Dechra Pharmaceuticals has now released their interim results for the year ending 2017.

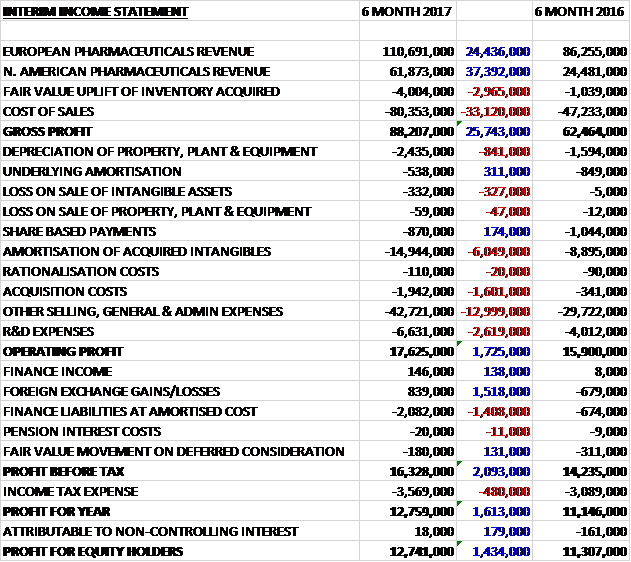

Revenues increased when compared to the first half of last year with a £37.4M growth in North American revenue (£25M attributable to the Brovel and Putney acquisitions) and a £24.4M increase in European revenue. Cost of sales also increases to give a gross profit £25.7M above that of last time. Depreciation was up £841K, the amortisation of acquired intangibles increased by £6M, acquisition costs grew by £1.6M, R&D expenses increased by £2.6M and other general costs grew by £13M which meant that the operating profit was £1.7M higher. A favourable movement in forex hedging generally offset a £1.4M growth in finance liabilities and after tax charges increased by £480K the profit for the period came in at £12.7M, a growth of £1.4M year on year.

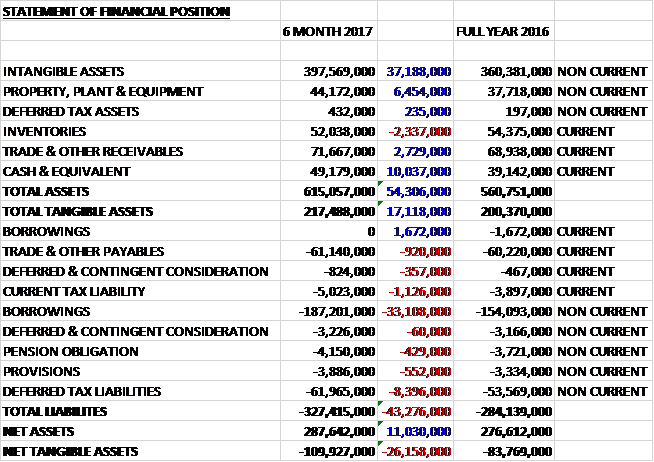

When compared to the end point of last year, total assets increased by £54.3M driven by a £37.2M growth in intangible assets, a £10M increase in cash, a £6.5M growth in property, plant and equipment and a £2.7M increase in receivables, partially offset by a £2.3M decline in inventories. Total liabilities also increased during the period due to a £31.4M growth in borrowings and an £8.4M increase in deferred tax liabilities. The end result was a net tangible asset level of -£109.9M, a deterioration of £26.2M over the past six months – I would like to see this debt stabilise now.

