Fairpoint provides debt solutions and legal services, particularly for individuals experiencing personal debt problems but has branched out into more broad legal services this year through the acquisition of Simpson Millar. When the group was created it was dependent on IVAs as their only substantial income stream but this has been expanded in recent years with a growing number of debt management solutions, claims management and legal services. It is listed on the AIM exchange and its operations are located wholly within the UK.

IVA consists of group businesses Debt Free Direct and Clear Start, the core debt solution brands. The primary product offering of these brands is an Individual Voluntary Agreement which consists of a managed payment plan providing both interest and capital forgiveness and results in a consumer being debt free in as little as five years. Debt Management consists of the brand Lawrence Charlton. DMPs are generally suitable for consumers who can repay their debts in full, if they are provided with some relief on the rate at which interest accrues on their debts. They could take more than five years to complete and offer consumers a fixed repayment discipline as well as third party management. Claims Management activities involve enhancing the financial position of customers through PPI and other claims and offering a switching facility on personal outgoings such as utility costs. Legal Service activities provide a range of consumer focused legal services with the main lines being family, personal injury and clinical negligence through 13 offices around the UK.

For IVA fees, revenue is recorded to recognise gross income during the life of the IVA based on the cost of the work to date as a percentage of the total cost of services to be performed. They are discounted to reflect the fair value of cash flows recoverable. Over the life of the IVA the actual cash flows of the case in excess of fair value at recognition are recognised through finance income (unwinding of discount). The group also receives fee income for work performed for both Scottish and self-employed clients who require trust deeds or IVAs from other providers. In this instance, IVA income is recognised once a contractual obligation is incurred by the IVA provider accepting the referral.

The group received income in relation to claims management activity, principally for refunds of PPI in relation to its current client base. These fees and commissions are recognised when the claim has been settled by the creditor. In debt management, revenue is recognised on a cash receipt basis reflecting the proportion of work performed. Initial fees are recognised once a customer has made their first contribution to the plan and subsequent fees are recognised on receipt of funds into the plan. In legal services, revenue is recognised as it is earned over time and the group assesses the extent to which it considers it has the ability to recognise revenue based on the likelihood of recovery on a particular case. Services provided to clients that have not yet been billed are recognised as legal services revenue within trade and receivables. This all looks sensible although I suppose there is margin for error in the recognition of the legal services revenues.

Impairment provisions against trade receivables arising from the breakage of IVA payment plans are recognised when there is objective evidence, such as significant delay in payment, that the group is unable to collect all of the amounts due.

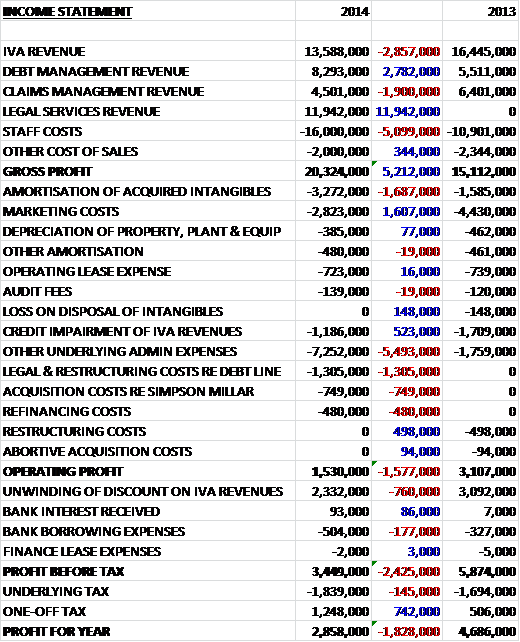

Fairpoint has now released its final results for the year ended 2014.

Overall revenues increased year on year as a maiden contribution of £11.9M from the legal services division and a £2.8M increase in debt management revenue was partially offset by a £2.9M decline in IVA revenues and a £1.9M fall in claims management revenue. Cost of sales also increased, which included a higher staff cost (not sure how much of those staff costs actually are cost of sales) to give a gross profit some £5.2M ahead of last year. We then see a big fall in marketing costs along with a £523K decline in credit impairments of IVA revenues but there was a £1.7M increase in the amortisation of acquired intangibles and an increase in other underlying admin costs along with some one-off expenses relating to the restructure of debt line and acquisition costs of Simpson Millar to give an operating profit £1.6M below that of 2013. Finance income fell year on year with a £760K decline in the unwinding of the discount on IVA revenues and an increase in borrowing costs before a lower tax bill meant that the profit for the year was £2.9M, a fall of £1.8M year on year.

