Cranswick has now released their interim results for the year ending 2018.

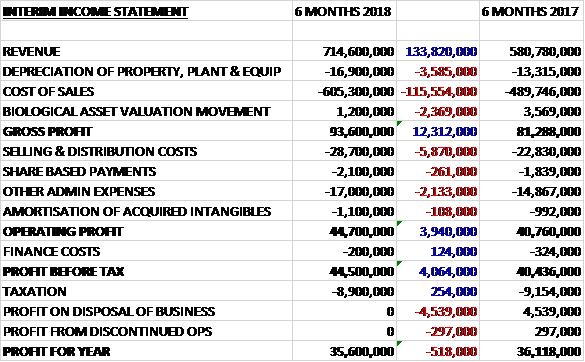

Revenues increased by £133.8M when compared to the first half of last year (£26M from Ballymena, £3.5M from Crown Chicken and the rest organic). Depreciation was up £3.6M, other costs of sales increased by £115.6M and there was a £2.4M fall in the growth in the value of the pig inventory to give a gross profit £12.3M higher. Selling and distribution costs were up £5.9M and admin expenses grew by £2.4M which meant that the operating profit was £3.9M higher. Finance costs were down £124K and tax charges fell by £254K but there was no profit from the discontinued operation which was £297K last time. All of this meant the profit for the period was £35.6M, a growth of £4M year on year.

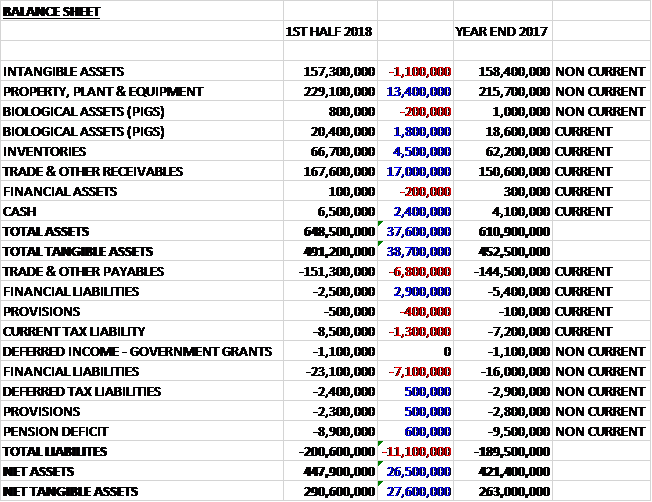

When compared to the end point of last year, total assets increased by £37.6M, driven by a £17M growth in receivables, a £13.4M increase in property, plant and equipment, a £4.5M growth in inventories, a £2.4M increase in cash and a £1.6M increase in the value of the pigs, partially offset by a £1.1M decline in intangible assets. Total liabilities also increased due to a £4.2M growth in financial liabilities, a £6.8M growth in payables and a £1.3M increase in current tax liabilities. The end result was a net tangible asset level of £290.6M, a growth of £27.6M over the past six months.

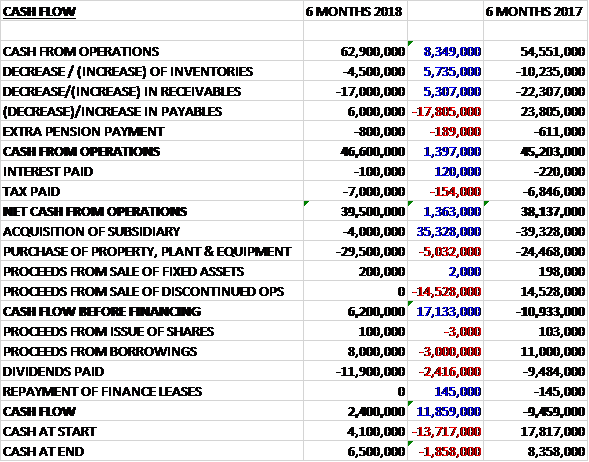

Before movements in working capital, cash profits increased by £8.3M to £62.9M. There was a cash outflow from working capital but an increased tax charge was offset by a reduced interest charge and the net cash from operations was £39.5M, a growth of £1.4M year on year. The group spent £29.5M on capex and £4M on an acquisition, relating to contingent consideration, to give a free cash flow of £6.2M. This didn’t cover the dividends of £11.9M and the group too out £8M of new loans to give a cash flow of £2.4M and a cash level of £6.5M at the period-end.

Fresh pork revenue increased by 26%. Excluding the contribution from Ballymena, like for like revenue growth was nearly 13%. Performance was comfortably ahead of the overall UK fresh pork market which saw volumes decline slightly. More recent market data has, however, been more encouraging with volume growth of 4% last quarter. Innovation has been the key driver of the positive trend with growth of meal kits and mid-week meal solutions supported by a strong AHDB TV advertising campaign. During the period the group also gained new listings including added value supper ranges and developed new processing techniques which have delivered significant eating quality improvements.

The Ballymena butchery hall extension was completed during the period resulting in capacity being increased from 8,000 to 12,000 pigs per week. Further investment is being made at the Hull facility to lift pig chill capacity and to upgrade the rapid chill system to improve yields. The group are also investing £4M in their Wayland operation to increase breeding and finishing capacity of premium pigs in response to customer demand.

