Dechra Pharmaceuticals has now released its interim results for the year ending 2016.

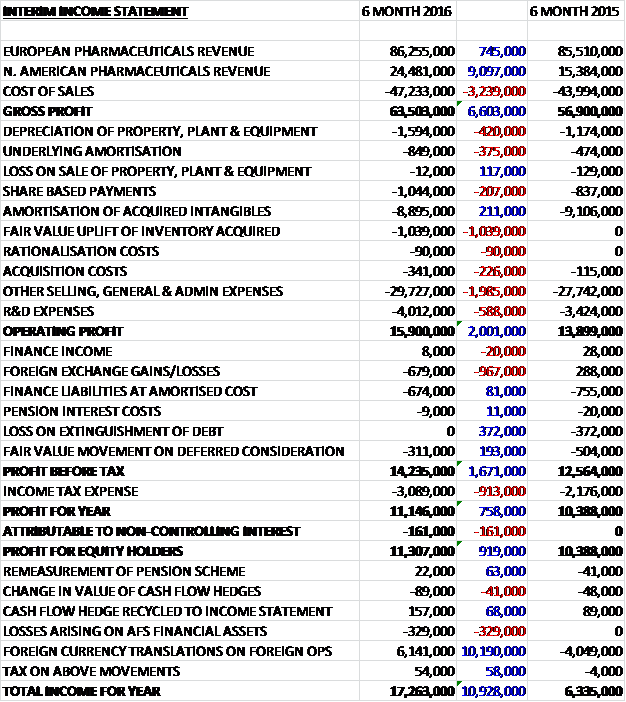

Revenues increased when compared to the first half of last year with a £9.1M growth in North American revenues, aided by a strong US dollar, and a £745K increase in European revenues which included the benefit of the Genera sales but an adverse effect of the weak Euro. Cost of sales also increased to give a gross profit £6.6M above that of last time. Depreciation was up £420K and underlying amortisation grew by £375K. We also see a £1M fair value uplift of inventory acquired through business combinations, which presumably pushed acquisition costs up, and other selling, general and admin costs which were up £2M. After a £588K growth in R&D expenses, the operating profit grew by £2M year on year. We then see a £967K adverse swing in foreign exchange levels, partially offset by no losses from the extinguishing of debt that took place last time, and a £193K improvement in the fair value movement on deferred consideration to give a pre-tax profit £1.7M above that of the first half of 2015. After tax increased by £913K, the profit for the half year came in at £11.3M, a growth of £919K year on year.

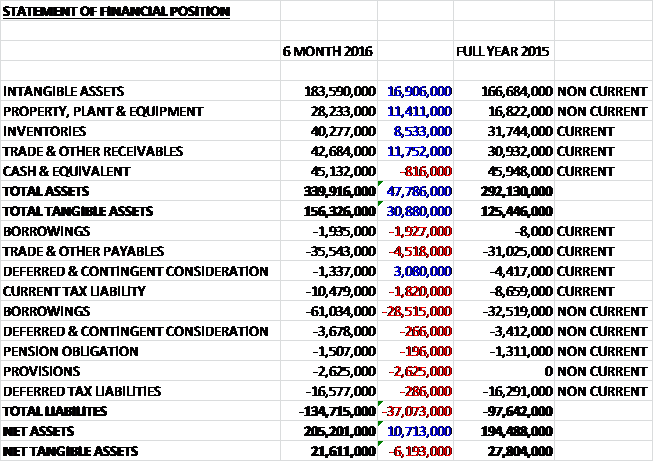

When compared to the end point of last year, total assets increased by £47.8M, driven by a £16.9M growth in intangible assets, an £11.8M increase in receivables an £11.4M growth in property, plant & equipment, and an £8.5M increase in inventories. Total liabilities also increased during the period as a £30.4M growth in borrowings, £4.5M increase in payables, a £2.6M growth in provisions, and a £1.8M increase in current tax liabilities were partially offset by a £2.8M decline in deferred and contingent consideration. The end result is a net tangible asset level of £21.6M, a decrease of £6.2M over the past six months.

