Games Workshop has now released its final results for the year ended 2016.

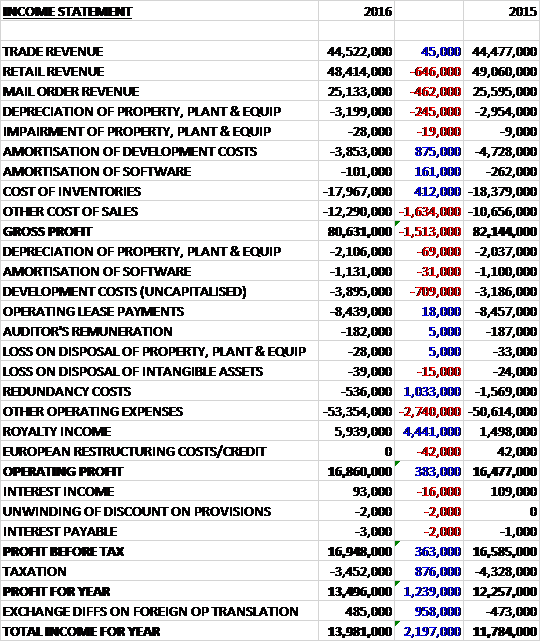

Revenues declined when compared to last year due to a £646K fall in retail revenue, and a £462K decrease in mail order revenue. Amortisation fell by £1M and cost of inventories was down £412K but depreciation was up £245K, mainly as a result of the opening of the visitor centre last year, and other cost of sales grew by £1.6M to give a gross profit £1.5M below that of last year. We then see development costs up £709K and other operating expenses increasing by £2.7M, mainly relating to new store openings and higher staff costs but redundancy costs fell by £1M and royalty income grew by £4.4M, mainly due to the launches of Total War: Warhammer and Warhammer: End Times – Vermintide, which meant that the operating profit increased by £383K. Tax was down by £876K so that the profit for the year came in at £13.5M, a growth of £1.2M year on year.

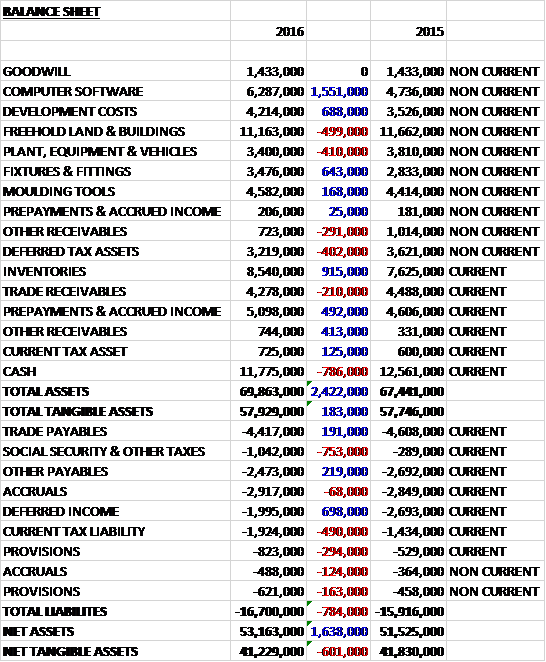

When compared to the end point of last year, total assets increased by £2.4M driven by a £1.6M increase in computer software, a £688K growth in development costs, a £643K increase in fixtures and fittings and a £915K growth in inventories, partially offset by a £786K decline in cash. Total liabilities also increased during the year as a £753K growth in social security and other tax payments along with a £490K increase in current tax liabilities and a few other small increases was partially offset by a £698K decline in deferred income. The end result is a net tangible asset level of £41.2M, a decline of £601K year on year.

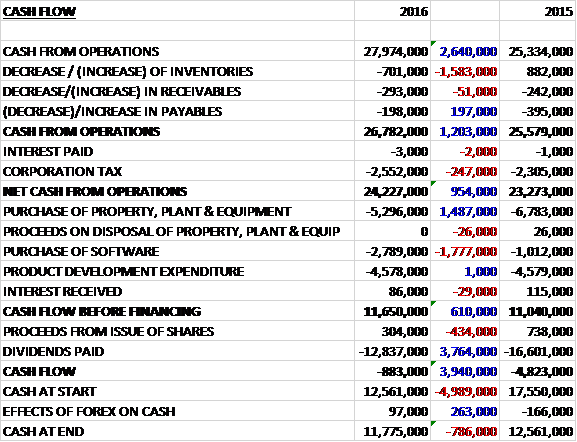

Before movements in working capital, cash profits increased by £2.6M to £28M. There was a modest cash outflow from working capital and after tax payments increased by £247K, the net cash from operations came in at £24.2M, a growth of £954K year on year. The group spent £5.3M on tangible fixed assets, £2.8M on software and £4.6M on product development which meant the free cash flow stood at £11.7M, all of which was paid out in dividends to give a cash outflow for the year of £883K and a cash level of £11.8M at the year-end.

The profit in the Trade business was £10.6M, a decline of £882K year on year. The new trade team for accounts in the UK and Europe has settled in well and made some progress during the year. Sales in North America were broadly flat. They have also updated their trade product range in June 2016 to ensure they provide their stockist accounts with the best sellers.

The profit in the Mail Order business was £13.7M, a fall of £685K when compared to last year. Sales of the Forge World range grew by 28% but there was a 12% decline in sales of the Citadel range. In the first half of the coming year they will be making a change to their home page; removing complexity and adding a deeper introduction to the worlds. During the year they migrated their web data centre to a new location in North America.