When compared to the end point of last year, total assets increased by £21.3M driven by a £4.8M growth in goodwill, a £5.3M increase in acquired back books, a £5.4M growth in unbilled legal services income and a £5.8M increase in trade receivables. Total liabilities also increased during the year due to a £9.9M growth in bank borrowings and a £4.6M increase in contingent consideration to give a net tangible asset level of £25.3M, a decline of £5.3M year on year. For the tangible assets I have discounted goodwill, software development and customer relationships but kept the other intangible assets as I reckon they might be worth something.

Before movements in working capital, cash profits fell by £846K to £8.1M which became £7.9M after working capital movements before an increased interest cost, partly relating to refinancing costs, and a reduced tax bill meant that net cash from operations stood at £5.7M, a decline of £323K year on year. This was enough to cover the capital expenditure, including software development along with the purchase of debt management back books but was not enough to cover the acquisition so before financing, the cash outflow stood at £7.7M. The group then took out nearly £10M in new borrowings which enabled them to pay the dividends of £2.6M to give a cash outflow for the year of £491K and a cash level of £2.4M at the year-end.

Market conditions for the group’s debt solutions remain challenging. Whilst the volume of new IVA solutions in the country increased to 52,190 from 48,881 last year, the group has found that these volumes have been driven from customers with lower disposable incomes which has resulted in lower fees. These market conditions are likely to continue until the bank rate increases adversely affect the financial circumstances of home owners who typically have higher incomes. In the sector, a rigorous regulatory agenda has been driven by the FCA which is likely to result in both change and further consolidation in the market. As with all firms operating within the sector, the group has traded under an interim regulatory permission but has submitted its application for full regulatory permission which is expected to be processed in 2015.

Pre-tax profit at the IVA business was £3M, a decline of £600K when compared to last year. In light of the market conditions outlined above, the group has focused on profit margin maintenance through tight cost management which meant that margins remained at 25% during the year. Revenues reduced largely as a result of fewer incepted cases as the group continues to avoid exposure to fee levels which it considers uneconomic. The total number of fee-paying IVAs under management at the end of the year was 17,628 compared to 19,337 this time last year, the number of new IVAs written reduced from 4,491 to 2,716 and the average gross fee per new IVA was £3,437, up from £3,239 last year.

The pre-tax loss at the Debt Management business was £316K, although this included exceptional costs of £1.3M, without which the profit would have been £1M which was broadly flat on the profit recorded in 2013. Three DMP back books were acquired during the year and the total number of DMPs under management increased by 62% to 25,462 as a result of this. The pre-tax profit at the Claims Management business was £1.1M, a fall of £1.2M year on year. Claims levels, largely relating to PPI reclaim activity from existing IVA clients have reached maturity while those from the growing number of debt management clients are still under development. As anticipated this resulted in a reduction in claims revenues and profitability during the year but expertise in the acquired Simpson Millar provides support for further development of more sustainable forms of claims activity.

The pre-tax profit at the Legal Services was £548K which included £749K of exceptional items, without which the profit would have been £1.3M. This was the first year that the division has been trading but represents good growth on the same period of last year. Good progress is being made on detailed integration work streams in areas including sales, marketing and support services.

There were a number of one-off costs this year which included £700K of costs relating to the acquisition of Simpson Millar, £500K of costs associated with the refinancing of the debt with AIB, and £1.3M of transactional and restructuring costs in relation to the acquisition of Debt Line.

On the 16th June the group acquired Simpson Millar, a customer-focused legal services company with services that include family, personal injury and clinical negligence. The group paid a total consideration of £12.7M that included cash of £6.1M, shares at a value of £2M and contingent consideration of £4.6M. The acquisition came with intangible assets of £5.3M and generated goodwill of £4.8M. Since the acquisition the business contributed £1.6M to pre-tax profit which seems like a good acquisition to me. Also during the year the group acquired the Debt Support Company which comprised a DMP back book, for a cash consideration of £1.3M; the Money Debt and Credit DMP back book for £2.7M and Debt Line Topco for £3M which also included a DMP back book. The board have indicated that they are targeting further value enhancing acquisitions in 2015

There is now some susceptibility to interest rate rises with a 0.5% increase reducing profit by £48K. The group entered into a banking facility with AIB Group which expires in May 2019. The new committed facility, which has a five year term, comprises a £12M revolving credit facility and an £8M term loan. The term loan was used to finance the initial cash consideration of the acquisition of Simpson Millar with £5M repayable within five years and the remaining £3M repayable at the end of the five year term. The long term loan has an interest rate of 2.85%+LIBOR and the credit facility has 3% + LIBOR, which actually seems like quite a lot to me.

