Pan African Resources has now released its interim results for the year ending 2016.

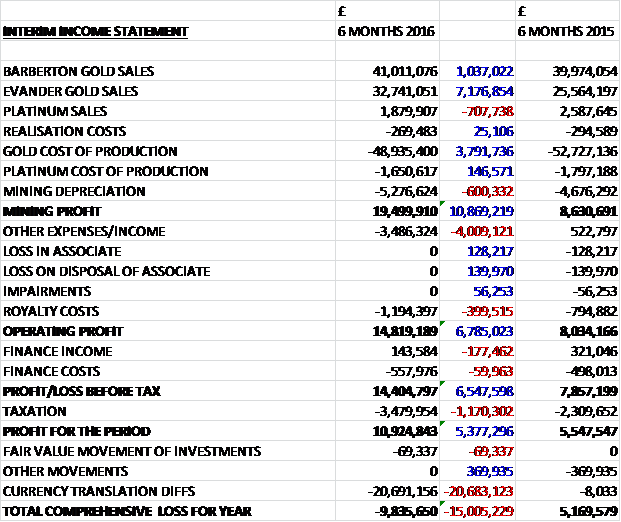

Revenues increased when compared to the first half of last year as a £707K decline in platinum sales due to lower tonnages processed and the lower price of platinum was more than offset by a £1M growth in Barberton gold sales as a result of improved gold sales, and a £7.2M increase in Evander gold sales. The cost of production decreased by £4M due to the depreciation of the rand (rand denominated costs increased) but mining depreciation grew by £600K to give a mining profit some £10.9M above that of last time. There was another expense of £3.5M compared to an income of £523K which at least partly related to gold price hedges in the first half of 2015, and royalty costs increased by £500K to give an operating profit £6.8M ahead. Finance income was down by £177K and there was a modest growth in finance costs so that after a £1.2M increase in tax, the profit for the half year came in at £10.9M, a growth of £5.4M year on year.

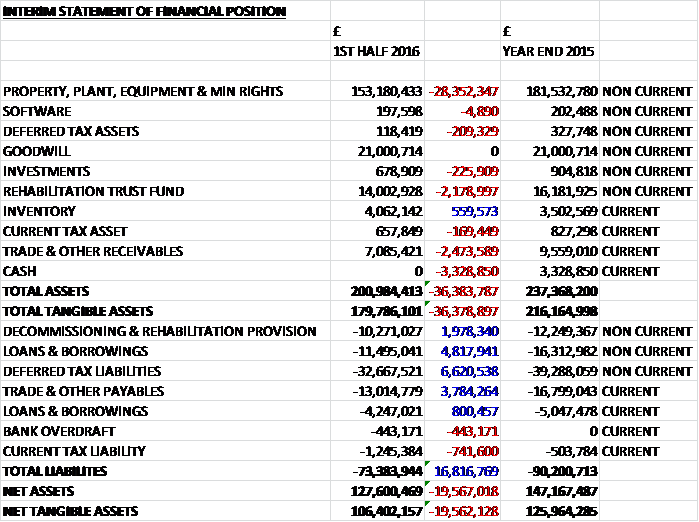

When compared to the end point of last year, total assets declined by £36.4M, driven by a £28.4M fall in property, plant, equipment and mineral rights; a £3.3M decrease of cash, a £2.5M decline in receivables and a £2.2M fall in the value of the rehabilitation trust fund due to the Rand depreciation. Total liabilities also declined during the period due to a £6.6M fall in deferred tax liabilities, a £5.6M decline in borrowings due to a decrease in the Evander Mines’ gold loan and the revolving credit facility, a £3.8M fall in payables and a £1.9M decrease in the decommissioning and rehab provision. The end result is a net tangible asset level of £106.4M, a decline of £19.6M over the past six months.

