Spectris has now released its interim results for the year ending 2016.

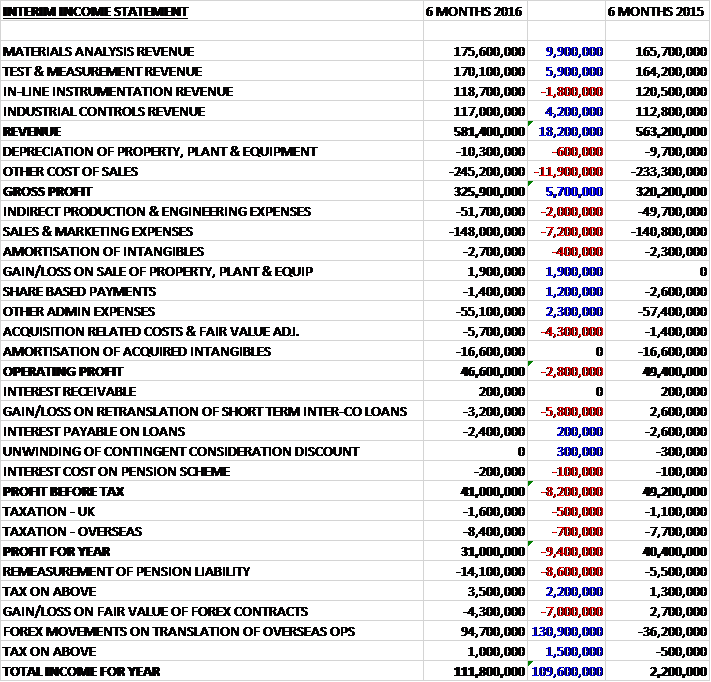

Revenues increased when compared to the first half of last year due to favourable forex movements as a £1.8M decline in in-line instrumentation revenue was more than offset by a £9.9M growth in materials analysis revenue, a £5.9M increase in test & measurement revenue and a £4.2M growth in industrial controls revenue. Cost of sales also increased which meant that the gross profit increased by £5.7M. Production & engineering expenses were up £2M whilst sales & marketing expenses increased by £7.2M but there was a £1.9M gain on the sale of fixed assets, a £1.2M reduction in share based payments and a £2.3M fall in other admin expenses. Acquisition costs did increase by £4.3M, however, which gave an operating profit £2.8M below that of last time. We then see a £5.8M detrimental movement to a loss on the retranslation of short-term inter-company loans and after tax also grew, the profit for the period came in at £31M, a decline of £9.4M year on year.

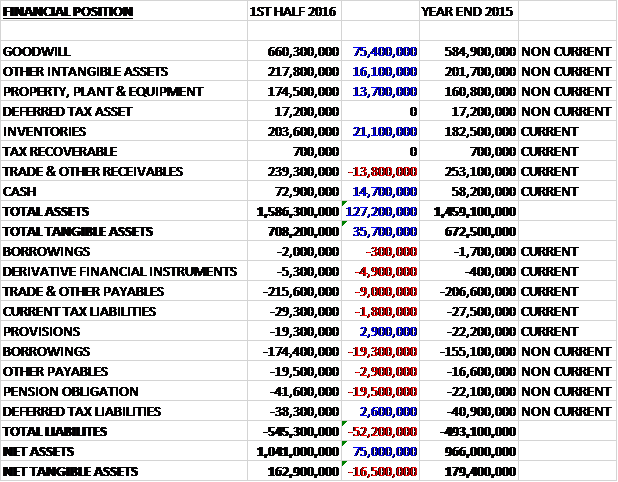

When compared to the end point of last year, total assets increased by £127.2M to £1.586BN driven by a £75.4M growth in goodwill, a £21.1M increase in inventories, a £16.1M growth in other intangible assets, a £14.7M increase in cash and a £13.7M growth in property, plant and equipment, partially offset by a £13.8M decline in receivables. Total liabilities also increased during the period due to a £19.6M growth in borrowings, a £19.5M increase in pension obligations and a £9M growth in payables. The end result was a net tangible asset level of £162.9M, a decline of £16.5M over the past six months.

