Cranswick has now released their final results for the year ended 2017.

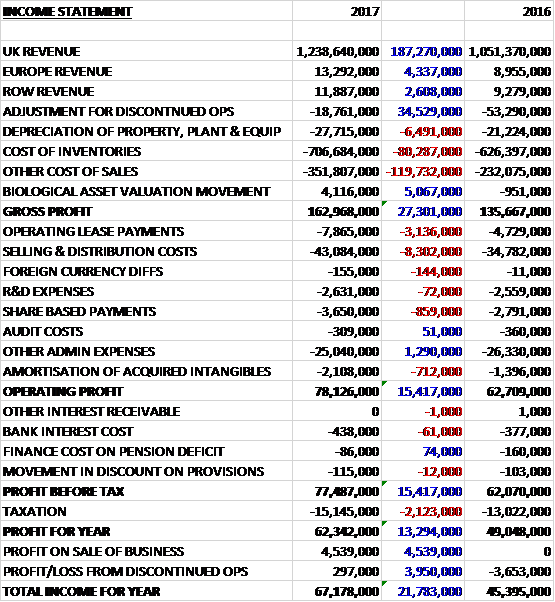

Revenues increased when compared to last year with a £187.3M growth in UK revenue, a £4.3M increase in Europe revenue and a £2.6M growth in ROW revenue. Depreciation was up £6.5M, cost of inventories increased by £80.3M and other cost of sales grew by £119.7M but there was a £5.1M swing to the positive for the biological asset valuation movement which meant that gross profit was up £27.3M. Operating lease payments grew by £3.1M and selling and distribution costs increased by £8.3M with share based payments up £859K. The amortisation of acquired intangibles increased by £712K but other admin expenses were down £1.3M to give an operating profit £15.4M above that of last year. Finance charges were flat but tax charges grew by £13.3M to give a profit from continuing operations of £62.3M, a growth of £13.3M year on year.

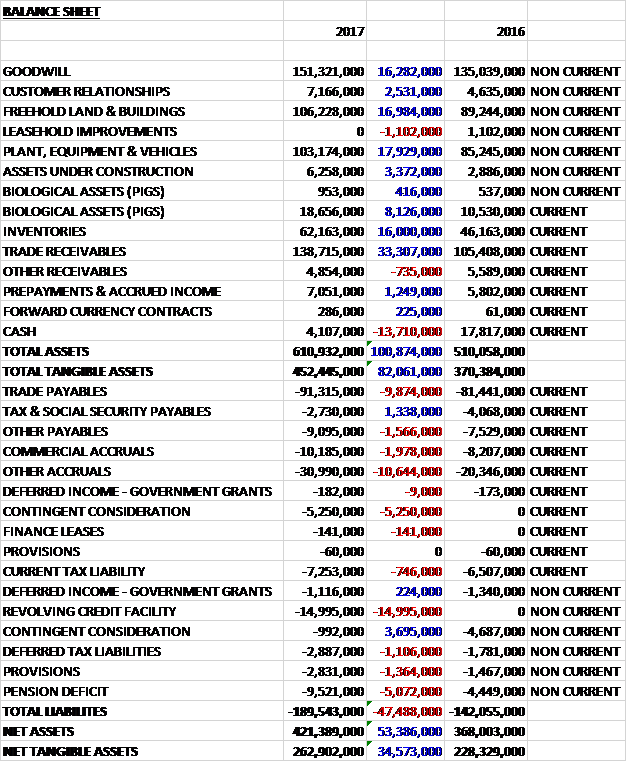

When compared to the end point of last year, total assets increased by £100.9M driven by a £33.3M growth in trade receivables, a £17.9M increase in plant, equipment and vehicles, a £16.3M increase in goodwill, a £16M growth in inventories, a £17M increase in freehold land and buildings an £8.5M increase in the value of the pigs, partially offset by a £13.7M decrease in cash. Total liabilities also increased during the year due to a £15M increase in the revolving credit facility, a £10.6M growth in other accruals and a £9.9M increase in trade payables. The end result was a net tangible asset level of £262.9M, a growth of £34.6M year on year.

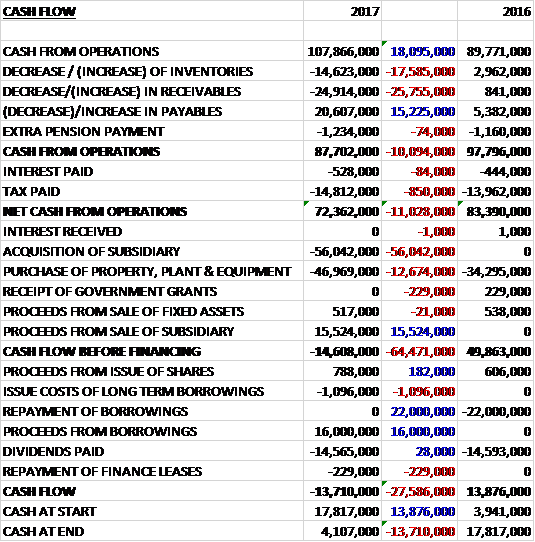

Before movements in working capital, cash profits increased by £18.1M to £107.9M. There was a cash outflow from working capital with an increase in inventories and receivables and after tax payments grew by £850K the net cash from operations was £72.4M, a growth of £11M year on year. The group spent £47M on property, plant and equipment along with a net £40.5M on acquisitions to give a cash outflow of £14.6M before financing. The group then took out £15M in new borrowings to pay for the £14.6M spent on dividends so there was a cash outflow of £13.7M and a cash level of £4.1M at the year-end.