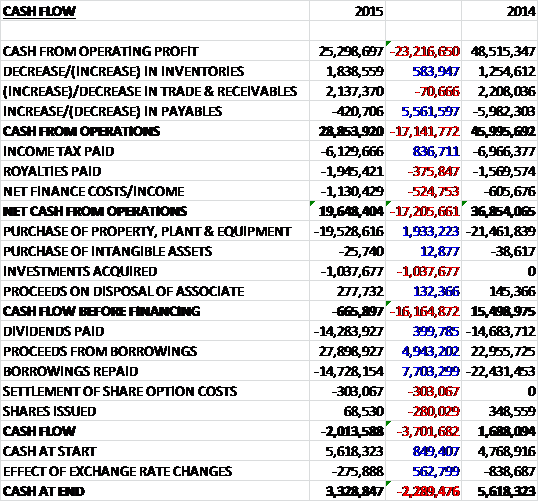

Before movements in working capital, cash profits increased by £8.4M to £19.5M. There was a modest outflow through working capital, although this was less than last time and after a growth in finance costs was offset by a fall in royalties paid, and tax increased by £924K, the net cash from operations came in at £14.1M, a growth of £8.4M year on year. The group spent £6.2M on capex relating to £2.3M at Barberton Mines, £400K on the BTRP and £3.5M at Evander Mines to give a free cash flow of £7.9M which did not cover the dividends of £9.3M so there was a cash outflow of £2.4M for the period and a cash overdraft of £443K at the period-end.

Overall gold sales increased by 17.4% to 101,797 ounces. All in sustaining cost per ounce declined from $1,165 per ounce to $908 per ounce and the average gold price received fell by 9.8% to $1,110 per ounce. The market platinum group metal basket price decreased by 20.4% to $859 per ounce but Phoenix’s average net basket price decreased from $894 per ounce to $641 per ounce after taking into account the terms of its off-take agreement with Lonmin.

The profit at Barberton mines was £9.9M, a growth of £1.4M year on year. The average underground head grade fell from 11.6g/t to 10.9g/t but the gold sold increased by 6.6% to 56,447 ounces and tonnes milled from mining operations was 10% higher at 139,430 tonnes due to the underground mining operations tonnes increasing to 133,890 tonnes and surface tonnes milled increasing to 5,528 tonnes. Gold sold from the BTRP increased by 9.6% to 12,830 ounces but tonnes processed decreased by 4.2% to 464,179 tonnes at a lower head grade of 1.3g/t which was set off by an increase in plant recoveries from 51% to 64%.

Excluding the BTRP, the cash cost per ounce decreased by 23% to $681 per ounce. This was mainly due to an increase in gold sold by 5.8% and a reduction in cost of production following a gold inventory credit adjustment amounting to ZAR23.5M as a result of 58Kg of unsold gold inventory concentrates held in the Fairview BIOX plant. Excluding this adjustment, the ZAR cash costs increased by 4.6%, although the USD cost was still lower due to the Rand depreciation. The BRTP’s cash cost decreased from $459 per ounce to $367 per ounce, mainly as a result of the Rand depreciation. The combined all-in cash cost decreased by 16.4% to $800 per ounce, once again due to the depreciation of the Rand.

The total cost of production increased by 0.9% on ZAR terms and was up 10.4% excluding gold inventory adjustments. Salaries and wages increased by 15.7% to ZAR219.3M due to an increase in the wage agreement settlement and a rise in production incentives and overtime due to the increased production. Mining costs increased by just 1% to ZAR58.5M due to the vamping contractor’s costs increasing, offset against cost controls. Processing costs decrease by 10.2% to ZAR29.1M as a result of lower plant repairs and maintenance costs. Engineering and technical services increased by 24% to ZAR39M with additional costs due to secondary support at Fairview to assist in accessing additional high grade pillars and corrosion maintenance in BTRP’s carbon in leach tanks.

The cost of electricity increased by 9.2% to ZAR52.1M which was lower than the National Energy Regulator’s approved rate increases due to improved electricity management of metallurgical plants and ensuring processing occurred mainly during lower peak tariff periods. Admin and other costs increased by 18.6% to ZAR19.8M as occupational accident and disease insurance increased, asset and bullion insurance costs increased, additional legal expenses were incurred, and license and software charges increased following IT upgrades.

From July, the life of mine was increased by a year to 20 years due to the down dip extension of the high grade 11 Block of the main reef complex ore body by a further 170 metres which resulted in an annual increase in the mine’s mineral reserves by 236,162 ounces. Total capital expenditure at the mine was maintained at the same level as year as maintenance capex increased and expansion capital declined with the ZAR900K being spent on the development of the Fairview ventilation raise borehole project to improve operating ambient temperatures.

Going forward, Barberton aims to maintain and increase levels of production by focusing on improving its tonnage throughput, while delivering on underground head grade in excess of 10g/t. Cost containment to avoid margin erosion is also a focus and will continue to be a priority.

