Avingtrans has now released their interim results for the year ending 2017. Following the disposal, management is reorganising the business into two core sectors: Energy and Medical. In Energy the group supply industry proves modules – in particular nuclear waste storage containers, as well as a variety of other niches in the renewable energy sector. In Medical they supply cryogenic vacuum vessels to markets such as MRI, nuclear magnetic resonance, proton therapy and related sectors.

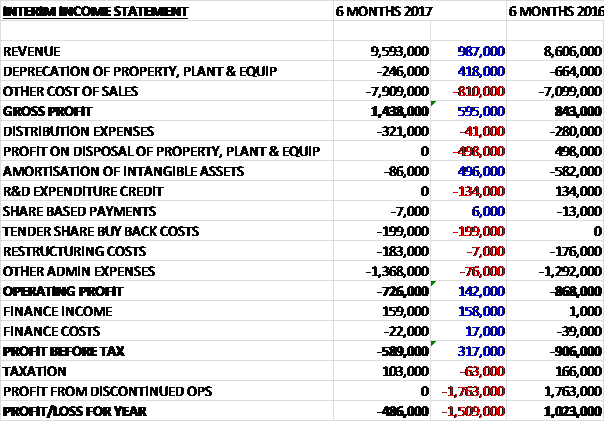

Revenues increased by £987K when compared to the first half of 2016 and although depreciation was own £418K, other cost of sales increased by £810K to give a gross profit £595K above that of last time. There was no profit on the disposal of fixed assets which brought in £498K last time but amortisation was down £496K. There was also no R&D credits which were £134K last time and there were £199K of tender share buy-back costs with other admin expenses up £76K to give an operating loss £142K lower. Finance income grew by £158K but tax credits were down £63K to give a loss for the period of £486K, a £254K decrease year on year.

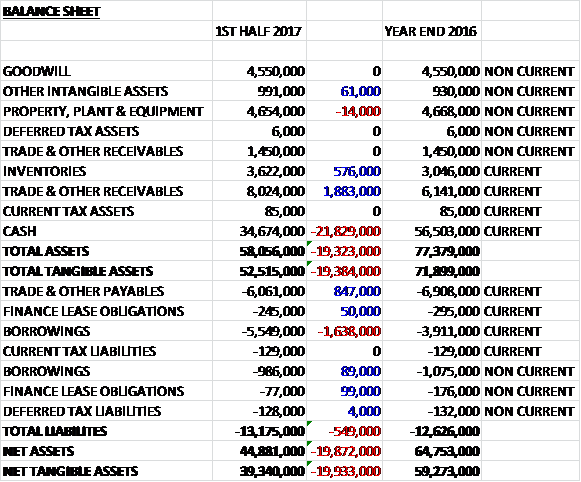

When compared to the end point of last year, total assets declined by £19.3M driven by a £21.8M fall in cash, partially offset by a £1.9M increase in receivables and a £576K growth in inventories. Total liabilities increased somewhat during the period as an £847K decline in payables was more than offset by a £1.6M growth in borrowings. The end result was a net tangible asset level of £39.3M, a decline of £19.9M over the past six months.

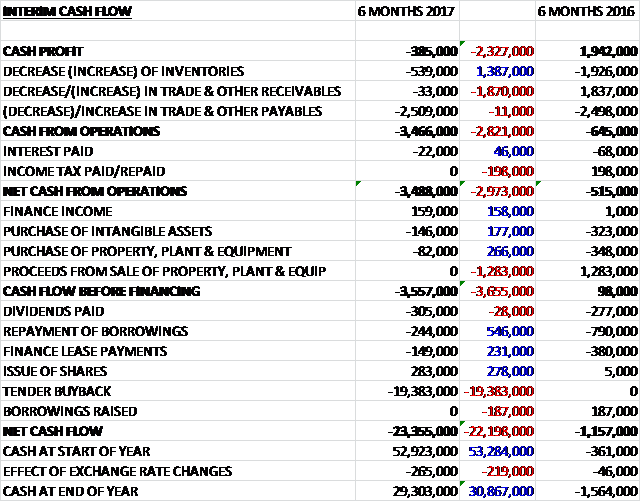

Before movements in working capital, cash losses reversed by $2.3M to £385K. There was a cash outflow from working capital and no tax receipts so there was a net cash outflow of £3.5M from operations. The group received £159K in finance income and spent £82K on intangible assets along with £146K on property, plant and equipment to give a cash outflow of £3.6M before financing. The group also spent £305K in dividends, £149K on finance leases, £244K in loan repayments and £19.4M on the tender buyback which meant a cash outflow of £23.4M and a cash level of £29.3M at the period-end.

