gas bearing zones that will be tested for production during the continuation of the drilling programme later in the year. The second well (CGD-12) was spud in August with a further six wells to follow in Lalla Mimouna over the next year.

The daily production rate in Sebou averaged between 6.8 and 7 MMscf during the first half of the year and negotiations are underway for further off-take by the year end. The 2014 CPR reserves estimate the 2P value of gross initial gas reserves in Sebou and Oulad N’Zala was 30.2bef with 22.33bef net to Circle. After the half year production was taken into account, the 2P gross remaining reserves were estimated to be 23.9bef which, current drilling campaign to enlarge the reserve base not-withstanding, seems to suggest only two years of reserves left.

In Egypt at the Al Amir SE field there were ten wells in production with a further two in the Geyaf field with a combined gross production rate of 11,592 boepd and water injection through five of the wells maximised production efficiency and maintained levels. The appraisal well AASE-19, production well AASE-21 and water injection well AASE-22 were successfully drilled during the period and a work over programme was initiated to follow on from the drilling campaign. The export gas line to the SUCO facility is currently flowing at 10 MMscf per day with valuable condensate and natural gas liquids being stripped out and sold to EGPC with average rates of 100 bbls of condensate and 20 tonnes of LPG. The latest reserve estimates in the NW Gemsa showed gross initial oil reserves of 38.3 MMbo and 2P gross initial raw gas reserves of 43.14 bcf which totals 2P gross initial reserves of 45.73 MMboe, 18.29 MMboe net to the group. Following production during the period the gross remaining reserves are estimated to be 22.72 MMbo which seems to suggest the present reserves will not last that long.

In Tunisia the group drilled the EMD-1 well in the North Central area of the Mahdia permit in a water depth of 240m, 120km east of Sousse. It was drilled to a TD of 1,200 metres in the upper Ketatna carbonates. The well discovered very good light oil shows in the lower Birsa carbonate primary target and the upper Ketatna carbonate secondary target over a combined interval of 133 metres. These oil shows confirm the existence of a working petroleum system in the Mahdia permit. The gross oil zone interval in the Lower Birsa is 77 metres and the Upper Ketatna has a minimum interval of 48 metres, subject to confirmation. Using known reservoir and fluid parameters from equivalent formations in the Gulf of Hammamet, the most likely recoverable prospective resources discovered by the EMD-1 well are approximately 100 MMbo.

During drilling of the target carbonates, severe mud losses occurred and hole conditions in the well deteriorated rapidly so multiple attempts at open hole logging by wireline failed until finally the decision was taken to terminate further efforts and suspend the well, which is the second well detailed in this report that seems to have failed on a technicality. The group has been granted a six month extension to the Mahdia permit to January 2015. It then has the right to elect for two additional renewals of the permit for 3 years each with a commitment of one well per period. The award of the Takelsa permit on the Cap Bon peninsular was ratified by the Tunisian authorities in late 2013 and planning for the first exploration phase of three years of work commitments is in progress, starting with the acquisition of seismic, followed by the drilling of four low cost onshore exploration wells.

In Oman the seismic has been interpreted and an exploration well location has been selected in the southern part of onshore block 49. The principle target depth is about 1,900 metres and the intended spud date is late H2 2014. The recent seismic survey on offshore block 52 is being processed and interpreted and there has been renewed interest in the group’s acreage following a discovery in the adjacent block to the north which augers well for securing a farm in partner to drill an exploration well next year. The bid for an onshore block continues to progress with no news as of yet.

During the period the group agreed a reserve based lending facility of up to $100M with IFC, part of the World Bank Group. The facility matures in 2018 and during the period the group drew down $25M which was used to repay the $12.5M facility agreed with Ahli United Bank of Egypt. This seems like a better company to borrow from. The group continues to receive payment from the Egyptian government, albeit at the same belated rate as before. The oil price achieved in Egypt was $104.3/bo and the gas price achieved in Morocco was $10.3 per MMsef.

The board see an exciting period ahead that includes new drilling in both Morocco and onshore Oman. Circle finished the half year with increased revenue from its production in Egypt and Morocco and the company is now drilling its 2nd well of twelve in Morocco and recently completed operations offshore Tunisia and forthcoming operations in both Oman and onshore Tunisia have the potential to further enhance the asset base.

