Keller is the world’s largest independent ground engineering specialist. Their services are used across the construction sector in infrastructure, industrial, commercial, residential and environmental projects. Piling involves the installation of structural elements to transfer foundation loads through weak soils to stronger underlying ground. The group offers a wide range of piling and earth retention systems including diaphragm walls and marine piles. Ground improvement techniques are used to prepare the ground for new construction projects and to reduce the risk of liquefaction in areas of seismic activity. Common soil stabilisation techniques include a combination of vibro-compaction with stone, concrete or lime columns as well as soil mixing and injection systems.

Anchors, nails and minipiles are used to provide temporary or permanent solutions for a wide range of stability or support problems and are often used to underpin or stabilise buildings, slopes and embankments. Speciality grouting strengthens target areas in the ground and controls ground water flow through rocks and soils by reducing their permeability. It is applicable to both new construction projects and to repair and maintenance work. Other applications include excavation support, settlement control and geo-environmental services to protect adjacent ground from contamination. Post-tension cable systems are used to reinforce concrete foundations and structural spans, enhancing their load bearing capacity by applying a comprehensive force to the concrete, once set. Suncoast’s post-tension systems are used in foundation slabs for single family homes and, in the commercial high rise sector, in concrete structural spans and beams.

The group also specialises in providing instrumentation and monitoring solutions for a wide range of applications. They provide and install a wide range of instruments and then provide repeatable data presenting it to their clients. About half of the work the group undertakes is piling and earth retention, with about 20% in ground improvements, 10% anchors, nails and minipiles, 10% speciality grouting and 9% post-tension concrete.

The group is the market leader in North America and operate from locations across the US and Canada. Hayward Baker offers ground engineering solutions across both counties. In the US, Case, McKinney and HJ are heavy foundation specialists and Suncoast provides post-tension cable systems. In Canada, Geo-Foundations specialises in micro piling, ground anchors and speciality grouting services and Keller Canada offers a broad range of piling solutions. The EMEA division has operations across Europe, the Middle East and Africa along with a developing business in South America. The group operate as Keller across these regions except for in Sub Saharan Africa where they operate under the Franki brand.

The group offers a wide range of foundation services in Asia and they are well established in Singapore, India and Malaysia where they predominantly trade as Keller. In Australia, Frankipile, Vibro Pile and Piling Contractors offer a range of piling services; Keller ground engineering offers specialist ground improvement and geotechnical solutions; and Waterway specialises in foundations for and the maintenance of wharves, jetties and other marine structures.

Keller has now released its final results for the year ended 2014.

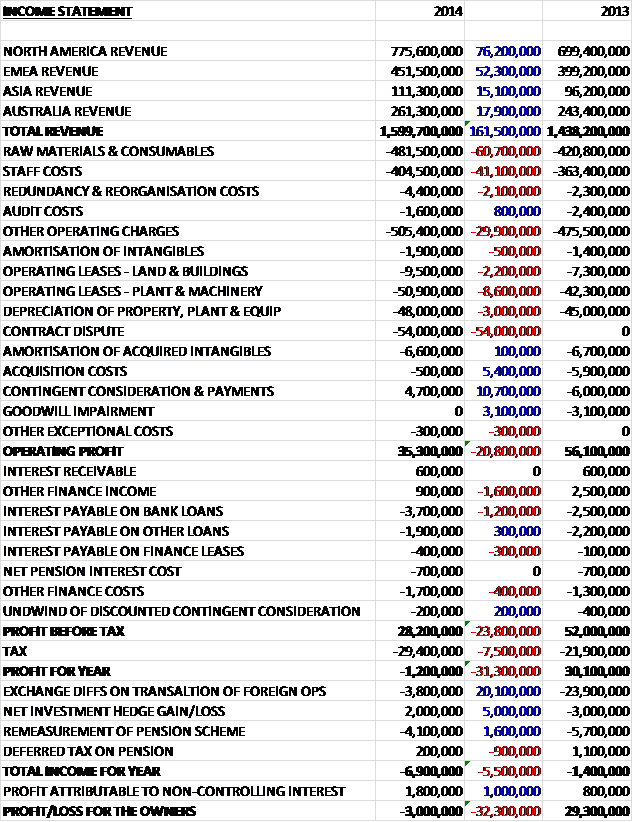

When compared to last year, total revenues increased by £161.5M driven by growth in all markets as the contribution from acquisitions was partially offset by a £9.3M adverse movement in foreign exchange. The cost of raw materials and consumables increased by £60.7M and staff costs grew to £41.1M. We also see a £2.1M increase in reorganisation costs and a £29.9M hike in other operating costs along with large increases in operating leases and depreciation. There was a general increase in non-underlying expenses as a £54M charge relating to a contract dispute partially offset by a £5.4M reduction in acquisition costs and a £10.7M positive swing in contingent consideration payments to give an operating profit some £20.8M lower than last year at £35.3M. After finance charges, which included less “other” finance income and more interest on the loans the profit before tax was £28.2M which was entirely wiped out by the £29.4M tax bill to give a loss for the year of £3M, a negative swing of £32.3M year on year.