The Energy and Medical business had an operating loss of £49K, an improvement of £379K year on year.

In Metalcraft, business with Siemens and Cummins in the UK was again steady. The contract with Sellafield to produce 3M3 boxes for the storage of intermediate level nuclear waste is progressing to plan. They have made good progress with facilities refurbishment and pre-production tests. The production set-up and prototyping phase will continue in the current year with series production expected to start in the 2018 calendar year. The total number of boxes required is now expected to be more than 70,000 over the entire programme life worth an estimated £3BN. The Chinese unit saw results improve with the preparation for the new contracts with Bruker and Wuhan for NMR vessels.

At Maloney Metalcraft, the low oil price continued to affect the business in the period, though this has largely washed through, with a limited restructuring completed, to stabilise their position in the new $50 a barrel oil reality. The gas project contracts with Samsung and JGC Gulf International progressed substantially in the period. Both have taken longer to complete than previously anticipated, however, due to customer originated programme changes. Work also commenced on the EDF contract.

Crown had a steady, if subdued, first half. The FET carbon abatement trial in Wales concluded successfully and they are working to turn this application into a product of the future with FET. This technology promises to make small to medium diesel generators clean. Other prospects with FET are also progressing, albeit slowly.

Composite Products’ performance in the period improved markedly as they began volume deliveries to Rapiscan. The second half performance will be similar and they expect further volume growth in the next year. Whitely Read Engineering has completed overspill activities from Metalcraft and Maloney.

The business is expected to be second half weighted, having won important projects last year which are in the process of ramping up – notably the pre-production phase of Sellafield 3M3 Box operations at Metalcraft. So far, this is progressing positively with Sellafield recently approving the first prototype unit. Crown is also expected to enjoy a stronger second half with new projects expected to convert to sales during this period.

After the period-end the group acquired a 94% majority stake in superconducting magnet and cryogenic systems company Spacy Cryomagnetics for a total consideration of £347K (although the group are also repaying an outstanding loan of £468K). The business designs, manufactures, tests and installs superconducting magnet systems for a range of applications, as well as providing consultancy services to companies such as Siemens and Rolls Royce. In addition, it will broaden the group’s capability in the supply of vacuum vessels and cryostats for science, space and astronomy projects. Last year the business made a profit of £41K.

A principal focus going forward will be further acquisitions in order to utilise the £28M of available cash. The group existed last year with almost £60M of LTAs signed and have since signed a Wuhan contract worth £9M and an extended contract with Siemens.

At the current share price the shares are trading on a PE ratio of 154.9 which increases to 226.1 on the full year consensus forecast – clearly these shares are being valued on what the group is going to do with that pile of cash. Net cash reduced from £51M to £27.8M following the tender offer which returned £19.4M to shareholders. After a 9% increase in the interim dividend, the shares are yielding 1.6% which remains steady on the full year forecast.

Overall then this is a company that seems to be in transition. The losses did improve during the period but the operating cash flow worsened, not helped by working capital movements. The various businesses seem to be ticking along with Maloney sill affected by the low oil price and progress at Crown seems to be rather slow. The group are winning some interesting looking contracts, however, and the second half is looking like improving. The shares are clearly priced for the anticipation of what the board are going to do with the cash, however, as the current business can’t really justify this rating despite the vital Sellafield contract. Overall I also continue to hold in anticipation.

On the 31st March the group announced they had made a bid for Hayward Tyler PLC, although there is no further information.

On the 26th June the group announced that they had secured a contract extension with Sellafield. The contract is worth an additional £11M in revenue to be spread over the three years to 2021. Overall, although revenue was slightly behind management outlook, they closed the year with pre-tax profits marginally head of internal expectations and net cash of £26.2M. They also reported a strong current order book for the energy and medical division.

On the 30th June the group announced the acquisition of Hayward Tyler. Under the terms of the scheme, shareholders will be entitled to receive one new share for every 4.755 scheme shares. This represents a premium of 14.7% to the Hayward Tyler closing price of 47p per share and the number of new Avingtrans shares expected to be issued is 11,533,278 which will result in scheme shareholders owning 37.6% of the total share capital of the enlarged group. This is not yet a done deal though so watch this space!