Overall this was an OK update. The exploration work in Tunisia has clearly taken its toll on the financials of the company with a fall in profits, net tangible assets and free cash flow. The reserves currently shored up seem as though they do not have a huge life ahead of them so hopefully some of these wells can help confirm some new reserves. Unfortunately both of the new exploration wells have experienced technical difficulties that have prevented testing so in some ways, the program has been a bit of a disappointment during the half year. There is not enough here to encourage me to buy but I will continue to keep an eye on the company.

On the 7th October the group released an update covering the exploration well CGD-12 in Morocco. The well was spud on 25th August and drilled to a TD of 1,232 metres. Gas shows were confirmed by wire logging and encountered at different levels in the Guebbas and Hoot sands. The total net gas pay encountered in the well from the wireline log analysis is 9.7 metres. The first test over the secondary target Intra Hoot sands flowed at a sustained rate of 2.21 MMScf per day on a 18/64” choke. The second test over the main target Hoot sands flowed at a sustained rate of 4.62 MMScf per day on a 24/64” choke. The well will be completed for further production and the Upper Hoot and Guebbas sands will be available for production at a later date. The rig will now be moved to drill KSR-12, the third well of the Sebou permit.

On the 11th November the group released an update covering a directorate change and an operating update. CEO Chris Green has given notice of his intention to step down and resign from the company after eight years, four as CEO and the search for a successor has started. In Morocco drilling continued on the KSR-12 exploration well in the Sebou Permit. It has a primary target in the Mid Hoot interval and a secondary target in the Upper Guebbas. The planned TD of the well is 1,980 metres and upon completion the drilling rig will be demolished and returned to work with another operator. Drilling will therefore start recommence on the next well in the campaign using another rig which is currently being mobilised. This rig has now been contracted to provide continuous cover for drilling the remaining nine wells in the exploration programme for the Sebou and Lalla Mimouna permits and be used for any required work overs and testing programmes, which is good to hear. Due to the onset of winter rains, the next wells will be drilled on higher ground in the Lalla Mimouna permit before returning to Sebou. Production levels continue to run in line with expectations at 7 MMscf per day.

In Egypt production in the NW Gemsa and Geyad permits continued in line with predictions with oil production varying between 9,300 and 9,700 bopd and gas delivery of 10 to 11 MMscf/d. Receivables levels continued to be in line with earlier guidance and regular payments continued from EGPC. The group is expecting an additional one-off payment from the announced special tranche allocated to reduce overall oil company debt in the country. In Tunisia, the results of the Mahdia well are being interpreted in order to produce data to permit the commencement of a farm out for future block appraisal and the company has apparently already received expressions of interest from a number of companies which will be pursued in the coming months. Meanwhile they are in discussions with the Tunisian authorities regarding the renewal of the permit for another three years. As a result of various delays and technical challenges, the well came in at the top end of the board’s cost expectations but not enough to hamper the company’s plan going forward. They are still waiting further news from the operator regarding the well to be drilled in the Ras Marmour permit.

In Oman the group is engaged in preparations to commence drilling the block 49 commitment well. Access roads have been constructed to the main road and the drilling rig base and mud pits ahave also been completed. The rig has been identified and contracts are being finalised so it should begin soon. This well is a high risk prospect so it seems the Chairman is trying to play down expectations. The Shisr-1 well will target the main prospect at 1,883 metres and a secondary target at 2,669 metres with a TD of 2,768 metres. Discussions are continuing regarding the possibility of a farm out in the offshore block 52 and results of the seismic survey have confirmed the presence of the shallow water prospects and added a fourth prospect to the portfolio. Trading as a whole was in line with expectations.

On the 22nd December the group released an update regarding the KSR-12 exploration well in Morocco’s Sebou permit in which they found a significant gas discovery. The well was drilled to a TD of 1,980 metres and gas shows were encountered at two different levels within the Hoot sands. The net gas pay encountered in the well is 19.5 metres in the main target Intra Hoot sands and 1 metre in the Upper Hoot which is a greater thickness than originally expected and pressure testing showed that these sands are not connected to the Hoot sands in the other nearby KSR wells. The first test over the primary target main Hoot sands flowed at a sustained rate of 8.09 MMscf/d on a 20/64” choke over eight hours with no decrease in well head pressure. The second test over the upper Hoot sands produced a stabilised rate of 2.32 MMscf/d on a 9/64” choke over ten hours. The well will be completed for production for future production in the Main Hoot sands and Upper Hoot will be completed for production once the Main Hoot gas sands have been depleted.

