Conviviality Retail is the UK’s largest off-licence and convenience chain and has 595 stores in England and Wales operating under the Bargain Booze, Wine Rack and Thorougoods brands through a network of franchises who are responsible for running the stores and driving sales. The group has a strong presence in the North West with scope for expansion elsewhere in the country. The product mix is 57% alcohol, 30% tobacco and the remainder other impulse buys. Conviviality Retail has now released its final results for the year ending 2014.

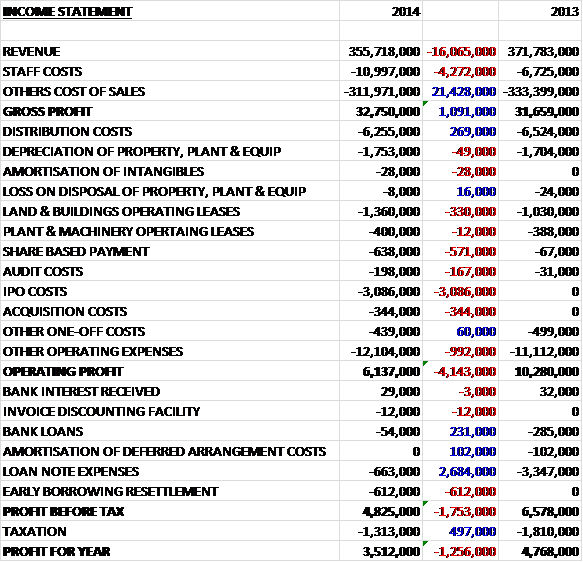

Revenues fell by £16.1M when compared to last year predominantly due to the closure of underperforming stores but a larger reduction in cost of sales meant that gross profit was some £1.1M higher. Operating costs were also higher and there was just over £3M in IPO costs which helped bring the operating profit down by £4.1M to £6.1M but the £2.7M reduction in loan note expenses and a near half a million pound fall in tax meant that the profit for the year was £3.5M, a reduction of £1.3M on 2013.

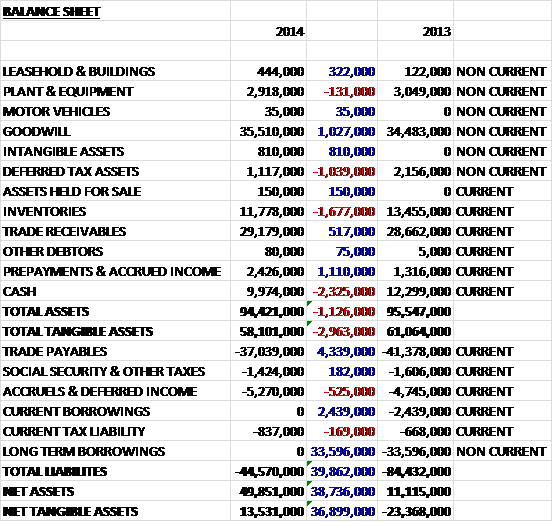

When compared to last year, total assets fell by £1.1M driven by a £2.3M fall in cash levels, a £1.7M reduction in inventories and a £1M decline in deferred tax assets, somewhat offset by a £1M increase in Goodwill. The £150K worth of assets held for sale relate to owned stores that are being marketed to potential franchisees which have subsequently been disposed of. Liabilities fell considerably as the group used its IPO proceeds to pay off £36M of debt and trade payables fell by £4.3M. This meant that net tangible assets increased by £37M to £13.5M.

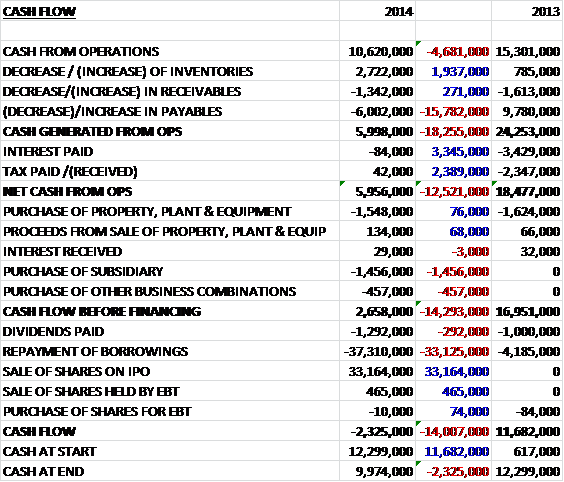

Before movements in working capital the cash profits were down £4.7M to £10.6M. A huge swing to a decrease in payables meant that cash before interest and tax was just under £6M, an £18.3M collapse from last year. The group paid far less interest, though, due to the repayment of debt and actually got a cash tax rebate so the net cash from operations was down £12.5M at just under £6M. About £1.5M of this cash was spent on capital expenditure and a similar amount was spent on an acquisition and another £1.3M on dividends. The IPO cash didn’t quite cover the repayment of all the loans and there was a deficit of £4.1M which explains the £2.3M cash outflow compared to the £11.7M inflow last year. Despite the outflow of cash, this would be a cash inflow if there were no loans to pay back (as is the case next year).

At £12.43M, EBITDA was on a par with last year. During the year 62 stores were closed which impacted sales by £15.7M. The opening of new stores was slower than planned and the group ended the year with 595 stores, 11 fewer than planned but average weekly sales were £430 higher per store. The group have now concluded the bulk of the store closures. Management have identified the North East and the South as areas with expansion potential and stores were opened in Longbenton, South Shields, Ramsgate, Stevenage, Broxbourne and Leighton Buzzard. Going forward, the group only spent the second half of the year as a public listed company and only in the final quarter did the board see the benefits really coming through with improved franchisee engagement so it will be interesting to see how this goes next year in the first full year.

The shops have a decent pricing offer with promotional pricing some 15% lower than the Supermarket’s convenience stores. The ever-important franchisees are incentivised by being offered equity in the company depending on store performance and the full allocation this year is expected to be 1.2M shares.

During the year the group purchased LCL Enterprises (Wine Rack) for £1.7M in cash. The acquired group came with £930K of net assets so they only paid £720K in goodwill. From the acquisition date in August 2013, Wine Rack has contributed £7.6M in revenue and £100K in profit before tax. This seems modest but the small acquisition cost suggests it may be worthwhile. After the end of the balance sheet date, the group acquired 31 stores from Rhythm and Booze, a subsidiary of Bibby Retail for £1.85M in cash, of which £200K is deferred, which added another £100K of profits.

The current Chairman, David Adams stepped into his role when Roger Pedder retired in January this year. At the same time two new non-executive directors joined in the shape of Steve Wilson and Martin Newman. This seems to be a period of some board room turmoil as Franchisee director Keith Webb resigned in July for personal reasons. One risk facing the group is the continued convenience expansion of the major supermarkets, continuing to increase competition, although this is being mitigated somewhat by the focus on alcohol but relying on products such as alcohol and tobacco means the group is somewhat exposed to the whims of the government who may introduce new regulations around these products.

If we ignore the one-off costs, the underlying P/E ratio at this share price is 14.3, reducing to 12.2 next year. At the current share price the yield is a very decent 5.5% increasing to 5.7% on next year’s forecast. There was a net cash balance of £10M at the year end. Overall then this was a decent update. Underlying profits seem to be doing OK, although growth is not stellar. The balance sheet looks much better now the loans have been paid off and there is a decent cash flow if the payback of these loans is taken out. There are some risks, though, as mentioned above and I think I would like to see some more progress made on revenues before jumping in.