Interserve has now released its half year results for the year ending 2014.

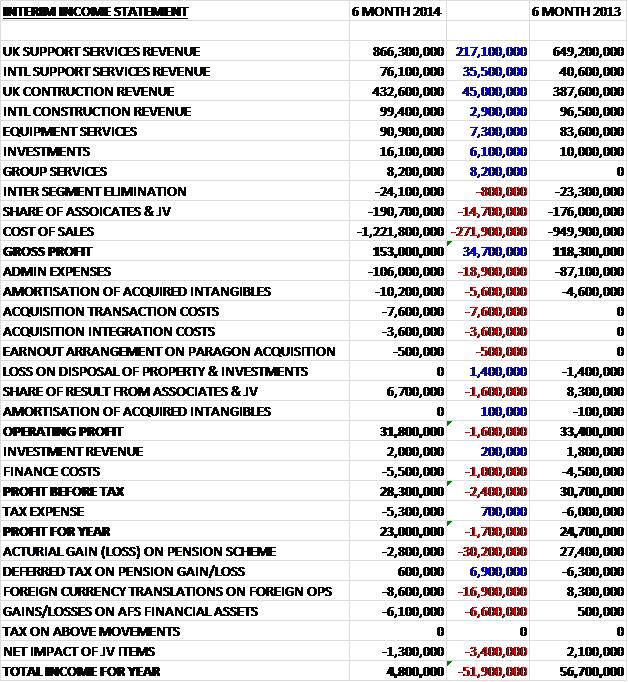

When compared to the first half of last year revenues increased across all sectors with some notable increases being a £217M hike in UK support services, a £35.5M increase in International Support Services revenue and a £45M increase in UK Construction revenue. As would be expected, the cost of sales also increased, up £271.9M so that Gross profit was some £34.7M higher. Admin expenses were up £18.9M and there were also a number of one-off costs including £7.6M in transaction costs, £3.6M of integration costs and a £5.6M increase in amortisation of acquired intangibles. The share of joint venture profit fell by £1.6M during the year which incidentally was the same amount that Operating Profit fell by. Finance costs increased by £1M but these were largely mitigated by a reduction in tax expense so that the profit for the year was £23M, £1.7M less than in the first six months of 2013 but when the one-off acquisition costs are considered, this is not a bad result.

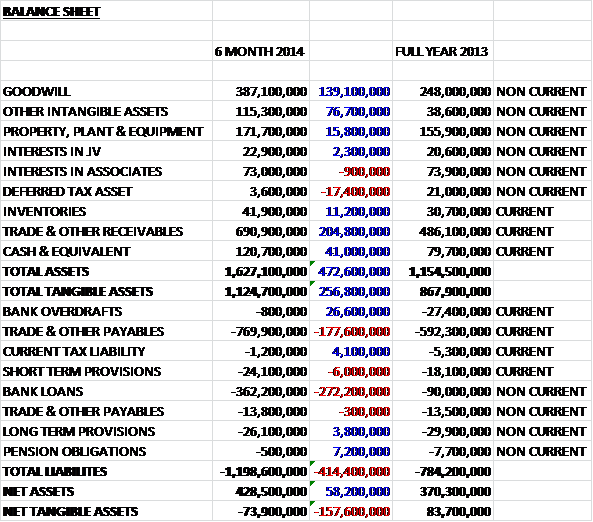

Total assets increased by a massive £472.6M when compared to the end point of last year. This increase included a £139.1M hike in the value of Goodwill and a £76.7M increase in other intangible assets. There were also some large tangible increases with receivables some £204.8M higher and cash £41M higher. Most of these increases were due to the Initial acquisition and in fact, only deferred tax assets fell – down £17.4M to just £3.6M. Liabilities also increased during the period, driven by a £272.2M increase in bank loans and a £177.6M growth in trade and payables, this was somewhat mitigated by a £26.6M fall in bank overdrafts and a £7.2M reduction in pension obligations, which now only stand at £500K. Overall then, net assets were up by £58.2M to £428.5M but due to the large increases in intangible assets, net tangible assets fell by a disappointing £157.6M and are now negative to the tune of £73.9M.