Before movements in working capital, cash profits declined by £4.1M to £74.4M. There was a cash inflow from working capital due to a decrease in receivables and after tax payments modestly increased, the net cash from operations came in at £80.1M, an increase of £27.2M year on year. The group spent a net £5.5M on capex and £24.2M on acquisitions to give a free cash flow of £50.6M. This was easily enough to pay for the £38.4M of dividends and £2M in interest payments to give a cash flow for the period of £10.4M and a cash level of £70.9M at the end of the half.

Trading conditions in the period continued to be challenging, particularly in the in-line instrumentation and industrial controls segments, both of which were impacted by weak global industrial demand. Like for like sales overall were down 3% with a 4% decline in North America reflecting weak industrial demand following the sharp fall in energy prices in 2014. Like for like sales grew in Asia, benefiting from growth of 5% and 8% in China and Japan respectively, although this was against a weak comparator last year. Like for like sales in Europe declined by 6% and a 15% like for like decline in ROW countries was largely due to the weak economy in Brazil.

The adjusted operating profit of the Materials Analysis division was £21M, a growth of £6.4M year on year reflecting an improved product mix with higher aftersales along with prior year restricting, on revenues that increased by 6% (flat like for like) with good growth in China, Japan and North America being offset by declines in Europe and Brazil.

Like for like sales in the pharmaceutical sector grew modestly in the period, despite the lack of Indian generic drug manufacturers being focused on FDA approvals for US export, reflecting a healthy underlying demand. After modest growth last year, sales to the metals, minerals and mining sectors suffered sizeable declines across all four regions. Large systems orders continue to be deferred or cancelled and the growth within the cement and building materials markets in North America and Europe has abated. Aftermarket sales remain strong in this sector, however, as customers prefer to repair and support existing equipment rather than replace or upgrade.

Sales to academic research institutes increased, reflecting strong growth in China and India after both markets had been weak in 2015 with growth also seen in North American and Germany. Outside Germany, European academic research expenditure remained subdued with significant weakness in the UK. Demand in the electronics, semiconductor and telecoms sector continued the growth trajectory that begun in the second half of 2014, reflecting good acceptance of the group’s new products and the acquisitions made of distributors in South Korea and Taiwan.

The board expect sales growth to continue in the second half of the year within the pharmaceuticals and electronics sectors. Demand from the metals, minerals and mining sector is expected to remain weak and to be primarily of an aftermarket sales nature. Sales to the academic research sector remain unpredictable as public sector budgets are likely to remain under pressure in many countries. The benefits of the prior year cost reduction measures, coupled with sales growth, are expected to lead to further improvements in profitability in H2.

The adjusted operating profit of the Test & Measurement division was £18.5M, a decline of £200K when compared to the first half of last year on sales that increased by 4% but fell by 4% on a like for like basis reflecting the difficult market conditions experienced by ESG Solutions in the North American unconventional oil and gas market. On a like for like basis, the profit declined by 9% as the positive pricing and mix effects of the two largest operating businesses were offset by the impact of negative operating leverage at ESG. Regionally there was good sales growth in Asia, driven by China, with declines in all other regions.

There was good sales growth to machine manufacturers, a significant proportion of which represented sales into the automotive supply chain, although direct sales to the automotive sector were flat. There was good growth from the sector in China and India but the market in Europe, in particular the UK and Germany, was weak. Sales to the aerospace industry decreased. Following several years of strong growth in Asia, sales to the region fell in the period despite growth in China and India. There were also lower sales to North American aerospace customers during the period but sales to European customers increased.

Sales to electronics and telecoms customers increased following declines in 2015 – sales in the category are lumpy. The underling business trends in this sector remain healthy and the group sees good opportunities to provide additional testing and calibration services. Sales of the environmental noise monitoring services declined in the period due to the end of a major contract secured last year with the Italian government for exhaust monitoring in vehicle inspection sectors. The underlying market conditions for the business remains healthy, however.

Ongoing weakness in the unconventional oil & gas and mining markets led to difficult market conditions for the microseismic monitoring solutions business, particularly in North America. The business continues to develop opportunities in its international markets and is making progress in this regard in Latin America and Australia, although the near-term focus remains on cost control.

Going forward, the board expects the automotive and aerospace sectors to remain subdued in the second half with growth focused on engineering software and services. The consumer electronics market is expected to remain attractive but the microseismic monitoring market is likely to remain challenging for the rest of the year.