The main operational risks include the potential for regulatory change with some of the services coming under the regulation of the insolvency act; underlying economic conditions such as interest rates, unemployment and consumer debt levels; and the potential for customers to default on plans. On the latter point, fees on new IVA cases are based upon a budgeted percentage of defaults based on historical experience but there is a risk, that through external factors, the rate of default is higher than planned (unemployment and disposable incomes are particular factors that can affect this).

Going forward, the group will benefit from a full year of trading from the legal services platform which should provide a good growth stimulus. The market conditions in the IVA segment will remain challenging with a continued focus on margin management but the board expect the development of PPI claims through the DMP clients to mitigate the effects of the maturing IVA claims activity so they expect to make good progress in 2015.

At the current share price the shares trade on a PE ratio of 24.3 including the one-off items and amortisation of acquired intangibles (the ratio is 9.4 when these items are discounted). This reduces to a very cheap-looking 8.7 on next year’s consensus forecast. After a 7% increase in the total dividend, the shares are currently yielding 4% which increases to 4.3% on next year’s forecast which again, seems pretty decent. At the year-end net debt stood at £7.6M compared to a net cash position of £2.8M at the end of last year. There is also £8.9M of future operating lease payments off the balance sheet.

Overall then this has been a bit of a difficult year for the group. Profits were down, not helped by the debt line restructuring and acquisition costs; net tangible assets fell due to increased levels and borrowing and operational cash flow declined when compared to last year. The main issue is that the fees being received for IVAs have been pushed down due to the lower disposable incomes of people hitting difficulties. This has meant that the group has taken on less business this year as fees become uneconomical and this has a knock on effect on the amount of commission earned in the claims management business.

The group have taken some interesting measures to combat this problem though, they have purchased more DMP back books which will boost the debt management division and should provide more impetus to the claims management division, replacing some of the lost commissions relating the IVA customers. More importantly, though , they have acquired a legal services business which already seems to be generating decent profits and offers another interesting division to the group, and one which should help mitigate declines in other areas. The forward PE ratio looks cheap and the dividend yield of over 4% also looks tempting. I am thinking of taking a position here.

On the 3rd August the group released a trading update covering the first half of the year. Overall trading has been materially ahead of the same period of last year and in line with the board’s expectations reflecting a strong contribution from the legal services business. In that division, Simpson Millar performed well and is now the group’s largest source of income and have made some acquisitions in this area (more on that below). Market conditions remained difficult in the IVA market, however, with volumes of new IVA solutions in the country falling by over 23% in Q1 2015 but the group are sensibly being cautious about not writing uneconomic business despite the pressure to do so.

Revenues in the DMP division were broadly flat year on year which largely reflects the absence of acquisitions in the area as the group favours capital deployment towards the legal services business because the evolution of the DMP market remains unclear. The claims management activities were also broadly in line with last year as good growth from the in house claims management services offset a reduction in IVA related claims activity. At the period end net debt stood at £5.2M compared to £7.6M at the end of last year which shows some decent cash generation.

At the same time the group has announced the acquisition of Colemans, comprising Colemans-CTTS and Holiday Travel Watch, for an initial consideration of £9M and a potential contingent consideration of £7M. The initial consideration consists of £8M in cash and £1M in Fairpoint shares while the contingent consideration consists of two payments of £3.5M based on the financial performance of Colemans and the achievement of certain integration targets for 2016 and 2017. It is split 50/50 in shares and cash and is expected to be self-funding given the hurdles set which is very nice to hear.

Colemans is a provider of consumer focused legal services with particular expertise in volume personal injury, volume conveyancing and travel law. In the last year it made pre-tax profits of £2.3M and is expected to be immediately earnings enhancing to the group. The acquisition will be funded out of existing financial resources but to ensure appropriate funding for the group following completion, they have extended the current five year debt facility with AIM from £20M to £25M. Immediately following the acquisition, the net debt of the group is expected to be £13.2M.

To me this seems like a good acquisition. Given the profitability of the business and the fact that the contingent consideration will be self-funding, the initial price of £9M looks a great entry point. I have decided to buy some shares in the company.

Having gone no-where in the past year or so the shares seem to have broken out.