Total revenues were up 22% and like for like revenues increased by nearly 13% on volumes that were 15% higher due to new contract wins, strong export sales and a greater number of pigs being processed through the three primary processing facilities. The operating margin at 6.1% was 29 basis points lower with the delay in recovering rising input costs through the second half of the year being partly mitigated by a positive contribution from the rapidly growing poultry and export business and a strong operational performance across each of the businesses.

Fresh pork revenue increased by 6.7%. Excluding the contribution from Ballymena like for like revenue growth was 2.1%. Performance was comfortably ahead of the overall UK Fresh pork category with market data showing a decline of 4% due to lower promotional expenditure and lower sales traditional roasting joints. Total export revenue grew by more than 38% reflecting growth in Far Eastern markets of 49% together with a 15% increase into other export markets.

A major overhaul of the Norfolk facility was completed in the year. Work is also underway at Ballymena to extend the butchery operations which will enable more pigs to be processed through the facility more efficiently. They are also planning to extend their Hull facility with work expected to start in the next financial year. Improvements in productivity together with rising pig prices resulted in an improved contribution from pig production in the year.

The UK pig price increased by 34% during the year rising steadily through to the end of December before stabilising in Q4 with the average price being 8% higher year on year. This reflected a more pronounced increase in the EU reference price due to strong demand from China and tighter supply in European markets.

Convenience revenue increased by 20% reflecting new business wins and new product launches, well ahead of the UK market. Cooked meats performed strongly reflecting new business wins coming on stream throughout the period. Three major new contracts, with business secured for the long-term and with built in pricing models to address raw material price movements, leave the cooked meats category in robust share headlining into the new year. The ongoing capital investment programme resulted in £19M being spent across the three sites during the period to upgrade the facilities, add capacity and introduce new capability to slow cook and BBQ ranges which have been added to the portfolio of products following recent contract wins.

Revenue from continental products also grew strongly and the two Manchester facilities are now operating at full capacity. To enable the business to continue to grow and develop, a new £25M facility is being built in the North West of England which will consolidate production from these two sites. The new site, located in Bury, will increase current capacity by about 70% and will enable existing and new product ranges to be produced more efficiently.

Gourmet products saw revenue increased by 16% with all categories in growth. Sausage sales were very strong. New contract wins with the group’s two largest retail customers for their Butcher’s Choice ranges, with together delivered 350 tonnes per week of incremental volume, underpinned this performance. Sausage production recommenced at the Norfolk facility early in the year to meet the increase in demand. Sales of premium burgers from the Lazenby’s facility also grew strongly. New mixing and blending equipment has been commissioned to support the next phase of growth and development of the facility with £6M being invested across the two sausage sites during the year.

The premium bacon sector continues to outperform the overall category but slower year on year growth compared to previous periods highlighted the recent trend by the retail customers to move away from promotional mechanics and multi-buy offers. Growth accelerated in the second half of the year following a new contract win. Pastry returned to volume growth in the second half of the year driven by a strong promotional plan with the business’ anchor customer and a new contract win in the food to go market. Further improvements to operational efficiencies throughout the year allied to an improved top line performance leave the business well placed to drive further volume growth next year.

Excluding Crown, poultry revenue increased by nearly 18%, comfortably ahead of the overall UK market. Sales of fresh poultry reflected strong volume growth. Crown made a very positive contribution to the group during the period with the number of birds processed increasing by 9% since the acquisition. Sales of premium cooked poultry also grew strongly. The £9M capital investment programme which was completed at the start of the year has enabled new business to be secured and produced more efficiently. More recently, contracts have been secured with two of the group’s principal grocery retail customers.

During the year the triennial valuation of the pension scheme was completed. Following a review of the valuation a new contribution schedule was agreed to further reduce the deficit. From 2017 to 2022, cash contributions will be increased from £1.3M to £1.8M per annum.

In November the group acquired Dunbia Ballymena for a total consideration of £18.1M including a deferred consideration of £1.3M. The business is a primary pig processor and establishes a presence in Northern Ireland. The acquisition generated goodwill of £9.5M with the deferred consideration contingent on gaining a licence to export to China.

On the 23rd July 2016 the group disposed of its shareholding in the Sandwich Factory for a total cash consideration of £15.5M. This represented a profit on disposal of £4.5M and the group also disposed of £7M of goodwill. The business made a profit of £297K this year before it was sold and last year made an underlying profit of £982K.

Going forward, the current year has started positively for the group and the board believes they are well positioned to meet the challenges that lie ahead.

At the current share price the shares are trading on a PE ratio of 22.5 which falls to 20.9 on next year’s consensus forecast. After a 20% increase in the final dividend, the shares are yielding 1.6% which increases to 1.7% on next year’s forecast. At the year-end the group had a net debt position of £11M compared to a net cash position of £17.8M at the end of last year.

Overall then this has been an excellent year for the group. Profits were up, net assets increased and although the operating cash flow declined this was due to working capital movements and cash profits increased. After acquisitions, the group didn’t generate any free cash, however. There was a good operational performance across all businesses but with a forward PE of 20.9 and yield of 1.7% this is included in the price. Nevertheless, this is a high quality business and might just be worth it.

On the 24th July the group released a Q1 trading update. Revenue in the period was 27% ahead of the same period last year. Like for like revenue grew 21% compared to the same period last year, underpinned by strong domestic volume growth with all product categories making a positive contribution. Rising input costs were partially mitigated during the period.

During the period further progress has been made on the new continental products factory in Bury which will consolidate current production from the existing two facilities and provide substantial additional capacity. Ongoing investment in the pork processing facilities at Preston and the recently acquired Ballymena site will increase pig processing capacity and drive further efficiencies.

At the end of the quarter net debt stood at £18m compared to £11M at the end of last year and the board is confident in the outlook for the year, which remains unchanged.