The adjusted operating profit of the In-line Instrumentation division was £10.9M, a fall of £2.9M when compared to the first half of 2015 on like for like sale that declined 6%. On a regional basis, sales grew in North America but decreased in all other regions. This decline reflected ongoing weakness in capex across many heavy process industries such as hydrocarbon processing, chemicals, plastics and paper although certain niche markets remained robust such as emissions monitoring, healthcare, tissue and pulp and wind energy.

Like for like sales in the pulp and paper markets grew slightly reflecting the continued good progress the group are making in diversifying away from the graphic paper market. They increased sales to the tissue and pulp markets and their innovation in new solutions is helping to soften the decline in sales to the graphic paper industry. Sales to the web and converting industries declined slightly reflecting a lack of large projects in North America and Europe, with only the packaging and metals industries providing any respite from the significant reductions in capex being experienced across most process industries.

Sales to the energy and utilities market declined in the period. Sales of condition monitoring solutions to the wind energy sector decreased, although this primarily reflected the strong prior year comparison and the project nature of the business as underlying market conditions remain good. They continue to secure retrofit contracts in the wind energy market, including multi-year service agreement. There continue to be delays and cancellations of large projects in the hydrocarbon processing sector, particularly in North America and the Middle East, although there is investment in China to improve environmental quality which is leading to increased demand in emissions monitoring systems. There are also good levels of interest for the Vibration Interface Module, a system that enables data and signals from any machine protection system to be processed, stored and analysed on a single condition monitoring system.

There was good sales growth to the North American healthcare market. Following a large amount of acquisition activity amongst the customer base last year, which led to many investment decisions being postponed, there is now renewed investment from this sector in their gas sensing technology.

Going forward, management expect growth in sales to the pulp, packaging and tissue market to continue in the second half, helping to offset the structural challenges in the graphic paper market. Demand from the wind energy sector is also expected to remain healthy. Elsewhere, capex in many of the process industries that the group serves is likely to remain subdued.

The adjusted operating profit of the Industrial Controls division was £18.5M, a decline of £1.8M year on year on sales that fell 5% year on year reflecting continuing broad-based weakness in US industrial production with the business having a high exposure to the North American market. Outside that region, the segment performed well, notably in China where there was a strong demand for factory automation solutions.

Whilst the industrial networking business suffered from challenging market conditions, particularly in the core North American market, management believe this primarily reflects short-term cyclical softness and continue to view industrial connectivity as a key strategic market. The recently established industrial internet of things innovation centre in the US is progressing well and during the period the group held a productive cross-operating business workshop to share expertise on the topic.

Last year’s acquisition of Label Vision Systems has gone very well with strong sales growth of its products. There was also good sales growth in the core automatic identification and machine vision solutions business, particularly in China and they have continued to enhance the features of the Micro Hawk smart camera platform launched last year.

Going forward, progress for the segment in the second half will largely be determined by the industrial demand environment in the US, though management expect to see continued good growth in Asia and from their machine vision business. In the coming years the need for customers to improve efficiency is expected to result in increased demand for factory automation and industrial networking products, particularly in China where there is a drive to improve the return on previous capital ingestment.

There were a number of acquisitions during the period. In February the group acquired CAS Clean Air Service, a company based in Switzerland, for a total consideration of £12M, generating goodwill of £4.9M. This business extends the group’s capabilities in monitoring and calibration services within the life sciences market and is being integrated into the Material Analysis segment. In June they acquired Integrated Process Systems India for a total consideration of £900K, of which £200K was deferred. This acquisition generated goodwill of £500K and is being integrated into the Test and Measurement segment.

In June they acquired Capstone Technology, a company based in the US, for a total consideration of £14.6, generating goodwill of £9.4M. The business is a provider of software solutions for process control optimisation and decision support, serving multiple industries such as pulp, paper, chemical, utilities, oil & gas and good & beverage. It is being integrated into the in-line instrumentation segment. The profit contribution from these acquisitions was just £100K.

After the period-end the group acquired Sound & Vibration Technology for an initial consideration of £300K with an earnout based on future performance. This extends the group’s engineering services capability and offering of integrated solutions, primarily for the automotive market and the business is being integrated into the Test and Measurement segment. In late July they acquired DISCOM Elektronische Systeme und Komponenten, a company based in Germany, for an initial consideration of £13.3M with an earn-out based on future performance. The business is a provider of acoustical and vibration quality analysis, predominantly for powertrain production line testing within the automotive industry and is being integrated into the test and measurement segment.