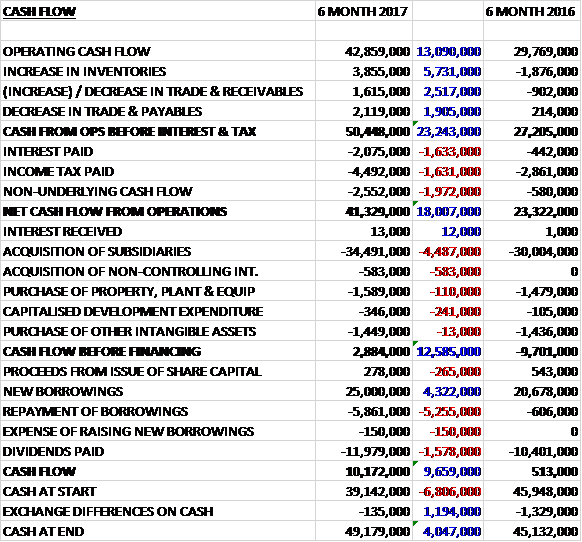

Before movements in working capital, cash profits increased by £13.1M to £42.9M. There was a cash inflow from working capital so despite interest payments increasing by £1.6M, tax payments growing by £1.6M and non-underlying cash flow increasing by £2M the net cash from operations was £41.3M, a growth of £18M year on year. The group spent most of this, £34.5M, on acquisitions along with £1.6M on fixed assets and £1.8M on intangibles to give a free cash flow of just £2.9M. This didn’t cover the £12M paid out in dividends so the group took out a net £19.1M of new borrowings to give a cash flow of £10.2M and a cash level of £49.2M at the period-end.

Not including acquisitions and forex movements, overall EU revenues increased by 5.9% and North American revenues were up 10.2%.

The operating profit for the European division was £30.8M, a growth of £6.1M year on year on revenues that increased by 12.5%. This was driven by companion animal growth of nearly 13% with strong performances from the majority of therapy areas. The core underlying EBIT growth was 6.9%. Several key products grew significantly, especially Cardisure, an anaesthetic, and Zycortal, an endocrine product launched last year.

Equine core sales increased by 8%, predominantly driven by European launches of Osphos. For the first time in three years, there was a growth from the pet diet range Specific which increased sales by 1.7%. This follows the transfer of the products into a new manufacturer and the reformulation of several lines in the range. The previously reported issue of a reduction in palatability of a number of therapeutic cat diets post reformulation has now been resolved with the reintroduction of the products to the market.

Farm animal product sales from the core business increased by 2.5% despite the planned reduction in production for the injectable antibiotics due to modifications in the manufacturing suite. The decline in sales reported last year in Germany due to antimicrobial resistance concerns slowed considerably. The issue remains that antibiotic sales continue to be under pressure, however, especially with recent government focus in Denmark and the UK.

Third party manufacturing revenues declined by 14.3% in the period predominantly due to one major account reducing its demand and by the rationalisation of a number of low value third party contracts to prioritise production of Dechra’s own products. The overall segment revenue benefited from an £11.3M contribution from the acquisitions of Genera and Apex.

The operating profit for the North American division was £18.1M, an increase of £9.4M when compared to the first half of last year with revenues more than doubling. The core underlying EBIT growth was 5.8%. Core sales of both companion animal and equine products increased revenue by 10.2% (at constant currency) despite the fact that a Levothyroxine based product was withdrawn from the market by the FDA. Zycortal and Vetivex were both launched in the US in the period. Equine sales grew by 67% driven by an excellent performance from Osphos.

Both the Mexican and Canadian businesses performed well. The overall segment revenue benefited from an outperformance by Putney. Market penetration of their products improved from the additional focus provided by Dechra’s sales and marketing team. Furthermore there was a one off benefit from opening new sales channels for these products resulting in a £3M uplift from stock sold into the distribution chain.

During the period the group received FDA approval for a generic antibiotic Amoxi-clav. This product was the first major approval from the Putney pipeline following the acquisition and the board expect additional approvals from Putney in H2. The group also received approval for Altidox, a new farm animal generic water soluble antibiotic in 13 EU countries. Osphos received approvals in Canada and Australia. Registrations were also gained from the Genera pipeline including Genoxytab, a farm animal intra-uterine antibiotic in four EU countries, and Canihelmin, a canine de-worming tablet in six EU countries. In addition, Apex received its first registration since acquisition for a liquid formulation of Benazepril, a companion animal cardiac medication. A number of new pharmaceutical product ideas have been screened and it is hoped that at least one will be introduced into the pipeline before the end of the year.

The implementation of the Oracle ERP solution has fallen behind schedule with “go-live” now expected in H1 2018. There are no fundamental issues with the project but detailed work flows and test plans identified the need to extend the implementation timetable.