The profit at Evander mines was £2.6M, an improvement of £3.9M when compared to the first half of last year. The underground head grade improved to 5.8g/t from 4.3g/t, principally due to mining at 8 Shaft’s newly established 25 level. The gold sold increased substantially, up 34.4% to 45,350 ounces due to underground mining operations increasing production to 36,370 ounces, while the Tailings Retreatment Plant provided an additional 3,708 ounces compared to zero last time and on an annual basis, the plant should add about 10,000 ounces of organic growth. Surface sources and surface feedstock material produced 5,272 ounces compared to 7,831 ounces following a reduction in the available surface tonnages to process.

Tonnes milled from underground sources increased by 1.5% to 200,942 tonnes and quantities treated by the ETRP amounted to 890,175 tonnes which comprised 729,085 tonnes from tailings sources and 161,090 of surface feedstock. Cash costs per ounce decreased by 31.4% to $903 per ounce, supported by the depreciating Rand and improved gold production. Total all-in cash costs declined by 41.8% to $1,046 per ounce as a result of increased gold produced and both ETRP plant construction costs and the redundancy cost that occurred last time.

The total cost of production increased by 14.1% to ZAR556.8M. Salaries and wages increased by 4.3% to ZAR247.8M as a result of the Chamber of Mines’ wage agreement offset by the implementation of a voluntary separation programme to reduce employee numbers. Mining costs increased by 8.3% to ZAR49.5M due to additional costs incurred on the No. 2 and 3 declines vamping recovery projects which produced an additional 820 ounces of gold. Processing costs increased by 11.7% to ZAR57.4M mainly as a result of acquiring surface feedstock material for ZAR4.4M. Engineering and technical costs increased by 24.7% to ZAR28.3M due to increased conveyor belt maintenance costs to maintain current efficiencies, as well as increased electrical repairs and maintenance costs to support the mine’s mature infrastructure.

Electricity and water costs increased by 19% to ZAR116M which included an increase for the ETRP, without this the 12.9% increase is broadly in line with Eskom’s tariff increase in the period. Security costs increased by 37.5% to ZAR7.7M to curtail criminal mining activities and protect surface assets. Admin and other costs increased by just 2.7% to ZAR25.6M and the gold inventory credit movements amounted to ZAR2M compared to none last time. Off-mine realisation costs nearly doubled to ZAR2.3M as a result of additional gold concentrates provided by the ETRP to Rand Refinery.

Effective from July, the life of the mine was 16 years compared to 17 years last year. Total capital expenditure declined from ZAR157.6M to ZAR71.9M with maintenance capex increasing by ZAR5.6M. Expansion capex was considerably lower than the corresponding period last year and ZAR1.9M was spent on development of 26 level compared to the capex on ETRP construction last time.

Going forward, the mine will invest in development capex to ensure that improved flexibility is achieved to mitigate the low grade mining cycles experienced in the prior year. The operational team will further focus on improving tonnages processed by the ETRP to reach its name plate capacity of 200,000 tonnes per month from tailings and surface feedstock material. Management will also continue to source toll-treatment material with a higher head grade than their ETRP tailings sources as long as it is economically viable, relative to treating their own tailings. They are also revisiting previous projects such as Evander South and the Evander 2010 Pay Channel with the objective of identifying viable options for the monetisation of these projects in light of the prevailing gold price.

The mining profit at Phoenix Platinum was just £837, a decline of £407K year on year. The profitability and cash generation decreased due to a curtailment in current arisings from International Ferro Metals’ Lesedi mine. Platinum production decreased by 4.6% to 4,493 ounces following a reduction in tonnage processed of 13.6% to 117,461 tonnes. This was a result of the drought constraining water resources to support re-mining activities at the Buffelsfontein and Elandsrakall tailings resource which gave rise to a loss of three weeks of production. The lower platinum group price environment further affected the operation’s profitability.

The all-in sustained costs declined from $636 per ounce last year to $608 per ounce during the period compared to an average price received that declined from $894 per ounce to $641 per ounce. The total cost of production increased by 7.2% to ZAR34.4M. Salary and wages increased by 5.3% to ZAR7.9M as wage increases were offset by lower production incentives. Processing costs increased by 5.5% to ZAR23.2M; electricity costs increased by 31.6% to ZAR2.5M which was above the NERSA tariff increase applicable for the period due to adjusting the milling coarseness of Elandskraal tailings, resulting in higher electricity consumption. Additionally, admin coasts increased by 14.3% to ZAR600K.

As of July, the life of operation remained steady at 28 years but in the event that the business rescue proceedings at IFMSA are finalised, and the Lesedi mine is put on care and maintenance indefinitely and the current platinum market conditions persist, there is a risk of an impairment of Phoenix’s carry value at the year-end. Total capex at Phoenix increased to ZAR800K.