A new rig was transported to Morocco but due to recent heavy rains affecting access roads into the drill site area in Lalla Mimouna, it cannot be delivered there at present. In order to avoid any further delay the drilling sequence is being modified and the rig will now be transported to the KAB-1 bis location in the Sebou permit, where access is presently possible. This well is a re-drill of the KAB-1 well which was drilled in 2011 and encountered swelling clays that compromised the integrity of the borehole, leading the well to be abandoned before wireline logging and testing but before this happened, the well encountered good gas shows at the target level. The new well has the same target with an updated mud system to minimise drilling problems in a slightly more updip location. The primary target Guebbas sands are expected at a depth of 1,272 metres and the TD of the well is 1,360 metres.

The rig is then scheduled to move to drill the first wells on the Lalla Momouna permit with the first well of the campaign, LAM-1 being located in the central part of Lalla Momouna Nord on the Anasba ridge within the existing 3D seismic area. The target for the well is for Miocene gas bearing sands, similar to the previously made Sebou discoveries. The sands are expected at a depth of 1,130 metres and the TD of the well is 1,431 metres. In summary, the KSR-12 well has found the thickest gas sand interval to date in Sebou and management believe that this well will add significant volumes to the reservoirs for potential gas production.

On the 22nd December the group announced that Mr. Colin Blackbourn no longer holds a notifiable interest in the group.

On the 7th January the group announced the appointments of Anthony Maris (53) and David MacFarlane (57) as non-executive directors of the company. Anthony Maris is currently COO of SOCO International and David MacFarlane was finance director at Dana Petroleum, overseeing a tenfold growth in market cap before the sale of the company to the Korean National Oil Company. He was aslo a director at Kentz when it was acquired by SNC-Lavalin group and is currently a director at Energy Assets. These seem like quality appointments to me.

On the 8th January the group announced that it had appointed Susan Prior (44) as executive finance director. Since 2012 she has been a transaction services director at PWC for their oil and gas deals team. It is good to see an executive position at the finance director level as one has so far been lacking.

On the 9th January the group announced that it had received $15M as part of a recent special payment distribution by the Egyptian government to oil companies operating in the company. This significantly reduces receivables from them and in my view somewhat de-risks operations there so this is very pleasing to see.

On the 12th February the group gave a financial and operating update. The recent fall in oil prices has had a substantial impact on the sector as a whole but while the group is not immune to this impact, it is somewhat moderated by gas production in Morocco where prices have remained stable. The existing convertible loan is due for redemption in July 2015 but Heads of Terms have now been agreed with regard to extending maturity to at least July 2017 which if successful would definitely be a help. The group currently has available cash of $34M and given the refinancing and ongoing oil price weakness, the board is reviewing the cost base and capital commitments.

In Egypt, production in the Al Amir SE and Geyad fields continues in line with previous guidance. The annual work programme is close to being finalised and is focussed on maintaining current production levels throughout 2015 and includes the drilling of three wells during the second half of the year. Two are planned as producers and one as an additional injector well aimed at providing further support to the AASE reservoir. In Morocco, following testing and completion of the KSR-12 well, the KAB-1 bis well has now been spudded and is the fourth well in the twelve well campaign. The company regards this well as lower risk due to the fact that it has been adapted to cope with the mud conditions and gas shows were encountered during the first run. Daily production from the Sebu permit continued at 6.5 to 7 MMscf/d, in line with previous guidance. The current drilling campaign has enable the replacement of depleted reserves and is now looking to add to the overall reserve base. The company anticipates being able to increase its sales of gas incrementally to both existing and new customers over the next two years as local demand for natural gas remains strong.

In Tunisia, the data from the Mahdia well is being made ready with the intention to start farm out discussions in the near future. The group continues to await final confirmation of approvals to drill the onshore Ras Marmour well. The prospect Sedouikech-1 is targeting a productive sand in the early Cretaceous Meloussi sand formation which is the proven reservoir in the adjacent Robbana field. Tenders are currently being evaluated in respect of the seismic for the Beni Khalled permit but management are considering postponing the award of the tender in order to obtain better pricing. It is thought that such actions will have a minimal impact on the overall timetable of the project.