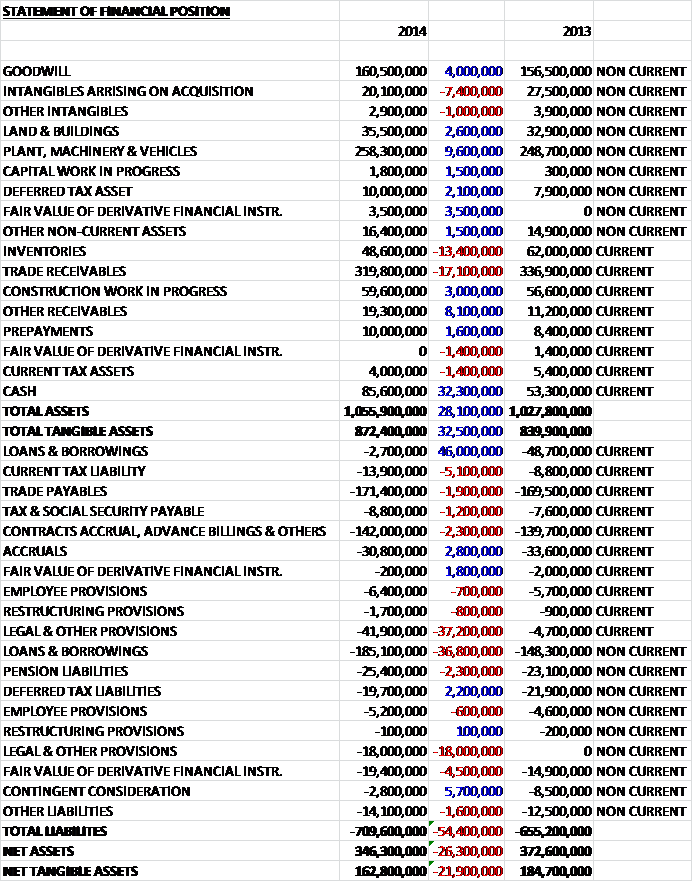

When compared to the end of last year, total assets increased by £28.1M to £872.4M driven by a £32.3M increase in cash, a £9.6M growth in plant and machinery, an £8.1M increase in other receivables and a £4M growth in goodwill, partially offset by a £17.1M fall in trade receivables, a £13.4M decline in inventories and a £7.4M fall in intangibles associated with acquisitions. Liabilities also increased during the year as a £55.2M increase in legal provisions, a £5.1M growth in current tax liabilities and a £4.5M increase in derivative financial liabilities (which stands at a substantial £19.4M) was partially offset by a £9.2M fall in loans and borrowings and a £5.2M decline in contingent consideration to give a net tangible asset level of £162.8M, a decline of £21.9M year on year.

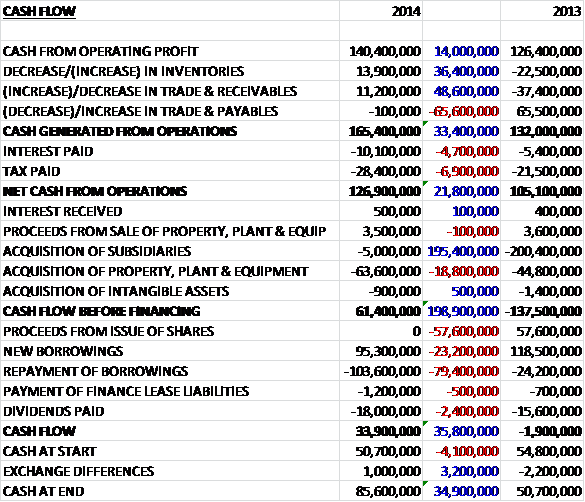

Before movements in working capital, cash profits increased by £14M to £140M. This was further boosted by decent falls in inventory levels and receivables before a higher interest charge and tax cost meant that net cash from operations stood at £126.9M, an increase of £21.8M year on year. This comfortably covered the £63.6M spent on property, plant and equipment along with the nominal £5M spent on acquisitions to give a free cash flow of £61.4M. The group then repaid a net £8.3M in loans and borrowings along with £1.2M in finance leases and after £18M was spent on dividends the cash inflow for the year was £33.9M and the cash levels at the year-end stood at a decent £85.6M. This is actually a pretty good performance, although that future legal payment is something to remember.

