International Greetings has now released their final results for the year ended 2017.

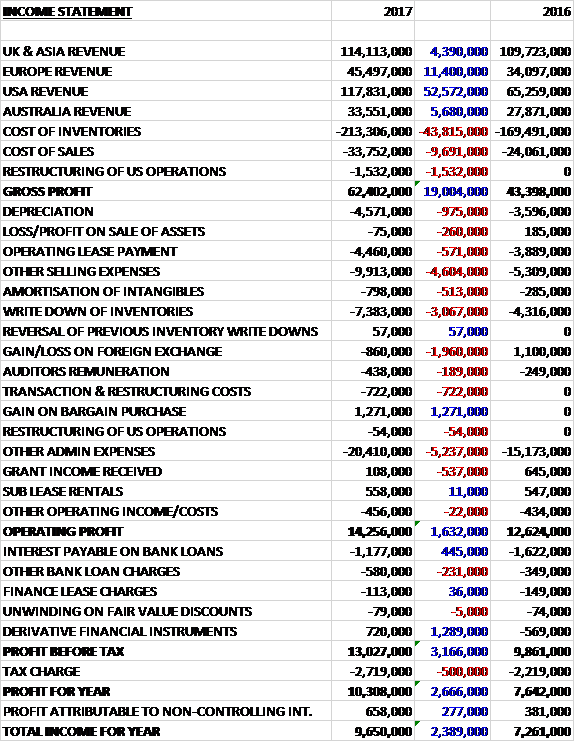

Revenues increased when compared to last year with a £52.6M growth in US revenue, an £11.4M increase in European revenue, a £5.7M increase in Australia revenue and a £4.4M growth in UK revenue. Cost of inventories were up £43.8M with £1.1M of this relating to an exceptional change due to the change of life of certain printing consumables, and other cost of sales increased by £9.7M with £1.5M being spent on the US restructuring to give a gross profit £19M above that of last year. Selling expenses were up £6.4M, there was a £3.1M growth in inventory write-downs and a £2M detrimental swing to forex losses with other admin expenses up £5.2M. There was a £1.3M gain on the bargain purchase, however, and the operating profit grew by £1.6M. The bank loan interest declined by £445K and there was a £1.3M positive swing with regards derivative financial instruments which meant that after the tax charge grew by £500K the profit for the year was £9.7M, a growth of £2.4M year on year.

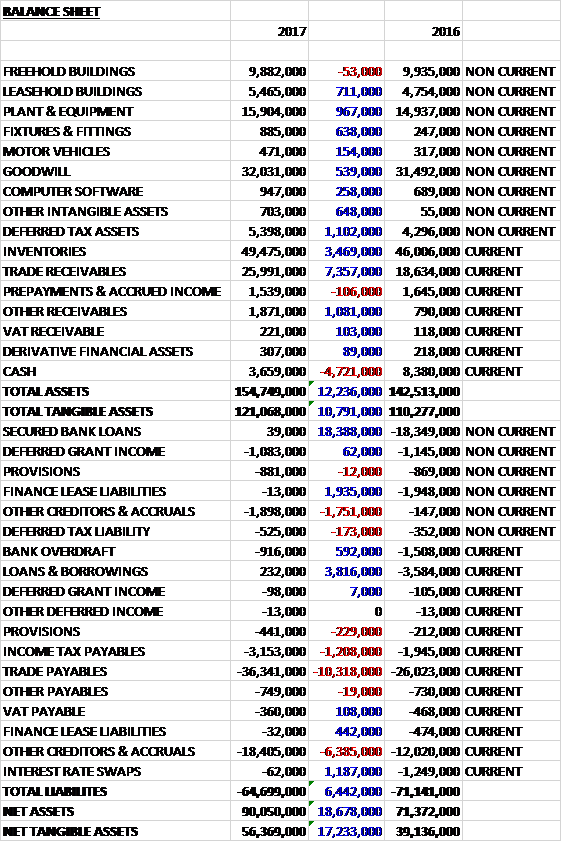

When compared to the end point of last year, total assets increased by £12.2M driven by a £3.5M growth in inventories, a £7.4M increase in trade receivables, a £1.1M growth in deferred tax assets, and a £1.1M increase in other payables, partially offset by a £4.7M fall in cash. Total liabilities declined during the year as an £22.2M decline in bank loans, a £1.9M fall in finance lease liabilities and a £1.2M decrease in interest rate swaps was only partially offset by a £10.3M increase in trade payables, an £8.1M growth in other payables and accruals and a £1.2M increase in income tax payables. The end result was a net tangible asset level of £56.4M, a growth of £17.2M year on year.

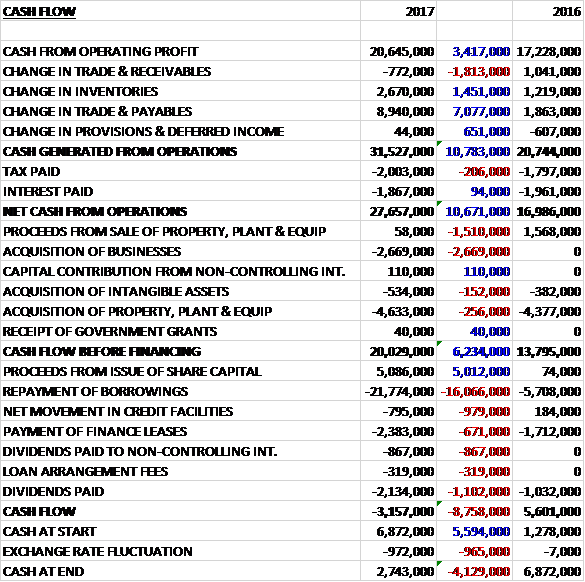

Before movements in working capital, cash profits increased by £3.4M to £20.6M. There was a cash inflow from working capital, in particular a large increase in payables and after tax payments increased by £206K the net cash from operations was £27.7M, a growth of £10.7M year on year. The group spent £4.6M on property, plant and equipment, £534K on intangible assets and £2.7M on acquisitions to give a free cash flow of £20M. The group received £5.1M from the issue of share capital, paid out £2.4M on finance leases, £2.1M on dividends and repaid £21.8M of borrowings to give a cash outflow for the year of £3.2M and a cash level of £2.7M at the year-end.