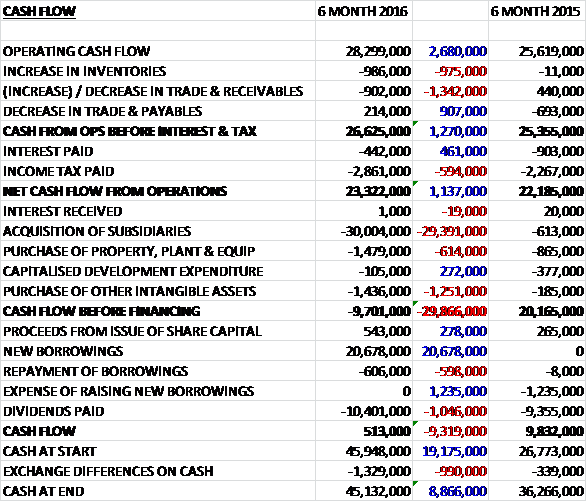

Before movements in working capital, cash profits increased by £2.7M to £28.3M. There was a modest outflow of cash through working capital to support the North American expansion and a higher tax payment was broadly offset by a decline in interest paid so that the net cash from operations came in at £23.3M, a growth of £1.1M year on year. The group spent £1.5M on property, plant and equipment along with £1.4M spent on intangible assets before they spent £30M on acquisitions to give a cash outflow of £9.7M before financing. The group still paid out £10.4M on dividends, however, so new borrowings of £20.7M meant that there was a cash flow of £513K for the half year period to give a cash level of £45.1M at the period-end.

The operating profit in the European pharmaceuticals division was £24.7M, a growth of £620K year on year. The growth was predominantly driven by a strong performance in companion animals with good sales in both the anaesthetic and endocrine therapeutic sectors. The introduction of Osphos into the UK, together with a repositioning of Equipalazone, contributed to the increase in equine sales. Osphos was also launched in Germany, France and the Netherlands towards the end of the period and will be launched into other European markets throughout the second half of the year.

Although there has been a continued decline of antibiotic sales in Germany, the group have delivered growth in farm animal pharmaceuticals in the period of 19% at a constant currency basis. This growth has been achieved through an increased penetration of target markets, a good performance in Poland which started trading in May, and the Genera acquisition which added 11% to growth. Two new farm animal antibiotics have been prepared for imminent launch in Europe and these products, together with a continued focus on increasing market share where they currently have a low base and gaining new registrations in the rest of the world, enhance the group’s future prospects in that area.

Diet sales declined by 2.3% at constant currencies over the period. This follows a difficult six months during which the group conducted a technical transfer of the products to a new supplier and the loss of a portion of their business with a large corporate account in Scandinavia. They have, however, seen signs of recovery in Q2 in several countries, including the largest market, France.

The operating profit in the North American pharmaceuticals division was £8.7M, an increase of £3.3M when compared to the first half of last year as the dermatology, endocrinology and ophthalmic ranges started the year strongly. Canada, which only started trading in the second half of last year, also contributed to the growth in revenues. Osphos has received good support from key opinion leaders within the US, and towards the end of the period, sales were strong and market penetration increased.

Sales of the Dermapet range reached the $20M annual total threshold in August which triggered the final milestone payment of $5M. The excellent growth in the endocrinology sector was again driven by Vetoryl which was enhanced by the launch of a new 5mg formulation which increases veterinarians dosing flexibility. During the period, expenses grew by 37% in North America as the group continued to expand their sales force in the US. Compared to the prior year, they have also funded two new subsidiaries in Canada and Poland. The R&D expenses have increased as they progress their pipeline.

In Western Europe there is a continued focus on prudent prescribing of antibiotics due to concerns about resistance. This trend is expected to continue in the region and has impacted the group’s farm animal business, particularly in Germany, but the rate of decline has slowed in Denmark and the Netherlands, where antibiotic use has reduced substantially in the past. The board believe their risk is minimal in other European territories where their market share is lower and their farm animal performance is stable.

The first half of the year saw some notable new product approvals. In September, Zycortal, a novel canine endocrine product for the treatment of Addison’s disease, received approval through the centralised process in all EU member states. The group are awaiting a new animal drug application in the US as all parts of the dossier were approved after the period-end. Following the successful registration of Osphos last year in the US and UK, approval was received in 19 EU countries in September for the product which treats Navicular Syndrome in horses.