In the US, expenditure in private non-residential construction increased significantly for the second year with good market growth in most segments. The year also saw a return to growth in public expenditure on construction with spend up 2% after four years of decline. In Canada construction activity in the Western Canadian resources markets remains subdued but demand in the commercial and infrastructure segments is holding up well. Conditions for most of the group’s European markets remain challenging, particularly in Southern Europe but there are some reasonable prospects in Poland and Austria despite the overall markets being relatively quiet. Demand for the group’s services in Germany remains flat but the UK has returned to steady, albeit slow, growth.

There are some good opportunities in the Middle East but the market remains very competitive, and the market in South Africa has picked up. Whilst there are some exciting opportunities elsewhere on the continent, a number of them are in the oil and gas arena and their timing is uncertain. Construction expenditure in the group’s Asian markets remains generally robust. There are a number of significant infrastructure projects in Singapore and the Malaysian construction market is buoyant while in India, the group are continuing to see signs of increasing confidence after a couple of relatively slow years.

In Australia, construction expenditure across virtually all segments, including the resources sector, has been subdued for some time and there are no significant signs of this changing in the short term. The exception has been in LNG, where the group has won and performed a number of large projects, including the Wheatstone project, although the foundation works for the LNG plants under construction are now effectively complete. Whilst there are some significant infrastructure projects on the horizon, these are unlikely to come to fruition in 2015.

In North America like for like revenues increased by 11% and operating profit increased by £8.3M to £59.9M as conditions continued to improve in the group’s largest market and reflecting improved profitability in the US foundation contracting business along with a solid contribution from the Canadian businesses. The US businesses had a strong second half of the year as construction activity continued to gradually improve across the country.

The largest North American business, Hayward Baker, finished the year strongly. Its business model of performing a wide range of small to medium sized contracts across a broad range of products benefited from better conditions across the market. In addition to this, there have also been an increasing number of larger contracts performed in recent years. The largest contract undertaken in the year at a value of £36M was the I-635 highway expansion project in Dallas where the business is installing earth retention systems for new high-occupancy managed lanes.

Good progress has been made on the Elliott Bay Seawall project in Seattle, a project valued at £25M, where the business is performing jet grouting to depths of 85 feet to provide seismic stability and foundation support for the repair and maintenance of a 0.7 mile section of the seawall. Hayward Baker also worked with the group’s piling business based in Miami to deliver projects at Oceana Bay Harbour and One Ocean with augercast, wet soil mixing, sheet piling and tie back anchor technology. This is an example of combining the presence of one company with the products and solutions of another to give an advantage in the marketplace.

Other piling businesses, Case and McKinney performed well in the year. McKinney had a good broad based result across the southern and eastern states and Case, which undertakes larger contracts, worked on projects such as the foundations for a mixed use high rise building on the Chicago River and the installation of catenary poles on an Amtrak high speed rail line in the North East. Suncoast continued to experience improving profitability despite the slight softening of the single family home market in the summer. The high-rise business performed particularly well on the back of more commercial developments and a significant increase in multi-family home starts.

In Canada the group merged their Toronto based geotechnical business, Geo Foundations, into the larger Keller Canada business which led to some cost savings in the Toronto area and has resulted in a more focussed business in eastern Canada. After a disappointing first half, the results in the country improved in the second half with a full year revenue of around C$190M and an operating margin of about 5%.

Like for like revenues in the Europe, Middle East and Africa region increased by 5% year on year with operating profit nearly doubling to £12.9M. Margins increased by 1.2% but remained razor thin at 2.9%. Despite the continued challenging markets in Europe, the group improved their performance through a focus on cost control, risk management and careful contract selection. The Polish business had a particularly good year, much improved on last year as the infrastructure market offered some good opportunities despite a competitive backdrop. Germany also reported a good result as it continues to adapt to the difficult climate in which it operates. The UK business successfully completed its large projects at Crossrail and Victoria Station.