During the period, Barberton mines entered into a short-medium term strategic hedge in July when the spot price of gold was ZAR440,000 per Kg, to protect its operational revenues against severe adverse price movements in the ZAR gold price. During the current year, the group recorded an unrealised cost collar derivative mark to market fair value adjustment of ZAR40.6M compared to a realised cost collar derivative income of ZAR44.8M last time. This was recorded under other income and expense.

The group is completing a definitive feasibility study to assess the merits of starting construction of the Elikhulu project. Elikhulu can potentially treat slimes at a processing capacity of up to 12M tonnes per annum and at a headgrade of 0.28g/t from the Winkelhaak, Leslie and Kinross tailings storage facilities. The total mineral resource for the project is 165M tonnes at 0.28g/t, equivalent to 1.5M ounces with a life of mine of 14 years. It is estimated to yield about 50,000 ounces of gold per annum in the initial eight years of production while treating the Kinross and Leslie storage facility and then approximately 38,000 ounces upon processing the Winkelhaak tailings storage facility.

Significant work has been performed on evaluating the Evander South project and progressing it to a preliminary economic assessment level. The project team is assessing the capital costs associated with the various mine designs that would provide the most efficient and cost effective manner of accessing the orebody. The project is a potentially attractive mining opportunity whereby the Kimberley reef could be exploited at shallow depths starting at 300 metres below the surface. It has an estimate mineral resource of 4.9M ounces relating to 20.1M tonnes at a grade of 7.7g/t.

In June the group entered into agreements to acquire the Uitkomst colliery. It is located near the town of Utrecht in KwaZulu Natal and is a high grade thermal export quality coal deposit with metallurgical applications. The consideration for the acquisition is the equivalent to about £8.9M at current exchange rates. It is an existing operational mine and the acquisition is expected to be earnings and cash flow enhancing with a coal resource of 25.7M tonnes of which 22.1M tonnes can be classed as measured or indicated. The area also has additional exploration potential and the mine currently sells about 400K tonnes of coal per annum to local and international customers.

The acquisition will be funded from an existing revolving credit facility and internally generated cash flows. The group has also received credit committee approval by Nedbank for £3.8M general banking facilities for the Colliery’s working capital purposes but the acquisition still remains subject to approval by the Department of Mineral Resources. The group’s exposure to coal, through this acquisition provides a natural hedge against an anticipated increase in energy prices in South Africa. It is not a divergence from the group’s strategy and precious metals focus. The life of mine is measured at 28 years, the coal price achieved was $52 per tonne, the sustaining capital per year is £350K and approximate profit per year is £1.4M. The group has committed £8.7M during the year to Oakleaf and Shanduka for the acquisition.

The group is well positioned to produce about 200K ounces of gold and 9K ounces of platinum group metals. The net debt was at the end of the period was £15M compared to £25.4M at the same point of last year. The shares are currently yielding 4.3% which is forecast to remain the same next year.

Overall then, this has been a fairly good period for the group. Profits were up, as was operating cash flow but although a decent amount of free cash was generated, this was during a period of low capex and it did not cover the dividends paid. Net assets did decline but this was due to the depreciation of the Rand rather than anything more sinister. Overall, the group managed to get a price of $1,110 for its gold sold with an all in sustaining cost of $908 which shows they are profitable at these levels.

The profit at Barberton mines increased during the period due to more ore being mined. The $800 per ounce all-in cash cost looks good to me. The Evander mine turned a profit during the period compared to a loss last time as the grade of ore improved. The all in cash costs of $1,046 per ounce still look rather high, though, mainly due to the ETRP construction costs so this should come down hopefully. The Phoenix Platinum operation is just about breaking even and with pressures including the low platinum price, the IFM business rescue proceedings and the drought affecting water usage, we are likely to see an impairment here and I am wondering if the venture has a future.

The colliery acquisition is an interesting one, if the profits are to be believed it looks like a canny acquisition that offers a hedge against one of the big appreciating costs in South Africa, the price of electricity. I must admit I am a bit reticent about investing in a coal miner at the moment but this seems to be a one-off purchase. The other big, appreciating cost is that of staff wages and this must be carefully watched going forward if the group are to keep their margins intact.

With a dividend yield of 4.3%, these shares do offer adequate reward but as with any stock of this nature, there are operational and country risks to take into account, not to mention the future movements in the stock price. It could be a decent hedge against a potential downturn in the markets though.

