Sylvania Platinum has now released its interim results for the year ending 2015.

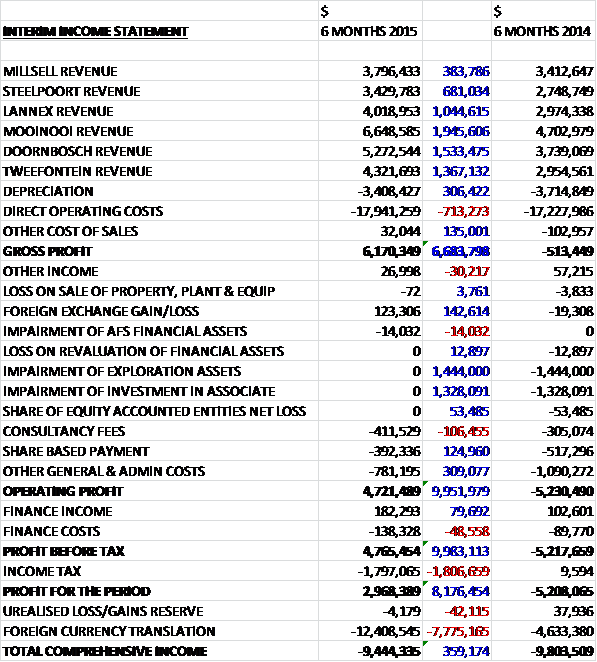

When compared to the first half of last year, revenues increased across all plants with the previously problematic Lannex and Mooinooi, along with the newer Doornbosch and Tweefontein plants increasing by more than $1M each. Direct operating costs increased slightly and gross profit was $6.7M higher at $6.2M. There was a positive foreign exchange gain and a lower share based payment, along with the lack of the two impairments that occurred in the first half of 2014 which helped operating profit swing $10M to the better before a higher income tax meant that the profit for the year enjoyed an $8.2M positive swing at just under three million dollars.

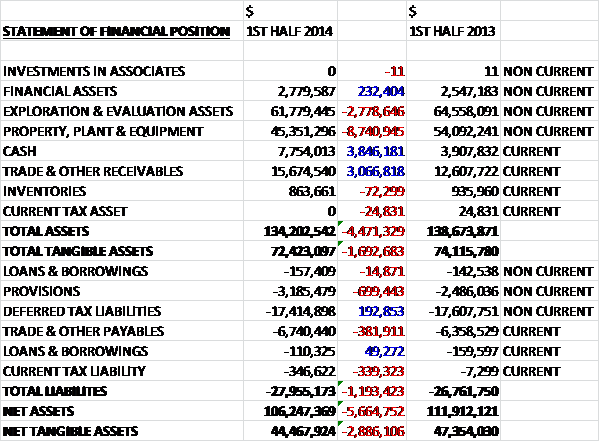

When compared to the first half of last year, total assets fell by $4.5M driven by an $8.7M decline in the value of property, plant & equipment, approximately half due to foreign currency movements and half due to depreciation, and a $2.8M fall in exploration & evaluation assets due to foreign currency movements, partially offset by a $3.8M increase in cash levels and a $3.1M growth in trade and other receivables. Liabilities increased during the period due mainly to a $700K increase in provisions. The overall net tangible asset level fell by $2.9M to $44.5M, although this does seem to be due to the fact that the tangible assets are denominated in South African Rand.

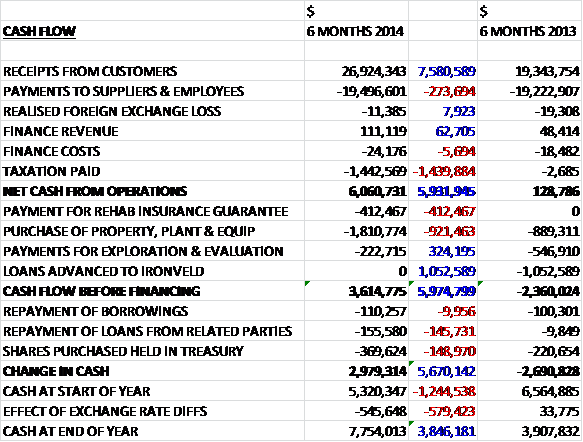

Cash receipts from customers romped ahead by $7.6M, tempered only somewhat by a small increase in payments and a $1.4M growth in tax so that net cash from operations was $5.9M higher at $6.1M. This cash was mainly spent on property, plant and equipment and $412K went on payment for rehabilitation insurance. There was the lack of the $1.1M paid in loans to Ironveld and exploration payments fell so that free cash flow increased $6M to $3.6M. After a bit went on repaying loans and treasury shares, the cash flow for the six month period was an impressive $3M, a $5.7M swing to the positive when compared to the same period of last year.