After a difficult winter-affected first half, the Austrian business picked up in the second half and finished the year ahead of 2013. Work performed during the year included a technically complex project at the Semmering railway tunnel in the south of the country. After the year-end, the Austrian business announced another large infrastructure rail project, a major £23.1M project on the Koralm railway line between Graz and Klagenfurt. The results were not as good in Southern Europe with the French market weak and business remaining very challenging in Spain and Portugal, with the Iberian business returning a small loss on revenues 20% lower than last year.

Competition in the Middle East remained tough but the group increased both its revenue and profit from the region. This performance was aided by a good result in Saudi Arabia and a number of contract wins in Qatar where, from a standing start, they are building a reputation for reliability and quality. Franki Africa performed in line with expectations in its first year as a Keller subsidiary. The integration has been completed and a number of technology workshops have been held to introduce Keller’s grouting and ground improvement technologies to the region. They have already performed some jet grouting jobs in South Africa. Elsewhere on the continent the group has undertaken significant contracts in a number of African countries, notably Algeria and Ghana.

The group have expanded their sales network to cover the key markets in Latin America: Sao Paulo and Rio in Brazil, Chile, Peru, Panama and Mexico. The business is now well established in Brazil and elsewhere they have performed a number of small projects involving small diameter techniques, piling and ground improvement works.

In Asia, operating profit fell by £700K to £8.3M despite revenues increasing as the margin fell from 9.4% to 7.5%. This was due to a major project that was won this year at a lower than average margin. The Malaysian business had a good year operating in a strong construction market. During the year they further expanded their piling business in the country and established a presence in Johor, a province neighbouring Singapore which is currently benefiting from substantial industrial and commercial investment. In August the group acquired a small Malaysian driven piling business, Ansah, broadening their product offering in the region with the group now offering a full range of foundation services and civil works.

In Singapore, Resource Piling completed the major Sengkang hospital project ahead of schedule and on budget. The project included a number of different technologies such as piling, diaphragm wall construction and micro tunnelling. After the year-end the group was awarded a major contract at Changhi Airport totalling £28M that comprises vibrocompaction of the ground as part of the land penetration works for a major expansion at the airport. The Indian business had a much improved performance in the year and prospects for 2015 apparently look encouraging. The group completed a number of large design and build LNG related projects to schedule using both bored piling and ground improvement techniques.

Operating profits in Australia were broadly flat year on year, increasing by just £100K to £15.7M as a result of the weakening Aussie dollar, and margins declined from 6.4% to 6% as last year benefited from the conclusion of a major project. Waterway Construction had a successful year working on contracts such as the Brisbane City Council wharf upgrade programme and the Overseas Passenger Terminal in Sydney Harbour. The other Australian businesses, however, found the year more challenging, mainly due to the subdued state of the market.

The piling for the onshore LNG processing plant at Wheatstone, the group’s largest ever project, is almost complete with 24,000 piles delivered. With the challenging market conditions and the completion of Wheatstone representing the last of the foundations work on LNG projects under construction in the country, the year ahead for the Keller Australia will be difficult. Management has begun to implement a number of initiatives to streamline the business and obtain cost savings. Frankipile received an award for sustainable achievement and leadership from Exxon Mobil in relation to their work on a major LNG project in Papua New Guinea.

There are a number of case studies included in the annual report. A 100 year old seawall built on top of wood piling was erected to provide access to Seattle’s piers, and supports the Alaskan Way Viaduct and the Alaskan way itself. The contract is worth £25M and the customer is the City of Seattle. Hayward Baker is currently performing jet grouting to depths of up to 85 feet to provide seismic stability and foundation support for the repair and replacement of a 0.7 mile section of the seawall.

The group is engaged on a £13.7M contract on the Berlin State Opera house in a joint venture with Bauer Spezialtiefbau where the group has completed the excavation pit to a depth of 12 to 14 metres. Another contract is on the Sengkang General Hospital for the Ministry of Health in Singapore worth approximately £28M where the group has completed piling works comfortably ahead of schedule. Finally the group’s largest ever contract in Wheatstone in Western Australia for Chevron working alongside Bechtel was mostly completed during the year. The contract was to procure, install and test around 20,000 piles and was worth about £105M. In addition, the group was also conducting certification and maintenance of piling platforms, storage, transport and distribution of piles and various other services.

The group is working in partnership with Monash University to develop geothermic piles incorporating heat exchangers for the intermittent storage of energy in soils for the heating and cooling of buildings. This technology should minimise the carbon footprint of built structures while also providing substantial long-term cost savings. Hayward Baker is partnering with three US universities to design methods for using ground improvement in liquefaction remediation. Also, Keller in the UK is working in partnership with Novacem on a carbon negative cement solution for the ground engineering industry which should see energy savings of between 60-80% over traditional methods.