Total export revenue grew by 30%, with a modest decline in sales to Far Eastern markets comfortably offset by a more than doubling of sales to other export markets which most notably include the US and Europe. Growth in these two markets reflected stronger volumes and higher prices resulting from Sterling weakness. Like for like export volumes grew by 19%. The UK pig price increased by 6% during the period, rising steadily through to the end of July before falling back slightly.

Convenience revenue increased by 17% reflecting the full contribution during the period of new business wins in the previous financial year. Again, growth was comfortably ahead of the overall market. Cooked meats sales were very strong reflecting the benefit of the new business wins. New product launches in the “Ready to cook” and “slow cook” ranges also helped underpin the strong growth. A further £7M of capex was made across the three cooked meats facilities during the period.

Sales of continental products were in line with the same period last year with higher prices, resulting from the weakness in Sterling, offsetting lower volumes following the loss of pizza toppings business with one retail customer. New business wins with other retail customers, including new platter range launches and pre-pack corned beef, boosted sales. The business continues to explore opportunities in the food service sector which offers good growth potential. Additionally the Woodall’s range of British charcuterie products continues to perform well with new listings secured in the period. The new £28M facility based in Bury is progressing to plan with completion expected in summer 2018. When finished the site will consolidate production from the two existing facilities, lift capacity by around 70%, add new capability and drive efficiency improvements on existing product lines.

In gourmet products, revenue increased by nearly 28% with all sub-categories delivering double digit volume growth. The overall market for these categories grew by 1% in volume terms but premium ranges were up by 9%. Strong sausage sales growth reflected the contribution from the new Butcher’s Choice business launched midway through the previous year together with new business wins launched in summer 2017. Both the Hull and Norfolk sausage facilities are gearing up for the peak Christmas trading period with two additional production lines installed in Hull.

New gammon and wet cure bacon business with one of the principal retail customers, secured in Q4 last year, helped drive strong bacon sales growth. Consumers continued to switch from standard tier lines into the premium ranges. Pastry sales grew strongly, reflecting the contribution from new business with a food to go customer launched at the start of the period. The business has also developed a range of frozen products for one of the group’s retail customers. These new business wins augmented continued growth with the site’s anchor retail customer. A strong new product development pipeline and full Christmas order book leaves the pastry business well placed moving into the second half.

The poultry business included the full contribution from Crown during the period with revenue up 27% and like for like sales growing 21%. The fresh and ready to eat chicken ranges categories continue to be the stand out performers in the wider UK meat protein sector, with market volume growth of 5% and 9% respectively. The Crown business continues to make progress. The management team has been strengthened and investment in the Weybread primary processing facility is driving efficiencies and lifting throughput. More birds are being portioned due to new contracts secured.

Sales of premium cooked poultry grew strongly in the period, reflecting underlying market growth and the launch of contracts with two of the group’s principal retail customers. Further lines have been added since these contracts were launched and looking forward there is a strong new product development pipeline to drive further growth.

The board has approved a £54M primary poultry facility in Suffolk with a further £13M associated investment to upscale existing milling and hatchery facilities. This facility is scheduled for completion in late 2019 and will double the existing capacity with further room for expansion. In July 2016 the group sold its shareholding in the Sandwich Factory.

Going forward, the board believe that the group is well positioned to deliver their expectations for the current year.

At the current share price the shares are trading on a PE ratio of 25.7 which falls to 22.8 on the full year consensus forecast. After a 15%increase in the interim dividend, the shares are yielding 1.5% which increases to 1.6% on the full year forecast. At the period-end the group had a net debt position of £16.7M compared to £11M at the end of last year.

Overall then this has been a good period for the group. Profits are up, net assets increased and the operating cash flow grew. The group is quite capex thirsty but despite this, a decent amount of free cash was generated, albeit not enough to cover the dividend. All aspects of the business seem to be performing well but with a forward PE of 22.8 and yield of 1.6% the shares are priced accordingly. Overall I’m comfortable with this investment.

On the 1st February the group released a trading update covering Q3. Like for like revenue was ahead of last year. Each of the group’s categories delivered growth, underpinned by a strong performance over the Christmas trading period. Total export sales were also well ahead. The UK pig price continued to ease during the period, ending the quarter at a similar level to that of a year ago and the downward trend is being reflected in selling prices. Overall though, trading in Q3 was slightly ahead of board expectations.

Construction on the new continental products facility based in bury is well advanced and progressing to plan with completion expected in H1 of next year. When finished the site will consolidate production from the group’s two existing continental products facilities, lift capacity by around 70%, add new capability and drive efficiency improvements on existing product ranges.

Plans for the new primary poultry facility in Suffolk continue to be developed, with construction expected to begin in Q1 next year. This facility, which is scheduled for completion in late 2019 will double existing capacity with further room for expansion. Net debt increased during the quarter, albeit it was below the level at the same stage of last year, reflecting the seasonal increase in working capital and ongoing capex.

Going forward, the board is confident in the prospects for the remainder of the year. This all looks fine, I continue to hold.

On the 12th February the group announced that director John Bottomley sold 8,000 shares at a value of £244K for “personal financial planning”.