Solid State has now released their interim results for the year ending 2019.

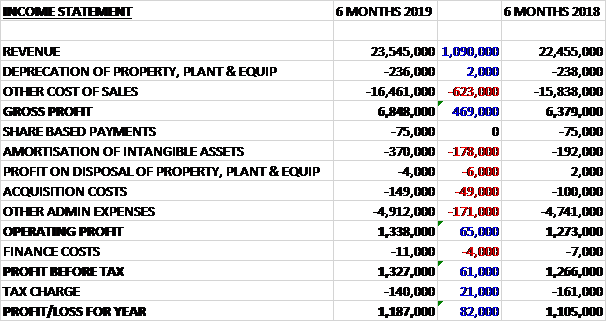

Revenue increased by £1.1M and cost of sales was up £623K to give a gross profit £469K higher. Amortisation charges grew by £178K, acquisition costs were up £49K and other admin expenses rose by £171K which meant that the operating profit increased by £65K. Finance costs were up £4K but tax charges declined by £21k to give a profit for the period of £1.2M, a growth of £82K year on year.

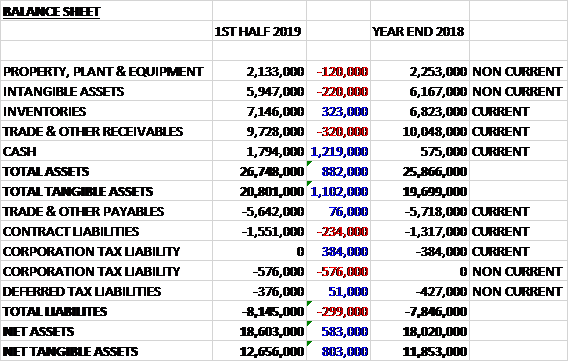

When compared to the end point of last year, total assets increased by £882K driven by a £1.2M growth in cash and a £323K increase in inventories, partially offset by a £320K decline in receivables, a £220K fall in intangible assets and a £120K reduction in property, plant and equipment. Total liabilities also increased during the period due to a £192K growth in tax liabilities and a £234K increase in contract liabilities. The end result was a net tangible asset level of £12.7M, a growth of £803K over the past six months.

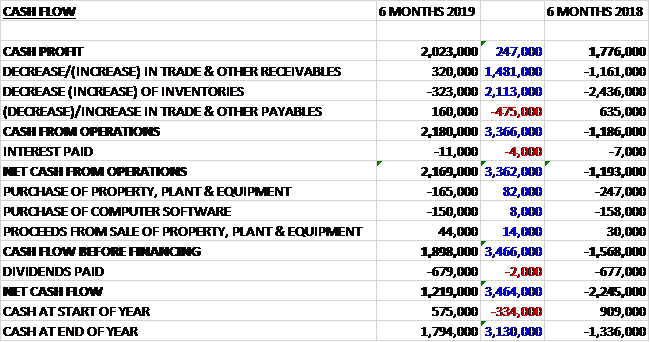

Before movements in working capital, cash profits increased by £247K to £2M. There was a small cash inflow from working capital compared to a large cash outflow last time and after interest payments remained broadly flat the net cash from operations was £2.2M, an improvement of £3.4M year on year. The group spent £165K on property, plant and equipment and £150K on computer software to give a free cash flow of £1.9M. They then paid out £679K in dividends to give a cash flow for the period of £1.2M and a cash level of £1.8M at the period-end.

The distribution division has had a particularly strong period, delivering 26% organic growth in revenues to £12M with slightly improved margins. The have benefited from a one-off client order of £1M and the military market showed particularly strong growth. The increased revenues attest to the wider range of products and recognise the increasing value of the division to its customer base. Examples of the value added services are sourcing and obsolescence which have started to contribute at meaningful levels. Securing the exclusive VPT franchise is expected to positively impact the second half and the division is well positioned for a strong period.

Revenues in the manufacturing division declined by £1.4M to £11.5M but the gross margin improved due to a richer sales product mix. The order book going into the year was second half weighted which is expected to result in an improvement in sales performance in H2. The sales emphasis has been on winning more complex value added business. They have continued to implement the planned investments in the Power business in Crewkerne with a focus on automation to pave the way for higher sales volumes in the second half and improved efficiency.

Group order intake increased by 38% to £33.3M and as of the period-end the open order book amounted to £29.4M, the majority of which is expected to be delivered in the next year.

After the period-end, in November, the group acquired Pacer Technologies for a cash consideration of £3.7M. Last year the business reported a pre-tax profit of £430K and the acquisition generated goodwill of £2.7M which seems fairly decent value. The business distributes and designs optoelectronic components, lasers and displays to the OEM market in the medical, military, commercial, industrial and security sectors. They operate in components and displays and products include industrial LEDs and light sources, lasers and laser range finders, photon detection and counting equipment. It is an established US business based in Florida with offices in the UK.

Going forward the strength of the order book and the acquisition of Pacer gives the board confidence in being able to deliver a stronger second half and continued growth. The board is confident of meeting market expectations for the year as a whole.

At the current share price the shares are trading on a PE ratio of 15.4 which falls to 11.7 on the full year forecast. After a 5% increase in the interim dividend the shares are yielding 3% which remains the same on the full year forecast.

On the 30th January the group released a trading update where they stated that they expect trading results for 2019 will comfortably exceed current market expectations. Revenues are expected to be above current guidance and adjusted profits significantly ahead. The strong demand seen in the first half in the distribution division has continued into the second half. With increased revenues and the impact of operational gearing, the division is now expected to deliver results well ahead of management’s previous expectations.

Sales in the manufacturing division are second half weighted. Some of the first half shortfall is expected to be mitigated in the second half, delivering revenues broadly in line with management expectations, although slightly lower than last year.

The focus in the manufacturing division has been on improving the mix of sales. The second half has benefited from the initial shipments of the new power packs for the industrial smart warehousing contract announced in June 2018, and the resolution of a technically challenging specification on a high value-added contract enabling product shipment. The improvement in gross margins seen in the first half has been maintained in the second half of the year and as a result a significant improvement in the full year gross margin is now expected.

The integration of the Pacer acquisition is progressing well. In addition to current year trading the order book now gives them confidence in an improved outlook for 2020.

Overall then this has been a good period for the group. Profits were up, net assets increased and the operating cash flow improved with a decent amount of free cash being generated. The distribution division is outperforming considerably whereas the manufacturing division is more subdued. We have now been told to expect an outperformance for the year and the forward PE of 11.7 and yield of 3% both look decent to me. I have bought more.

On the 30th April the group released a trading update covering the year. Profit will be slightly ahead of market consensus forecasts which are £3.5M. Revenue is expected to be ahead of expectations at £56M representing a 10% organic growth with the group benefiting from particularly strong value added distribution sales in Q4.

In the manufacturing division, progress in enhancing operating margins has been maintained and efficiencies in the power business are being delivered as a result of the capital investment in plant and equipment. The integration of Pacer is progressing as planned. The new facility in Weymouth began production in March.

Cash generation in Q4 has been much stronger than expected. Some of this strength is due to timing benefits resulting from proforma payments from customers, but the underlying cash generation was also pleasing. As a result, in April they made an early repayment of £2M of the highest price element of the term loan taken out for the acquisition.

The open order book of £35.9M is above the £25.6M of last year. The board is confident that its strategy will continue to deliver organic growth and that this can be complemented by further acquisitions.