The group have also had several successes in their farm animal portfolio in Europe with two new water soluble antibiotics, Solamocta and Phenocillin, approved in 17 EU states, and their existing antibiotic aerosol Cyclospray, extended into 12 new territories. Furthermore they have had several international approvals to enhance their geographic expansion including two canine products, Urilin in Australia, and Cardisure in Korea, and a farm animal antibiotic Soludox in Egypt. Although within the period they terminated an early stage project for canine ophthalmology, they continue to refill the pipeline and have started several new products in both farm animal and companion animal areas.

Geographical expansion is progressing well. In addition to the acquisition of Brovel which creates a foothold in Mexico, the Genera acquisition provides access to the smaller markets of Croatia, Slovenia and Bosnia. Furthermore a new start-up subsidiary has been established in Austria which started trading in January 2016. The subsidiaries in Canada and Poland, established in the prior year, are performing well with the latter being a major contributor to the reversal in trend of the farm animal business which returned to growth in the period.

Generics of Felimazole, Comfortan and Malaseb have entered the European market. In the first half of the year Malaseb sales have fallen by 5.8%, but the group’s defence strategies for the other two drugs have proved successful to date with European growth of 3% for Felimazole and 26% for Comfortan. During the period the group made forex transactional losses of £700K on trading activities and translational gains of £6.1M.

In August the group acquired 63% of Genera DD, a Croatian pharmaceutical business. By October they owned some 84% of the share capital of the business. The consideration paid was £26.8M in cash funded from current cash and debt facilities. The acquisition came with £17.5M of intangible assets and generated goodwill of £2.3M and in the four or so months since acquisition it contributed a pre-tax loss of £1.7M with an underlying operating loss of £200K. This acquisition gives the group an entry point into the fast growing poultry vaccines markets, broadens the EU farm animal business and extends the geographical reach in the Balkans. The integration so far is on track.

During the period the group also paid a further £300K contingent consideration relating to last year’s Phycox acquisition and £3.3M relating to the Dermapet acquisition that was contingent upon revenues exceeding $20M in any twelve month period. This was the final deferred consideration payment on this acquisition with a maximum further consideration of $3.2M outstanding on the Phycox transaction.

After the period-end, the group acquired Laboratorios Brovel SA, a veterinary pharmaceuticals company based in Mexico City. They paid $5M in initial cash consideration and a further $1M that is contingent on the business reaching registration milestones for Dechra’s products in Mexico. The book value of the net assets acquired was £1M and the business has a turnover of £2.6M. The board believes this acquisition will help open the significant Mexican animal health market to the group as well as offer the potential to access other Latin American Markets in the future. The initial focus will be to achieve registration of several existing Dechra products in Mexico.

Going forward, although the macro-economic conditions in Europe are uncertain and currencies could be volatile, trading for the second half of the year has started well and is in line with management expectations and they remain confident in their future prospects.

After an 8.4% increase in the interim dividend, the shares are now yielding 1.5% and this remains the same on the full year consensus forecast. The group had a net debt position of £17.8M at the end of the period compared to £3M at the same point of last year. Their revised borrowing facility comprises a £90M revolving credit facility and a £30M accordion facility committed until 2019.

Overall then, this was a strong six months for the group. Profits increased, despite neither acquisition being earnings enhancing yet; and operating cash flow improved with loads of cash generated before the acquisition. Net tangible assets did decline, however, as the group used hard cash to pay intangible assets related to the acquisition. The European business is performing strongly with companion animals doing well and farm animals improving following the new subsidiary in Poland. The launch of Osphos in much of Europe over the period should also be making a contribution. North America also performed strongly and the last contingent consideration for the Dermapet acquisition was finally paid during the period.

There are obviously some potential risks. The antibiotic prescriptions in Europe are still under pressure and generic drugs have been launched that are competing against some of the group’s important products, although in two of those cases they have not yet caused a decline in sales. In addition the recent acquisitions will require a lot of attention before they are contributing to results and the shares are highly rated. In conclusion, however, this is a quality business performing well with plenty of drivers of growth going forward and I am happy to continue holding.

On the 15th March the group announced the acquisition of Putney Inc, a developer of generic companion animal pharmaceuticals in the US based in Maine. In addition they have announced the placing of 4,398,600 new shares at £11 per share to raise £47.1M to part fund the acquisition. The total consideration being paid is £139M, payable in cash on completion (no pesky deferred consideration).