The loss from the Retail business was £3.4M, an increase of £1.9M when compared to 2015. The CEO has stated that the underlying performance of their own stores has not been good enough and the group made some changes to their retail support structure to address the decline. The flat management structure did not support the complexity of managing 149 stores across 14 countries in Europe and in January they moved to a country based solution. They now have four territory managers; Germany/Scandinavia, Netherlands, France and Spain/Italy.

The profit from the Product and Supply business was £7.1M, a decline of £1.5M year on year. The profit from Royalties was £5.3M, a growth of £4.3M when compared to last year. This has probably been the best year to date for licencing with launches of Bloodbowl 2, Warhammer: End Times, Warhammer 40,000: Freeblade, and probably most importantly, the launch at the end of May of Total War: Warhammer.

The year started with the launch of Warhammer: Age of Sigmar, one of the biggest changes ever made to a core universe. The simplified rules, supporting the models for those who like to play, made it much easier to get started. It didn’t all go smoothly, however, and the board learnt some lessons on how to deliver product system changes on this scale and they released more of the range in the second half of the year with sales of Sigmar at a higher rate than Warhammer has enjoyed for several years.

After a disappointing December, they carried out a review of their operational plan and performance improved since December, although not enough to prevent sales declines in most areas. Costs increased during the year, mainly as a result of the store opening programme and the full year effect of the depreciation of the visitor centre. The group now have a small retail sales HQ in Dallas and have opened 16 stores in the US during the year, taking the total up to 100. They are now targeting twenty store openings per year in the country which will be the main focus for store openings

The group now offer their models at a broader range of price points and have piloted a small “Start Collecting” range of models that have sold well. They have also introduced some stand-along high value box games, a gateway into Games Workshop products, which have also sold well during the year.

In Asia the group now have four new sales territory managers: in Singapore, Hong Kong, Japan and Malaysia, in addition to the existing business in China. They will grow the group by opening stockist accounts and their own stores.

The group now have 96 multi-man format stores and 355 one man stores. Due to the timing of the lease breaks, the opportunity arose to pilot some larger multi-man format stores placed to service a greater number of customers. The Tottenham Court Road store is on target to be the highest sales value store and the other pilots in Sydney and Copenhagen delivered their promises too. These successes give them more store options but the standard format will remain the one man store model.

To broaden their reach they are piloting a small range of products in new markets. They launched a dispenser of eight products called Battle for Vedros in toy shops in North American in June and will launch a small range called Build and Paint globally in modelling and toy shops later in the coming year. Currently all of the stores carry the same range but they will be looking at a matrix approach of broadening the product range in the higher volume stores and optimising their product range in some of the smaller stores. They will also continue to invest in core IP with product launched planned throughout 2017.

There are a number of risks for the coming year. The change of the core ERP system in the UK is a complicated project with the risk of widespread business disruption if not implemented well. Also, the change of the mail order warehouse system carries some risk. The board have avoided the Brexit issue, stating that they feel it is too early to tell what the effects will be.

During the year he group invested £7.5M in the design studio, including software costs, with a further £2.2M spent on tooling for new plastic models. A similar level of investment is expected in the coming year. They are also currently working on a significant project with a UK software supplier to upgrade the core IT systems that interface with the manufacturing equipment and systems. The project to upgrade the IT infrastructure and software for the warehouse that supports the mail order business will be delivered this autumn at a cost of £900K. The European ERP replacement has been more complex and costly than originally stated and will now launch in 2018 at an estimated cost of £6M, an increase of £1.5M.

At the current share price the shares are trading on a PE ratio of 11.6 which grows to 12.3 on next year’s consensus forecast. At the current share price the shares are yielding 8.2% in dividends which falls to 7.2% on next year’s forecast. Net cash at the year-end was £11.8M compared to £12.6M at the end of the prior year.

Overall then this has been a bit of a mixed year for the group. Profits were up, mainly due to lower redundancy costs but higher royalty income also had an effect. Net tangible assets declined but operating cash flow also increased with plenty of free cash being generated. The trade, mail order and retail divisions all saw performance deteriorate with new territory managers being appointed to try and stem the decline in the latter. The group was saved though but a large increase in royalty income following the success of the Total War video game.

The group is looking to the US for expansion and is also trying to tempt new customers with simplified rules but they have to be careful here as it is a balancing act between new customers and their existing fans. The ERP update is also something to watch as it has the potential to be disruptive. The forward PE of 12.3 looks OK but it is the dividend yield which is the real attraction here – the 7.2% yield looks decently covered by cash flow so is probably sustainable. I am tempted to go for this.

On the 16th August the group announced that non-executive director Elaine O’Donnell purchased 3,593 shares at a value of £19.5K. She now owns 5,093 shares in the company.

On the 6th October the group released a trading update covering the first four months of the year. In all, sales and profits are ahead of the board’s original expectations. Over the period, sales have grown in constant currency terms and have further benefitted from the favourable impact of a weaker pound.

On the 17th October the group announced a final dividend of 25p per share which equates to an annual yield of an astonishing 8.1%.

On the 2nd November the group announced that head of product and supply Max Bottrill acquired 3,500 shares at a value of nearly £20K.

Overall these updates all look decent to me and I continue to hold.

On the 1st December the group released a trading update covering the first half of the year where they stated that sales and profits are significantly ahead of those last year and head of the board’s original expectations with operating profit estimated to be around £13M. Over the period they have seen strong sales and profit growth in constant currency terms which have been further benefited from the favourable impact of a weak pound and royalty income is also expected to be ahead of last year.

This all sounds positive, I continue to hold.