Going forward, taking into consideration the potential net currency benefits at current exchange rates, the increased macro uncertainty and the limited visibility on trading in the second half, the expected overall outcome for the year is unchanged. The board believe that the Brexit vote presents only limited short term direct impact for the group. The main near term risk stems from broader uncertainty which could inhibit investment and increase market volatility. A Brexit risk committee has been established and the group will continue to monitor any additional exposure as the full implications become clearer.

The net debt position at the end of the period was £103.5M compared to £98.6M at the end of last year. At the current share price the shares are trading on a PE ratio of 19.5 which falls to 15.9 on the full year consensus forecast (likely to have been adjusted to remove certain items). After an increase in the interim dividend, the shares are yielding 2.7% which increases to 2.8% on the full year forecast.

Overall then this has been another difficult period for the group. Profits decreased, net tangible assets were down and although the operating cash increased with plenty of free cash being generated, this was aided by a decline in receivables and cash profits declined year on year. The Materials analysis business was the only segment to see growth, due to favourable product mix and lower costs (sales were flat). Test & Measurement was hit by a slow-down in the oil and gas market; in-line instrumentation suffered from weakness in capital expenditure in processing industries; and industrial controls declined due to a general weakness in US industrial production.

Going forward, this sluggish environment is unlikely to change any time soon and a forward PE of 15.9 and dividend yield of 2.8% doesn’t sufficiently account for these issues in my view.

On the 2nd September the group announced that it had completed the acquisition of Millbrook for a consideration of £122M, of which £3.4M is deferred for two years, which will be met from existing cash and bank facilities.

The business is a European test, validation and engineering service provider, primarily for the automotive and related markets. It was sold by General Motors to Rutland Partners and management in 2013 and from that point has been transformed from a GM dependent business to one with a broad base of UK and international clients. In September it acquired Test World, a winter vehicle and tyre testing business based in Finland. Their UK test tracks and facilities are located on a wholly-owned 665 acre site in Bedfordshire that has scope for further related commercial development.

The business has undertaken significant growth capital expenditure programmes in 2015 and 2016, from which trading this year is expected to benefit considerably. Last year, EBITDA came in at £5.4M but beyond this year the business has significant opportunities to accelerate its growth with a range of customers and in key areas of testing, through further customer-supported investment in facilities.

On the 22nd November the group issued a trading update covering the first four months of H2. Reported sales increased by 18% with acquisitions contributing 4% of that growth and forex movements contributing 18% so like for like sales declined by 4%.

Regionally like for like sales grew in Asia Pacific and ROW, and declined in Europe and North America. The performance in Europe has improved moderately since the first half of the year but North America saw a further deterioration. Materials Analysis delivered positive like for like sales growth but sales declined in the other three segments. At Omega Engineering the adverse profit impact from inventory adjustments mentioned at the half year stage has been quantified and ongoing process improvements continued to be implemented to remedy this.

Against this trading environment. The group continues its self-help actions to better align costs to sales performance and is on track to deliver £10M cost savings for the full year. They are making good progress in quantifying and planning the various productivity improvement initiatives included in “Project Uplift”.

During the period the group completed the acquisition of Millbrook for a consideration of £122M. The business is a European test, validation and engineering service provider, primarily for the automotive sector and related markets such as tyres, petrochemicals, defence and security. The integration is proceeding well and trading is in line with expectations. Following the acquisition, the net debt position was £180M.

In light of the challenging trading conditions, particularly in North America, and the continued weakness in the global oil and gas market, a review is underway of the goodwill associated with ESG Solutions and Omega Engineering which is likely to lead to a non-cash impairment charge in the full year accounts.

Trading conditions in the period have marginally deteriorated, particularly in North America, and the group’s performance continues to be impacted by weak industrial demand. This is offset by further strategic progress on acquisitions and the impact of forex movements. Accordingly the board expect the full year adjusted operating profit to be in line with current market expectations of between £179M and £209M.

Overall then times are tough but the group is being saved by the weakness in Sterling. I am not rushing in here just yet.