Dewhurst has now released their final results for the year ended 2017.

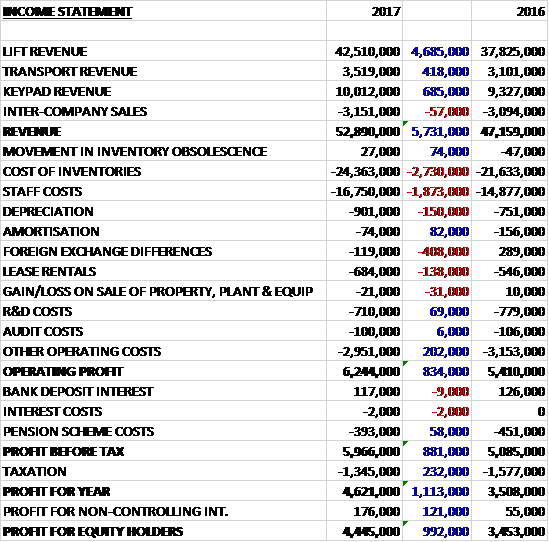

Revenues increased when compared to last year due to a £4.7M growth in lift revenue, a £685K increase in keypad revenue and a £418K growth in transport revenue. Cost of inventories increased by £2.7M, staff costs were up £1.9M and there was a £408K detrimental movement in forex but the operating profit remained £834K higher. There was a small fall in the cost of the pension scheme and tax charges reduced by £232K to give a profit for the year of £4.4M, a growth of £992K year on year.

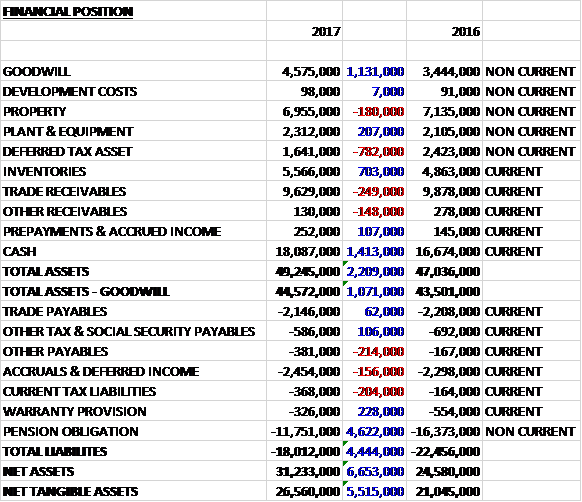

When compared to the end point of last year, total assets increased by £2.2M, driven by a £1.4M growth in cash, a £1.1M increase in goodwill and a £703K growth in inventories, partially offset by a £782K decline in deferred tax assets. Total liabilities declined during the year, mainly due to a £4.6M fall in pension obligations. The end result was a net tangible asset level of £26.6M, a growth of £5.5M year on year.

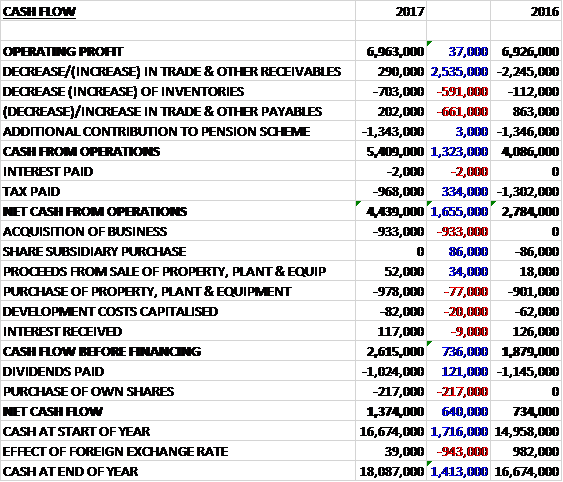

Before movements in working capital, cash profits were broadly flat at £7M. There was a cash outflow from working capital but this was less than last year and after tax payments were up £334K the net cash from operations was £4.4M, a growth of £1.7M year on year. The group spent £933K on an acquisition and £978K on capex to give a free cash flow of £2.6M. This easily covered the dividends of £1M and there was a positive cash flow of £1.4M for the year and a cash level of £18.1M at the year-end.

Overall, the real growth in sales this year came from the acquisition of P&R Liftcars (£2.2M) and the benefit from a weaker pound (£3.3M). The same two factors ensured the growth in profits, both contributing around £400K.

Dewhurst UK had a reasonable year but they were unable to continue the growth that they achieved last year. All regions, with the exception of Europe, showed slightly lower demand and they were also affected by a lull in production for projects in the Middle East. The board are confident that this lull is only temporary, however, and the New Year has started more positively with a number of delayed projects starting to move into production.

Deliveries of products for UK infrastructure projects have continued with the group’s products being used on the new Elizabeth Line in London. They have improved their manufacturing process and one key project has been to improve the flexibility of their push button pressel tooling. They can now mould all their ranges on their two pressel tools rather than just selective ranges. This has reduced the number of tool changes they need to carry out, reducing waste in terms of both time and materials.