The best profit performance came at Doornbosch with a result of $2.3M ($1.5M growth). Millsell enjoyed profits of $1.4M ($200K increase), Steelpoort posted profits of $1M ($800K increase), Tweefontein had profits of $900K ($1.3M increase), profits at Mooinooi were $300K ($1.6M improvement) and profits at Lannex were $256K (about a $1M improvement).

Overall the SDOs produced 31,341 ounces during the period compared to 25,189 ounces during the same period of last year. This was boosted by higher plant feed grades at Doornbosch and Tweefontein operations due to the type of material treated during the period and generally stable plant performances. The gross basket priced dropped just 1% to $899/oz whilst group cash costs fell by 18% to $611/oz mainly due to improved cost controls, a reduction in iron ore transport and equipment hire, and lower maintenance costs due to fewer breakdowns. Capital expenditure at the SDOs in general grew by 286% compared to the second half of last year as a result of new tailings facilities at Lannex, Doornbosch and Tweefontein, as well as the changeover from mechanical mining of the dumps to a hydro mining process. This new process is expected to reduce mining costs by up to 20% overall and the new PGM concentrate off-take agreement terms should also lead to reduced costs.

The company is still waiting for the outcome of the Mining Right Application for the Volspruit project with the public participation meeting for the Water Use License Application commencing in February. At the Grasvally Chrome exploration project, the group received permission to remove and dispose of a bulk sample of the minerals recovered during prospecting activities. The plan is to extract a bulk sample from small open pits in three separate areas on the chromite seam outcrop to ascertain metallurgical recovery information in order to complete the MRA. A resource model is being completed over the southern half of the property and the near surface resource will be classified into indicated and inferred categories. Further exploration will consist of a drilling programme in the north of the property for a near surface resource and additional drilling will be performed to categorise the deeper underground resource.

Overall this was a very good update. All of the plants seem to be performing well and are profit making despite a flat platinum price. The group is now cash generating but the balance sheet did weaken slightly, although I’d guess this is due to the South African Rand depreciation and the effect this has on the group’s assets. The exploration licenses are progressing rather slowly but the board seem to be doing this in a sensible, measured way. I do really like this company, although the issues around the South African labour problems are never far away and of course, the group is still susceptible to the platinum price and foreign exchange changes. I am considering buying in here.

On the 9th March it was announced that the DMR had granted mining rights for the mining of Platinum group metals over three of the group’s sites, being the farms of Cracouw 391 LR, Aurora 397 and Harriets Wish 393 LR. The rights have been granted to Hacra Mining which is a 71% held subsidiary of the group. Also the DMR has granted rights for the mining of iron ore, vanadium and heavy metals which will be transferred to a subsidiary of Ironveld.

On the 31st March the group released its initial mineral resource estimate following work done on the southern section at the Grasvally chrome project. It showed an initial mineral resource of 64,900 tons of high grade chromite with a grade of 40.7% Cr2O3 and a Chrome to Iron ratio of 2.19:1, all of which is accessible by small and shallow open pits. It is likely that this figure will increase as the exploration of the Northern section and deeper portions of the lease area is concluded over the next few months. The total cost of the project to date is R35.9M, comprising R22M to purchase the prospecting rights, R5M to secure the chrome dumps, £8.9M spent on trenching and rehabilitation with a further R2.7M planned for exploration of the Northern section of the surface outcrop of the ore body over the next six months.

On the 27th April the group released a statement covering performance in Q3. The combine production for all of the dump operations was 12,778 ounces and the company remains on track to exceed the production target of 53,000 tonnes for the year with the production for the year to date some 15% higher than last year despite the decline this quarter. The cash cost of production increased by 5% on last quarter to $619 per ounce due to the lower production volumes. This lower production was caused by a structural failure on the Lannex plant’s thickener that resulted in some downtime and a five day safety stoppage at the host mine that affected production at the Mooinooi and Millsell plants. Another issue was community unrest related to municipal service delivery at the Eastern operations that affected production at the Steelpoort, Lannex, Doombosch and Tweefontein operations.

The gross basket price of $833/Oz represents a 6.7% decline on that achieved during the previous quarter as a result of the drop in the commodity price which, when combined with the lower production resulted in a 19% revenue drop to $10.5M with the above issues contributing to an EBITDA fall of 57% to $1.4M. The cash generation remained good, though, with a $1M increase in the group’s cash balance quarter on quarter to $8.8M which represented a $2.9M cash generated from operations with $600K spent on the general business capital for the plants, $200K spent on exploration assets and $1M spent on share buy backs. Profitability in Q4 is likely to be further impacted by the continuing low metal prices and production for the year should be between 55,000 to 57,000 ounces.