During the year the group acquired Ansah, a business based in Kuantan in Malaysia for an initial consideration of £3.5M and contingent consideration of up to £1.5M. The acquisition generated £3.6M in goodwill. In May the group acquired the remaining 45% minority shareholding of Keller Engenharia Geotecnica in Brazil for a cash consideration of £2.8M at a premium of £1M to net book value. These acquisitions were fairly minor when compared to the £198M spent last year on Keller Canada, Franki Africa and Geo Foundations.

The reason the group made a loss this year was the £54M provision for a pay out on a disputed contract. A UK contract completed in 2008 was subject to litigation proceedings that was settled in February 2015. The final cost to the group is subject to a number of remedial and other actions to be undertaken as part of the settlement agreement and the above charge is the best estimate of the net cost to the group before taking account of future recoveries under applicable insurance. It is unclear exactly what the problem with the contract is and the extent to which it is covered by insurance as the company has not given any details but this is a substantial figure that needs to be paid.

The group refinanced most of its debt and financial facilities during the year, extending maturities, further diversifying the sources of finance and improving a number of key terms. A new five year £250M revolving credit facility was agreed in July, replacing a £170M facility expiring in 2015 and a $150M facility expiring in 2017. The group also raised $125M through a private placement with US institutions, the proceeds of which were used in part to repay $70M of private placement borrowings which matured in October. The group’s debt facilities now mainly comprise $165M of US private placements maturing between 2018 and 2024 and the £250M multi-currency revolving credit facility expiring in 2019. At the year-end there was £197.4M undrawn.

The group has pension schemes based in the UK, Germany and Austria. The UK scheme was closed to future benefit accrual in 2006. The last valuation of the scheme found that it was only 77% funded which means that going forward the group has to make £1.6M contributions a year to try and recover the deficit of £11.6M. The Austrian scheme also had a deficit which was £13.8M at the year-end.

The group has hedges against the dollar/sterling exchange rate changes but the fair value of the hedge currently has a liability of £18.5M which doesn’t look great and an increase of ten percentage points of Sterling against the other principal currencies would reduce profits by about £8.2M. An increase of one percentage point with regards to interest rates would reduce the pre-tax profit by £800K and this includes the impact of hedges. Other risks are associated with market cycles and economic downturns, although the international nature of the projects provides some protection against this. Also, as seen with the disputed contract that recently went to court, the tendering and management of contracts is another potential risk.

It was announced that the CEO was intending to retire at the end of next year having spent 25 years with the group, 11 of which were as CEO. While the group find a replacement, Justin will continue to carry on in the job. Also during the year the group appointed Nancy Tuor Moore as a non-executive director.

Going forward, after a relatively quiet period in the summer, the group’s contract awards have picked up in recent months. As a result, the order book at the end of January is 8% higher than at the same time last year with the increase spread across all of the divisions except for Australia where the Wheatstone contract was largely completed. Whilst conditions in the main markets remain mixed, the gradual upturn in the US, the largest market, continuing improvements in the operating performance and the strong order book mean that the group is set for “another year of progress” in 2015.

After a 5% increase in total dividends, the shares are now yielding 2.4%, increasing to 2.6% on next year’s consensus forecast. At the current share price the shares trade on an underlying PE ratio of 14.3 which falls to 12.4 on next year’s consensus forecast, which seems decent value. At the end of the year, net debt stood at £102.2M compared to £143.7M at the end of last year. It is also worth noting the £50.4M of operating leases off the balance sheet, however, which represented an increase of £6.6M year on year.

So, on an underlying basis this has been a pretty good year for Keller. Underlying profits increased, underlying net tangible assets improved and the increased operational cash flow provided lots of free cash. The one thing that hangs over all of this is the litigation surrounding the contract dispute – this has sent the group into a loss for the year and reduced net tangible assets year on year. The contract took place in 2008 so I hope lessons have been learned here. Operationally the group has done well in North America and the EMEA region with Asia and Australia proving more difficult. Markets that are reliant on the natural resources sector such as Canada and Australia have going rather difficult and profits from Australia in particular are expected to fall next year without the considerable benefit of the Wheatstone project.

Despite the problems in Australia, the board expect further progress next year, the banks are obviously happy and have increased headroom on the debt and the order book is now head of the same time last year. The dividend yield of 2.6% is OK if not spectacular but the forward PE of 12.4 seems good value for a market leader such as Keller. These shares look potentially interesting.