In October the group acquired Apex Labs, a veterinary pharmaceuticals company based in Australia. The group paid £34.2M in cash and the acquisition generated goodwill of £9.8M. For some reason the results are reported in the EU segment and the business generated profits of £600K in the period. If the acquisition had been completed at the start of the year, it would have generated profit of £1.6M. The principal reason for the acquisition is to give the group direct access to the Australian companion animal and equine markets which they currently operate through partners. During the period the group purchased a further 1.74% of Genera for a consideration of £580K. They now own 95.13% of the business.

Despite the uncertainties surrounding Brexit and the reduction in antibiotic use, current trading is meeting management expectations. The core portfolio continues to grow, the product pipeline is delivering new products and good progress has been made on the rationalisation and integration of the recent acquisitions. The board are confident in their future prospects and the expectations for the full year.

At the current share price the shares are trading on a PE ratio of 120.5 but this falls to 28.4 on the full year consensus forecast – this is clearly not a value stock. After an increase in the interim dividend the shares are yielding 1.1% which increases to 1.2% on the full year forecast. At the period-end the group had a net debt position of £138M compared to just £17.8M at the same point of last year and £116.6M at the year-end.

Overall then this has been another period of progress for the group. Profits were up as was the operating cash flow, although not much in the way of free cash was generated and net liabilities increased again. The core business saw decent growth of 6% in Europe and 10% in North America with the performance in the former driven by strong companion animal and equine sales. Most products have done well in North America with Osphos proving particularly popular.

Although there was core growth, there is no doubt that the driver for most of the growth has been the recent acquisitions, however, and I do hope the group is not overextending itself – I would like to see some consolidation. The results have also been flattered by the weakening of Sterling and with a forward PE of 28.4 and yield of 1.2% there really is no room for error. This is a great company and one I am holding on to for now but the valuation is starting to look a bit full to me.

On the 21st March the group announced that executive director Anthony Griffin sold 3,500 shares at a value of £59K. He now owns 64,320 shares in the company.

On the 31st March the group announced that it had entered into a long term IP licensing agreement with Animal Ethics, an Australia-based company focused on developing ethical pain relief products in animal health. The agreement gives the group the right to sell and market Tri-Solfen for all animal species in all markets except Australia and New Zealand. Under the terms of the agreement the group has agreed to make milestone payments on signing, upon the first and second anniversaries of the agreement and on the first two major species approvals in markets with significant potential. Additionally a royalty will be paid on all net sales.

Separately the group has acquired 33% of the parent company of Animal Ethics for a total consideration of £11.1M. The business has developed a topical product which anaesthetises, relieves pain, controls bleeding and protects against infection. Its primary use is in sheep, pigs and cattle but other opportunities have been identified in horses and companion animals. It has already been registered for sheep in Australia with annualised sales of $4M. The development process is underway to register this product in global markets, with initial focus being for pigs in Europe and pigs and cattle in the US with the first registrations targeted for 2020.

This seems a decent acquisition for the future but I do help the group aren’t overextending.

On the 22nd June the group announced that CEO Ian Page sold 134,500 shares at a value of £2.6M. This is a substantial sale and is disappointing to see, suggesting he thinks they may have peaked.

On the 6th July the group released a trading update covering the full year with trading in line with management expectations. Overall reported revenue increased by 28% at constant currency driven by growth from the core portfolio, good market penetration from recent launches and the performance of acquisitions made last year.

European revenues were up 7% with non-contract manufacturing revenues increasing by 9% driven by a strong performance from the core companion animal business and strong contributions from the Geneva and Apex acquisitions. Revenue from food producing animal products saw a second successive year of growth despite the ongoing pressure to reduce antibiotic prescriptions.

The North American segment saw revenues up 93% and includes a good performance from the core companion animal and equine portfolios in both the US and Canada. Putney delivered a strong performance, benefiting from integration of the sales and marketing efforts of the enlarged Dechra team and Mexico also delivered good growth.

As announced last year, the group received FDA approval for a generic antibiotic Amoxi-clav which was the first major approval from the Putney pipeline following acquisition. Several other products received approval in numerous countries including Mexico, Australia, South Korea, Thailand, Canada and the EU.