Colefax have now released their interim results for the year ending 2019.

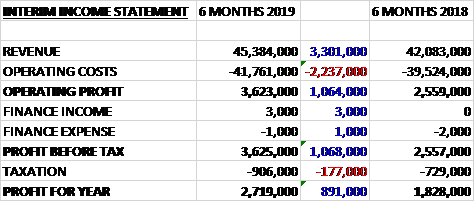

Revenues increased by £3.3M when compared to the first half of last year. After operating costs were up £2.2M the operating profit grew by £1.1M. A £177K growth in tax charges gave a profit for the period of £2.7M, a growth of £891K year on year.

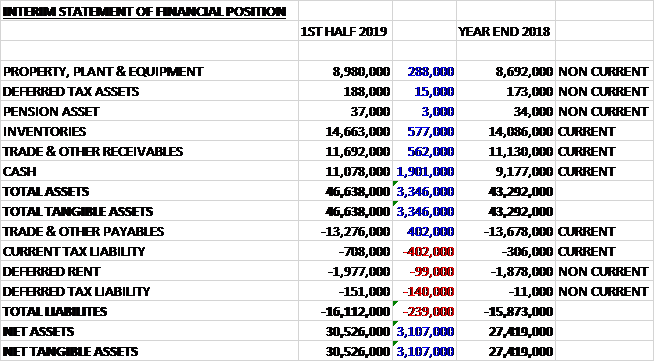

When compared to the end point of last year, total assets increased by £3.3M driven by a £1.9M growth in cash, a £577K increase in inventories, a £562K growth in receivables and a £288K increase in property, plant and equipment. Total liabilities also increased during the period as a £402K decline in payables was offset by the £402K increase in current tax liabilities along with a £140K increase in deferred tax liabilities and a £99K growth in deferred rent. The end result was a net tangible asset level of £30.5M, a growth of £3.1M over the past six months.

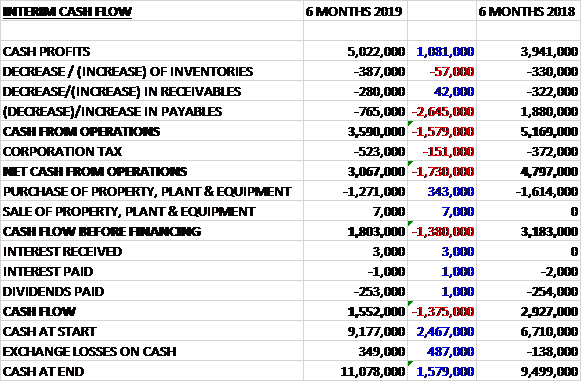

Before movements in working capital, cash profits increased by £1.1M to £5M. There was a cash outflow from working capital and after tax charges increased by £151K the net cash from operations came in at £3.1M, a decrease of £1.7M year on year. The group spent £1.3M on property, plant and equipment to give a free cash flow of £1.8M. Of this, £253K was spent in dividends to give a cash flow of £1.6M and a cash level of £11.1M at the period-end.

The main reason for the increase in profits was a strong first half performance from the decorating division. In addition hedging losses reduced by £522K due to the absence of contracts put in place before the Brexit referendum.

Sales in the fabric division increased by 1%. Excluding hedging losses, operating profits reduced by 2% to £2.9M reflecting challenging market conditions in the UK and Europe. Sales in the US increased by 2%. Trading became more difficult towards the end of the period with sales down 0.3% in Q2 despite relatively strong economic conditions. The board believe the confidence in the sector has been impacted by rising interest rates and stock market volatility. They are about to start the refurbishment of their LA showroom and expect this project to be completed by July. Currently they lease and operate eight company owned showrooms in the US.

Sales in the UK were flat during the period. The high end housing market remains very weak and the board believe conditions in the UK will remain difficult until the uncertainty of Brexit is resolved. In August they completed the refurbishment of their showroom in the Chelsea Harbour Design Centre and they are pleased with the positive reaction from customers.

Sales in Continental Europe decreased by 1%. Trading in most major markets has been weak. In France sales were flat but were helped by a significant contract order. In Germany sales were down 8% and Italian sales were down 15% reflecting very challenging economic conditions. They do not expect any short term improvement in trading conditions in most European markets. Sales in the ROW decreased by 2%. In Russia they changed their method of distribution from a distributor to an agent and are optimistic about growth prospects there.

Sales in the furniture business increased by 14% and the operating profit increased by £80K to £102K. This reflected a strong order book at the start of the year which is currently in line with last year.

Decorating sales increased by 16%. This was a strong performance reflecting the completion of a number of major projects during the period. As a result the business made a first half profit of £738K, an increase of £525K. Decorating sales can vary significantly between periods according to the timing of contract completions. For the current year sales will be weighted to the first half and they expect sales for the full year to be below the exceptional performance last year. Customer deposits remain at a healthy level and they remain optimistic about trading from the new Pimlico Road showroom which is performing well in its second year.

Going forward, in the US market the group continue to benefit from the strength of the US dollar but the confidence seen at the start of the year has slowed recently and the board are therefore more cautious about growth. In the UK, trading remains challenging, partly due to the high level of uncertainty surrounding Brexit, and in Europe they expect trading to remain difficult.

At the current share price the shares are trading on a PE ratio of 13.9 which falls to 13.7 on the full year forecast. After a 4% increase in the interim dividend the shares are yielding 1% which remains the same for the full year forecast. At the period-end the group had a net cash position of £11.1M compared to £9.5M at the same point of last year.

Overall then this has been a good period for the group. Profits were up, net assets increased and although the operating cash flow declined, cash profits increased and plenty of free cash was generated. The good performance looks unlikely to be repeated in the second half, however, as the improvement is mainly due to a lack of hedging losses and some large projects in the decorating division. The furniture business is performing well but it remains small, and excluding hedging movement, the fabric division suffered in all regions. Of some concern is that after the first quarter, the US market is now also suffering. The forward PE of 13.7 is decent enough but the dividend yield of 1% is nothing to write home about. On balance I feel like the risks are to the downside here.