The company continues to await the outcome of the mining rights application for the Volspruit project with a final decision expected before the end of July, dependent on the duration of the independent peer review. The application for the DMR at the Grasvally Chrome Exploration project will be submitted in May with a total of 1,317 metres of diamond drilling being completed by the end of the period, with planned completion of some 2,425 metres of drilling by early May. Once this drilling is completed and a JORC compliant resource is declared, this chrome deposit will be sold. The official signing to execute the mining rights at Harriet’s Wish, Aurora and Cracouw has been delayed pending a request to the DMR to reduce the amount of financial provision for rehabilitation. Upon finalisation of this, an application to transfer the right to mine iron ore, vanadium and heavy metals to Ironveld will be made.

The group have also announced the appointment of Eileen Carr as non-executive director as a replacement of Grant Button who has stepped down from the board after spending 11 years in his role and 14 years at the company in total. She has 25 years of experience in the resources sector including as Finance Director at Cluff Resources. Overall, this is a bit of a disappointing update with the various problems at some of the plants and the continued weakness in Platinum prices. Despite this, cash generation remains good and the company still looks a strong play in a troubled sector.

On the 11th June the group released a statement clarifying the position over the Volspruit development. Contrary to newspaper reports, the Environmental Impact Assessment was not rejected by the Limpopo Department of Economic Development (LEDET) requiring the application process to be restarted. In actual fact, LEDET requested clarification on matters related to water consumption by the project and requested additional work on the assessment be done to include a biodiversity and wetland offset strategy to address any potential loss of flora and fauna species or potential damage to the wetland located near the northern mining pit perimeter.

During the past week, the Environmental Assessment Practitioner released a statement that meetings would be held with LEDET to confirm further actions to be taken by the company to address their concerns and submit an amendment to the application. Sylvania has until the 19th July to submit an amended application which should be the final stage of the process. The group remains optimistic that the application will be granted as the detailed environmental impact study did not find any fatal flaws within the proposed project.

On the 29th July the group released an update covering Q4 2015. In all, some 13,468 ounces were produced during the period, bringing the total for the year as whole to 57,587 ounces. This represents a 5% improvement quarter on quarter and a 7% increase year on year and outperformance compared to the initial expectation of 53,000 ounces for the year. This improvement is attributable to higher feed tonnes and a slight improvement on recoveries despite lower feed grades.

The problems arise with the selling prices, however, the gross basket price of $1,032 per ounce is approximately a 2% decrease compared to the price of $1,049 per ounce in the previous quarter. The platinum and palladium price has dropped significantly since March which has directly impacted the basket price. After smelting and penalties, this resulted in a revenue drop of 5% compared to last quarter to $10M.

The group cash balance at the period end was $8.4M and cash generated from operations was just $200K with $800K being spent on stay-in-business capital and exploration asset rights applications, $500K being received from the partial repayment of the loan to Ironveld and $800K being spent on share purchases.

The cash cost of production remained stable compared to Q3 at $638 per ounce and increased by 1% when compared to Q4 last year. While the combined plant feed head grade was slightly lower than the previous quarter, plant feed tonnes, PGM feed tonnes and recovery efficiencies improved for the operations, contributing to the higher PGM ounce production in the period.

At the Volspruit Platinum Exploration license, the additional information requested was released for public review last week and will be submitted to LEDET at the end of August following an opportunity for comment by interested parties. LEDET will then have 120 days in which to consider the addendum and, assuming that it is accepted, another 30 days to grant the EIA towards the end of January, although it is expected that the department will make every effort to announce its decision sooner.

Exploration has continued over the northern portions of Grasvally in order to declare a JORC compliant resource which will be required by the company in order to exercise a mining right over the resource. Exploration has been in the form of an extensive drilling programme targeting both the upper and the lower chromite layers. The drilling was completed at the end of April, totalling 2,539m and the logging of samples in underway, to be completed by the end of the month. Using all acquired data and the previously published southern resource model, a complete resource model will be developed over the entire property. This will describe both the shallow resource which will be minable by opencast methods as well as the deeper, underground resource. This resource contains some of the best quality local chromite ore and represents an opportunity for the company to diversify its operations or to consider a brand new venture.

Going forward, the basket price of platinum remains a concern for the foreseeable future but the board is confident that they can continue to produce profitably if the basket price does not further reduce (a big “if” in my view). Overall, this should have been a good update with an increase in the volume of metal produced and progress on the Grasvally resource but the continued collapse in the platinum price undermines all of this and I feel until it improves, this is a difficult investment so I have sold my shares (although in the long term I think this is a great company).