On the 23rd March the group announced that MD of Barberton Mines, Casper Strydom, purchased 750,000 shares at a value of £91K which represents his maiden purchase of any decent amount.

On the 4th April the group announced the completion of the acquisition of Uitkomst Colliery from Oakleaf and Shanduka. The group settled the transaction’s revised purchase consideration of £8.2M in cash at the end of March and the total net purchase consideration, including working capital acquired, was £7M compared to the £9.3M previously announced.

The colliery will be implementing a BEE transaction which will result in additional 9% black ownership which will be held by broad-based trusts and by a strategic entrepreneur’s trust. The BEE transaction will be financed by the colliery on a notional basis with this funding accruing interest linked to the prime interest rate. The transaction results in limited dilution to PAF and 80% of dividends issued to the BEE shareholders will be retained to repay the notional funding over a period of ten years. Over the past eight months, the run of mine coal mined was 412KT, the saleable coal produced was 278KT and the wash yield was 67.5%. The life of mine of the operation is estimated at 28 years.

Previously the group announced that they had agreed to acquire Standard Bank’s 16.9% interest in Shanduka Gold. Shanduka’s only assets are its 23.8% interest in Pan African. The other shareholders are Mabindu at 49.5% and Jadeite at 33.6%. In early June, Jadeite exercised a right whereby the group made an offer to acquire their Shanduka shares. Therefore the group will acquire their shares on the same terms as the SBSA transaction.

The SBSA and Jadeite transactions are expected to be concluded simultaneously at £23.9M which will be settled in cash from the group’s existing reserves and from some placing proceeds. A placing of 111,711,791 Pan African shares will be issued to certain shareholders and institutional investors at a price of 14.25p per share, a premium of 5.1% on the month average price prior to the announcement. The placing will raise about £15.9M and the shares will represent about 5.7% of the enlarged share capital.

Shanduka is the group’s black economic empowerment main partner and the transaction will give the group a 49.9% direct interest in it. Implementation of this transaction will result in the group consolidating all of their shares held by Shanduka so the net effect will be a reduction of 324,646,268 shares in issue. This is a complex deal but it seems as though the main rationale is to retain as much profit as possible and still comply with the BEE rules.

On the 15th June the group announced that Barberton Mines GM, Casper Strydom, sold 747,613 shares at a value of £123K leaving him with just 6,387 shares. This is certainly not a very bullish sign!

On the 19th July the group announced that Samancor Chrome was selected as the successful bidder to acquire IFMSA. PAF has reached an agreement with Samancor that allows for the assignment of the TTA to Samancor. The agreement further clarifies a number of the provisions contained in the TTA.

Even though the agreement does not guarantee current arising feedstock to the group, which will be dependent on the manner in which they use the IFMSA assets, it places them in a position where they will continue operations under similar conditions to those prior to the business rescue proceedings. It also ensures that their operations and interests are safeguarded. They do have alternative sources of feedstock, which was processed during the business rescue proceedings.

From the above, I am not sure if there is a huge amount of clarity on what will actually happen but hopefully things will continue as normal.

On the 3rd August the group released a trading update for the year ended 2016. The EPS at constant currencies for the period is expected to be some 157% higher than last year at around 29.5c although a depreciation in the value of the South African Rand meant that the actual EPS was up “just” 114% to around 1.37p.

The share price increased significantly during the period which resulted in an increase in the group’s cash settled share option costs which amounted to £3.7M. Earnings increased due to the robust operating performances from Barberton and Evander. The improved operational performance was supported by an increase in the gold price. The earnings were further enhanced by consolidating the Uitkomst Colliery results for the last three months. Phoenix Platinum production was adversely impacted by the curtailment of current arisings following IFM being placed into business rescue, however.

In all, Barberton saw production increased by 7% to 113,281 ounces; Evander increased production by 31% to 91,647 ounces but Phoenix saw production fall by 19% to 8,339 ounces. Uitkomst produced 136,102 tonnes of coal during the period.

At the year-end the group had a net debt position of £19.4M compared to £18M at the end of the prior year despite the £10.2M investment in Shanduka and the £8.3M spent on Uitkomst. By the end of July, net debt had reduced to £14.3M. Following receipt of a positive high level assessment of the Elikhulu tailings retreatment project, the group has conducted a definitive feasibility study on the project, the results of which will be available in November.

This all seems rather positive to me and I continue to hold.