The acquisition accelerates the group’s North American strategy, potentially doubling their US business within their planning horizon and it is expected to be earnings enhancing in 2017 and materially earnings enhancing in 2018 and thereafter, on an underlying basis. It is expected that there will be a charge of £6M for one-off transaction and integration costs during the current year.

Putney currently markets eleven products, which have achieved significant market shares and continue to grow, in complementary therapeutic areas to Dechra, including pain management, anti-infectives, and dermatology. In addition, the business has a strong pipeline of ten complementary products which are expected to launch over the coming years. The business has achieved over 40% of all US companion animal generic approvals since 2012 and the outsource manufacturing either through a profit share arrangement or on a fee for service basis. In future the board believe it may be possible to manufacture in-house products in the pipeline which are not already set up with third parties.

Putney reported net revenues of $49.6M in 2015 but made a loss before tax of $1.7M with gross assets of $23M. The acquisition has been funded in part from an extension to the group’s existing revolving credit facility to £150M which means that net debt to EBITDA will increase to about 2.1 times immediately following the acquisition, falling to 1.9 times by the end of the year.

Unfortunately, as is common in these cases, members of the public are not entitled to participate in the placing. The shares, when issues, will represent about 5% of the existing share capital and the placing price of £11 per share represents a 5.4% discount to the closing mid-market price the day before, which is not too bad.

Overall then, this looks to be an interesting acquisition. Although the business is still loss-making, it seems as though the board are confident of turning a decent profit from it in future. It does look rather expensive and saddles the group with quite a lot of debt, but overall this seems to be a decent development.

On the 21st March the group announced that CFO Anne-Francoise Nesmes and her spouse sold a total of 3,100 shares at a value of £37K. Following the sale, her interest in the company is 39,502 shares.

On the 21st March the group announced that CFO Anne-Francoise Nesmes and her spouse sold a total of 3,100 shares at a value of £37K. Following the sale, her interest in the company is 39,502 shares.

On the 8th April the group announced that Tony Rice had been appointed as Chairman. He is currently the senior non-executive director at Halma having previously served as CEO at Cable and Wireless and Tunstall. Also, after six years in the role, Chris Richards is stepping down as non-executive director of the company with immediate effect.

On the 6th June the group announced that non-executive director Tony Rice purchased 20,000 shares with a value of £228K. This represents his first purchase.

On the 12th July the group released a trading update covering the year ended 2016. During the year, revenue growth in EU Pharmaceuticals increased by 5% at constant exchange rates (3% on actual rates). Including Genera, growth was 13% at constant rates. A solid performance in the Companion Animal Products and Equine portfolios together with a recovery in Farm Animal Products supported this growth. Whilst they have seen momentum in some of their markets, Diets have not yet fully recovered to their previous sales level following the supply problems. The growth in the Farm Animal division was driven by the new subsidiary in Poland, a slowdown of the decline in Germany and market share gain in countries where they had a low market share and are now increasing penetration. The launches of Osphos and Zycortal also contributed to the EU performance.

North America continued to grow at a significant rate with revenue increase of 37% at constant currency. The two months of trading at Putney added another 16% to the growth. These results were driven by increased market penetration of the Endocrinology and Dermatology portfolios in the US and the full year effect of the Canadian subsidiary.

The pipeline progress has been in line with board plans. A number of approvals were achieved throughout the year, including Zycortal, a novel endocrine product; four FAP products, including Solamocta and Solupen; and the first poultry vaccine, Avishield ND. Additionally they received several registrations in emerging markets.

The geographical expansion is accelerating with the acquisitions of Brovel and Genera and their solid progress in the recently established subsidiaries in Poland and Austria. The results also include the full year effect of the establishment of the Canadian subsidiary which started trading in January 2015.

Integration activities of the acquisitions are well underway. The reorganisation of Genera’s business is completed, the restructuring of Putney was conducted in the first week of integration and the new management team at Brovel is in place. Overall, trading in the acquired entities is progressing well.

The board remain confident in their future prospects and believe that the growth opportunities available to them should not be affected by the current market volatility and uncertainty. This all looks fine to me, I continue to hold.

On the 17th August the group announced the appointment of Richard Cotton as CFO. Richard joins from Consort Medical, where he is currently CFO but he won’t start until January 2017. In the meantime, the current financial controller, Septima Maguire, will be acting CFO.