Weaker sterling has boosted the translational value of overseas earnings and the group made an acquisition in the year but even at constant exchange rates, like for like underlying profit improved by 21% (although this figure does annoyingly exclude LTIP charges which increased during the year.

The profit in the UK and Asian division was £5.4M, a decline of £159K year on year, driven down by the investments made in the business. There was a successful year in the Celebrations products categories with sales underpinned by a good manufacturing performance from the gift wrap manufacturing operation in Wales and card, back and cracker production in facility in China. Next year will see the first UK manufactures retail collateral products including bags produced for fashion and beauty retailers to provide to their customers. Whilst the group’s share of the UK market for gift packaging is substantial, the board believe there remains scope for profitable growth across these and other categories.

The profit in the European division was £4.5M, a growth of £1.6M when compared to last year and the group are now trading with each of the continent’s top ten retail groups in their product categories. The group sustained double digit momentum in Poland and Slovakia, underpinned by their strong trading partnerships with the major retail groups who have expended into these markets as well as local companies.

The profit in the US division was £6.1M, an increase of £2.7M when compared to 2016 reflecting organic sales growth across all channels as well as the acquisition of Lang. This year has seen the expansion of the product offering to include design coordinated ranges of partyware, giftware, celebrations and stationary products to both regional and national retailers. There has also been good momentum in sales growth achieved with the Creative Play products and see considerable scope for expansion across all of the group’s markets.

The profit in the Australian division was £1.7M, an increase of £216K year on year. The group have won a three year contract for the supply of greetings cards to Australia’s largest discount retailer, which counteracted headwinds with more commoditised Christmas product. This opportunity required investment in infrastructure and in-store fixturing, the benefits of which should begin to flow through during the coming year.

In July 2016 the group raised £5.3M by way of a share placing of 3,000,000 new shares a £1.75 per share. Also in July they acquired Lang Companies for a cash consideration of £2.7M. The business is a supplier of branded consumer home décor and lifestyle products based in the US. There was a bargain purchase profit of £1.3M and the business contributed profits of £528K to the group so this really does seem like an excellent acquisition.

The board have approved the investment in the Netherlands in a second high speed, HD printing press. Once in place in 2019, this additional press will reduce risk, increase efficiency and sustain further growth in profitability. In the US the business case for the final phase to update the printing capability is still under appraisal but likely to take place later than previously expected.

At the year-end the group had a net cash position of £3M compared to a net debt position of £17.5M at the end of last year although average leverage throughout the year stands at 2.3x EBITDA compared to 3.2x last year. At the current share price the shares are trading on a PE ratio of 27.6 which falls to 17.6 on next year’s consensus forecast. After an 80% increase in the dividend, the shares are yielding 1.3% which increases to 1.5% on next year’s forecast.

Overall then this has been another year of strong progress for the group. Profits were up, net assets increased and the operating cash flow improved with plenty of free cash being generated. The group has been helped by favourable forex movements and a recent acquisition but the underlying performance is still strong. All regions saw growth in profits except the UK, apparently because of the investments made. It is also worth noting that the group did get a cheeky placing away during the year which would have further boosted the reported results. The shares are no longer that cheap but with a forward PE of 17.6 they still look reasonable value and I am tempted to buy a few.

On the 29th August the group released a trading update covering Q1 trading, which was in line with management expectations with a strong pipeline built in all regions. Group sales, combined with overall customer order levels already received give the directors confidence in the outcome for the full year.

In the Americas, sales volume growth together with product mix is continuing to enhance margins across the broadening customer base. The region has achieved noteworthy momentum in the Creative Play categories. The investment in the gift wrap converting facilities continues to deliver production efficiencies. The region is also benefiting from further synergies from the Lang acquisition, in line with management plans.

In the UK, trading is line with expectations. The investment in the manufacturing of not for sale consumables is fully on schedule and on budget. The order book for these new products is building strongly and the initial shipments are scheduled to take place in H2.

Continental Europe is on course to achieve record sales and production levels across the core gift packaging product categories. The group’s second efficient printing press is on schedule and on budget to be installed in time for the main production in 2019. Additionally, sales of both stationary and gift products are encouraging, especially to the existing base of multiple retail customers.

Australia has seen particularly strong growth in the higher margin independent store sector. Having won a major new contract for the supply of every day greetings card with Australia’s largest discounter, they are benefitting from the economies of scale that this opportunity presents, particularly leveraging their logistical capability and scale. Overall this sounds good, I continue to hold.

On the 21st September the group announced the acquisition of Biscay Greetings, a greetings card and paper products business based in Australia for a cash consideration of £5.5M, generating goodwill of £2.4M. An injection of working capital of up to £1.8M will also be required. Biscay provides greetings cards and related products across Australia and New Zealand and last year generated an operating profit of A$2.9M. While negligible to underlying earnings this year, the acquisition is expected to be earnings accretive from the next financial year.

The acquisition will approximately double the group’s market share in the value channel of the greetings card market in Australia and it seems like quite a good one to me.

On the 29th September the group announced that director Lance Burn sold 67,500 shares at a value of £233K and he no longer holds any shares, which is not a great indication!