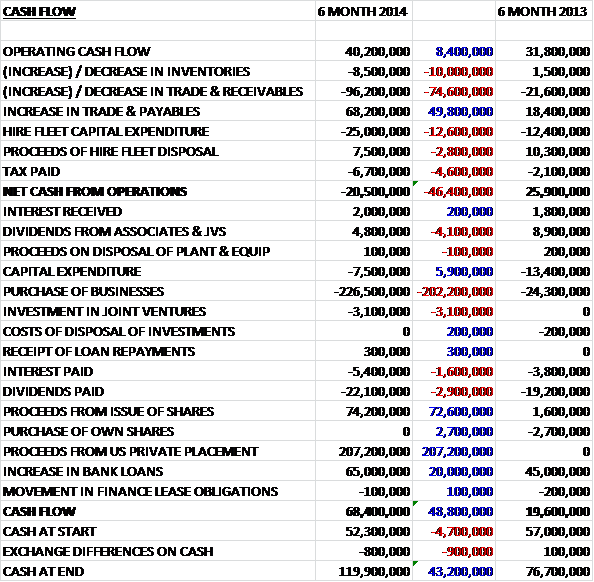

Before the movement in working capital, cash profits were up £8.4M to £40.2M. This is before working capital changes primarily related to the acquisition, although a £25M increase in hire fleet capex didn’t help. This drove the net cash from operations down by £46.4M to an outflow of £20.5M. The group also received about half of the amount of dividends from associates and joint ventures than it did this time last year but also nearly halved the non-hire fleet capex. The largest expense was clearly the £226.5M spent on the purchase of Initial which was paid for mainly by a £207.2M receipt from the US loan note placing. Other cash came in due to £74.2M of proceeds from new shares and a £65M increase in bank loans. All this meant that the group still managed a positive cash flow of £68.4M despite the £22.1M paid out in dividends. To be honest, the acquisition is such an upheaval during the half year that not much can really be taken from the cash flow statement during this time.

UK Support Service profit was up £8.6M to £33.9M which was driven by increased revenues as the operating margin remained stable at 4.2%. Strong organic growth came from existing clients and new contract wins in the defence, automotive, real estate and government sectors. Future workload for the division increased by £700M to £5.8BN during the period. Highlights during the year included mobilising a five year contract with the BBC, valued at more than £150M to provide facilities management and security services at over 150 buildings; winning a £322M contract with the MoD to manage the National Training Estate over a five year term with an option to extend for another five years (the group had already previously had a contract with the MoD); building on relationships with existing clients to win additional work with the Foreign & Commonwealth office, Mercedes-Benz and CBRE; and winning three Community Work Placement contracts worth £19M covering Yorkshire, Devon, Cornwall, Dorset and Somerset.

International Support Services profit was up £800K to £3.2M. Revenue was up strongly, partly as a result of the Adyard acquisition but due to a change in the business mix following this acquisition and competitive pressures, margins reduced to 4.3%. Future workload declined £15M to £149M which is rather disappointing but highlights during the period included a three year contract extension to the long standing logistics and oilfield service contract with Occidental Petroleum; a new three year contract to provide Qatar Shell with a range of mechanical services, including the replacement of large sections of piping and an upgrade to structural supports; and a five year facilities management contract with ExxonMobil.

UK Construction profit was up £600K to £8M. Demand in the market is beginning to improve but margins remain tight at 1.9% as supply chain pressures feed through. Revenues were boosted by the Paragon business acquired last year which increased momentum and won new contracts from Facebook and Markel and helped future workload increase by £400M to £1.4BN. About two thirds of the work is derived from framework agreements and repeat business relationships. The group started work on the Haymarket development in Edinburgh and the Co-Op building in Newcastle during the period. Other highlights included winning a £150M PFI contract to build seven secondary schools across Herts, Luton and Reading; the awarding of a contract to build a high energy proton beam cancer therapy facility for the Christie NHS trust in Manchester; winning a contract to build a new £55M sports centre for the Uni of Birmingham; the completion of JLR’s new Engine factory near Wolverhampton; and the completion of the Endeavour Centre in Portsmouth.

International Construction profits fell by £1.4M to £4.3M despite a small increase in revenues to give a reduced margin of 2.4%, but the group is starting to see recovery in the Middle East market. Encouragingly, future workload grew by £28M to £227M with highlights including a £323M contract in a joint venture with ELEC Qatar to build Doha Festival City, which will become Qatar’s largest retail development; further works contracts for Siemens and NCC in the development of Qatar’s power network; the commencement of a £160M extension to Dubai’s Mall of the Emirates; and a contract to build a new field services complex for Halliburton in Abu Dhabi as well as work with DP World, Dubai’s Taj Hotel and the RIVA group.

Equipment Services profits were up £5.5M at £14M which represents both a revenue and margin increase to a decent 15.4% when compared to the same period of last year. Capital expenditure rose significantly as the group increased investment in the equipment fleet and in new branches in South Africa, the US and Panama. In Asia there was a strong performance in Hong Kong, driven by infrastructure sending and the group also performed well in the Philippines with further investment in the power sector expected. There was strong growth across the Middle East but demand in Australia was affected by the completion of a number of energy projects and a slowdown in the mining sector. The UK performed well, boosted by projects such as the Resorts World Casino in Birmingham.