In Oman, the start-up for drilling the Shisr-1 well in block 49 has commenced. The well is located in the SE area of the block onshore in the Dhofar province of Southern Oman. It lies on the NW dipslope of the NE trending Ghudun high and updip of the Dauka-1 well in the central area of the block 3D survey. Both targets are potentially oil-bearing Haima Group sands of Ordovician age. The primary target Hasirah sands are expected to be at a depth of 1,890 metres and the secondary target Ghudun sands are expected to be at a depth of 2,420 metres with a TD of the well of 2,550 metres. The drill duration is expected to be between six to eight weeks and the completion of the well fulfils the groups obligations in respect of this block. As previously mentioned, this is considered a high risk commitment well with a loss possibility of success. The company also continues to seek a farm in partner for the offshore Block 52 but the downturn in the oil price is making this a challenging objective.

Overall, there seems to be progress being made in Morocco but the slide in oil prices makes this a difficult investment at this time. I suspect they will struggle to find farm in partners and the priority will probably be on keeping those dwindling reserves at a decent level.

When looking at the chart we can see the share has undergone a strong decline as the oil price fell but this year has so far bottomed out. The share price seems to be testing the 50 day moving average but the trend is probably still sideways. I may look for an entry point in the future but that point is not now.

On the 4th March the group announced the results of the Shisr-1 well Block 49, onshore Southern Oman. The decision has been taken to plug and abandon the well after it encountered drilling difficulties on reaching a depth of 1,650 metres. No hydrocarbons were found but it seems as though the drill did not reach the primary target Hasirah sands prognosed at a depth of 1,890 metres. The Bottom Hole Assembly (BHA) became stuck below the 9 5/8 inch casing shoe which had been set at 819 metres. Multiple attempts were made to remove it but they proved unsuccessful. The group have been advised that further attempts to deepen or sidetrack the borehole are not a good idea. This well was always going to be a risky venture but it is a shame that nothing has really been learned in this venture.

On the 16th March the group announced the results for the drilling of the KAB-1bis well in the Sebou permit, onshore Morocco. The well spudded on the 4th February and was targetting the same sands that the KAB-1 well targetted in 2010. That well encountered gas shows but problematic swelling clays created borehole instability and the well could not be logged or tested. This time the well was drilled with an adapted mud system to minimise drilling problems in a slightly more updip location. Unfortunately the target Guebbas sands were absent down to a depth of 1,410 metres and it was decided to plug and abandon the well. The result indicates that the gas shows encountered previously were of a very limited extent. The rig has been released to complete and test the SAH-W1 well on the western area of the Sebou permit. The well encountered three gas bearing Guebbas sands but could not be completed as a non-standard 4.5 inch liner was needed. This is more disappointment from the company on a well that was supposed to be lower risk.

On the 24th March it was confirmed that CEO Chris Green was stepping down with the search for his replacement ongoing.

On the 27th April it was announced the group had signed an agreement to amend and extend the current convertible loan which had previously been due for redemption by July 2015. The group will now repay $10M before the end of July whilst extending the remaining $20M until July 2017 at a revised conversion price of 13.6p per share which removes one uncertainty hanging over the company.

On the 11th May the group released an operating update for Morocco that includes the preliminary testing of the SAH-W1 well in the Sebou permit. The well was drilled to a depth of 1,263 metres in June 2014 with gas shows encountered at different levels within the target sands. The group will start production from the lowest zone, followed by the main zone. The lowest zone has 3.6 metres of net pay and the test over this interval flowed at a sustained rate of 4.94 MMscf/d on a 24/64” choke during a period of five hours. The rig has now been released from the well and is being transported to the Lalla Mimouna concession to drill the company’s first well on this permit (LAM-1). The target of this new well is for Miocene gas-bearing sands, similar to the Sebou discoveries. The primary target sands are prognosed at a depth of 1,231 metres and the total TD of the well at 1,521 metres. The chairman believes that after the test of the SAH-W1 well, it has potential to add significant volumes to reserves for gas production.

On the 12th May the group confirmed the spudding of the LAM-1 well on the Lalla Mimouna permit, onshore Morocco. This is the first well to be drilled by Circle on the permit and is located in the centre of the area, on the Anasba Ridge. The well is only expected to take between 14 and 20 days to drill, so hopefully there will be some news soon.

On the 29th May the group announced that it had finally appointed a new CEO. Mitchell Flegg will join from Serica where he has been since 2006 including as COO since 2011.