It was another challenging year for Thames Valley Controls but the decline in sales has been arrested with the business showing a small increase. During the year they have gradually improved their production processes for the Ethos 2 controller. This will allow them to increase their capacity for this product line. They are investing in a new computer aided panel layout and wiring system that will streamline their engineering processes and will allow for automated transfer of information from engineering into production. Furthermore they recently completed the design and manufacture of four test simulators that will dramatically reduce the test time for an Ethos 2 panel.

The new features that are required to meet the EN81-20 standard have proved quite onerous but these have now been fully incorporated into the design and function of the Ethos 2 product line. During the year they have won and installed some major monitoring projects for both local councils and housing associations. Their new Non Invasive Monitoring systems has been particularly successful. The system interface allows them to provide full lift monitoring in closed-protocol lift control systems. It provides the benefits of full lift monitoring and breakdown identification to their customers irrespective of the make of lift. Through their online dashboard their customers can get instant breakdown advice and better management of repairs.

After significant growth last year, sales at Traffic Management Products grew once again this year but the increase was more measured with the first half of the year starting strong before demand tailed off during the summer months. Over the past year and a half they have launched a significant number of new products and have targeted additional export sales with particular success in the Far East. The business has decided to take control of their key supply chain processes such as moulding and lamination of their bollards and to integrate them into the business over the next two years.

At Dewhurst Hungary there was an 8% increase in sales but that growth was predominantly in the first half of the year and sales in the second half were disappointing. There has been a fairly significant reduction in demand for ATMs and this has impacted the business. There is a growing trend for contactless payments and associated with that there will inevitably be a reduced dependency on cash.

They have redesigned their stainless steel keypad which removes the key skirt that they have historically used which will make for a cleaner design and allow them to reduce the cost of the range.

In the Middle East, although it is early days, the group have already won a number of new projects and the outlook for the coming year is encouraging. They will predominantly source their products through the UK business and focus on fulfilling demand for the region for lift signalisation products. There is also an opportunity longer term to broaden the range of lift products marketed through the Middle East office.

In North America, sales fell back at Dupar Controls following some years of good growth. Despite the 6% fall in sales, however, they were able to improve their margins and closely control overheads which led to a year of record profits in Canada. They are looking to boost capacity in the business and to achieve this they are planning to reorganise the plant and invest in new manufacturing operations software that will help them better control their planning.

This was a very difficult year for Elevator Research and Manufacturing with sales falling sharply and significant losses being incurred. In the second half it became clear that they would need to restructure the business by mothballing the door and cab product lines and focusing solely on the core business of elevator signals. They completed the restructuring in the year and move into the New Year with a much more clearly targeted business and significantly lower overheads. They still believe that there are real opportunities for their products on the West Coast of the US and are working to resolve the challenges in the business.

The Australian market continued to be quite buoyant and all of the group’s Australian businesses showed solid growth. Australian Lift Components achieved the highest level of growth with strong demand for their signalling products. The business opened a new office in Brisbane which allowed them to better serve their customers in that area. Sales at Lift Material remained quite consistent throughout the year and the restructuring of the business into two divisions, elevators and escalators, has worked well, delivering growth for both divisions.

The group completed the acquisition of P&R Liftcars in early 2017. Based in Sydney, the business is similar to that of Dual Engraving. They design, manufacture and install custom lift interiors into lift cars in NSW and provide doors, entrances and other elements of steelwork for their lifts and escalators. Despite the Perth economy continuing to be somewhat soft, Dual Engraving grew their sales over the year. There are fewer major projects at the moment but there is still a steady base load of jobs. They are continuing to invest in new manufacturing plant to improve their processes and allow them to increase capacity and have just taken delivery of a new brake press.

Sales grew in Hong Kong by 16% to a new record level. This growth has been achieved by the sale of TMP products into the Hong Kong market. Sales of their lift products fell as the new property market softened but demand for lift products has shown signs of strengthening in the New Year.

Going forward, the weaker pound is benefitting the reported numbers but UK demand is more fragile at the moment and projects are subject to delay and deferral. Both these effects are at least partly caused by the uncertainty regarding Brexit so any progress in negotiations (or lack of) could materially affect future results.

Overseas demand in the lift market is more buoyant with North America, Australia and the Far East generally reasonably positive. The weaker demand for keypads in the second half has flowed through to the New Year, however and with contrasting significant positive and negative factors it is difficult to predict where the balance will lie.

At the current share price the shares are trading on a PE ratio of 11.4 which falls to 11.3 on next year’s consensus forecast. After an increase in the dividend the shares are yielding 2% which increases to 2.1% on next year’s forecast. At the year-end the group had a net cash position of £18.1M compared to £16.7M at the end of last year.

Overall then this has been a pretty decent year for the group. Profits grew, net assets increased and the operating cash flow improved with plenty of free cash being generated, although cash profits were flat year on year. The underlying performance isn’t quite as strong as this, however, as the growth in profits has come from the weakness of sterling and the acquisition, without which profits would have declined. The group seems to be struggling a bit with UK demand and some of the businesses in the US.

With a forward PE of 11.3 and yield of 2.1%, along with a load of net cash, these shares are not expensive and I really do like this company and the cautious management but I have a feeling the first half of the coming year might be a bit of a struggle and I am tempted to sell up.