The recovery in the US was somewhat slower than anticipated and Government investment remained sluggish but the expansion into California is bearing fruit with ongoing work on a number of sizeable developments in the Bay area and San Francisco. In addition, the continued expansion into Latin America opened up new markets in Colombia and Panama. Highlights included the supply of heavy duty support equipment for the construction of a new Terminal Complex at Abu Dhabi international airport; a new transport hub providing transport of pilgrims to Mekka; the supply of 1,300 tonnes of equipment for the Mall of Egypt project; and providing the shoring towers for the Sultan Qaboos Mosque in Oman.

The contribution of investments fell by £300K to £700K. Highlights included a further £3.1M investment into the Haymarket project in Edinburgh; financial close on the redevelopment of the Co-Op building in Newcastle; being appointed preferred bidder to build seven schools in the UK and a centre of excellence for the Scottish National Blood Transfusion Service; being selected by Southampton NHS Foundation Trust as its long term development partner; and securing a £9.6M investment from the Scottish Partnership for regeneration in urban centres as a co-investor in the Edinburgh Haymarket development.

As mentioned in previous updates, the most important event this year was the acquisition of Initial Facilities from Rentokil. The acquisition cost £249.7M and seems mainly to be designed to increase facilities management exposure to private companies. The acquisition came with just under £110M of net assets with the goodwill paid being some £139.8M. Since acquisition, Initial has contributed £160.6M to revenue and a £7.7M loss after exceptional items. The integration is well underway and the anticipated synergies remain on track with Initial winning new contracts with Exterion and Dairy Crest during the period.

After the period end the group protected around 35% of the pension scheme liabilities from fluctuating interest rates, inflation and longevity risk through a buy-in agreement with Aviva. Trading conditions in the group’s main market continue to improve and going forward, they are positioning themselves to take advantage of sustained market improvement by investing in skills, infrastructure and fixed assets which will obviously have an effect on short term cash flow. The future workload for the group stands at £7.5BN, which compares favourably to the £6.4BN at this point of last year. It has been announced that David Thorpe will retire from the board at the end of August and he will be replaced as Remuneration Committee chairman by Keith Ludeman.

At the end of the half year, net debt stood at £243.1M, an increase of £204.5M when compared to the end point of last year. A dividend of 7.5p per share (an increase of just over 10%) was declared which makes the rolling annual yield 3.3%. It is clear that this is an important year for Interserve with the acquisition being very material to the group. It is a case of wait and see really to see how Initial integrates and whether it is worth the extra debt taken on board. The profit this half is not bad when the acquisition costs are stripped out with the Equipment Services sector doing particularly well. It was disappointing to see net tangible assets slipping into net tangible liabilities. In conclusion, though, I am happy to continue holding here.

On the 21st August the group announced a new joint venture between Interserve and Shanks to build and operate a new waste treatment facility in Derby under a 27 year, £950M PPP contract. Interserve will start building the £145M Mechanical Biological Treatment facility and an on-site gasification plant which Shanks will operate along side Derby’s existing waste management facilities. The new plant is expected to be completed by 2017, at which point both Shanks and Interserve will inject £18M of subordinated debt into the joint venture.

On the 12th November the group released an interim management statement covering Q3 and a bit more. The group performed in line with expectations with organic growth in Support Services, UK Construction and Equipment Services. International Construction continued to struggle somewhat but the market seems to be improving. Pleasingly the integration of Initial Facilities has largely been completed and expected synergies remain on track. During the period the group won contracts with Hyundai Engineering and Construction (UAE), Qatar Foundation, Kempinski Hotel (Oman), Hong Kong Zhuhai Macao Bridge, Ministry of Justice, Derbyshire County Council, Southampton City Council, Warner Bros, Debenhams, Scottish Power, Northern Powergrid, Crossrail, Royal Opera House, Prince Charles Hospital and British Airways. All in all a decent update with no real suprises. As an aside, it is mentioned that the Financial Reporting Council has removed the obligation for companies to provide quarterly management updates so given Interserve’s usual terse updates, I suspect they will dispense with this annoyance going forward which is a bit of a shame.

On the 5th December the group announced that they had acquired the Employment and Skills Group (ESG), a UK based provider of vocational training, skills and employability services from Ares Capital for £25M. ESG provides training and employment services for Government and employers and also provides vocational training in three further education colleges in Saudi Arabia. The transaction is being funded from the existing debt facilities and is expected to be accretive in 2015. The price paid doesn’t seem high but it will be interesting to see how much the group makes from the acquisition.

On the 18th December the group released a statement detailing a new contract for the provision of probation and rehab services. A new partnership has been created with Addaction, Shelter, P3 and 3SC to manage services in Manchester, Merseyside, West Yorkshire, North Yorkshire, Humberside and Hampshire covering over 40,000 offenders each year. The collective contract values are worth £600M over seven years so represents a significant contract. Despite this good news, however, I have decided to sell out as I am concerned about the effect that low oil prices will have on the Interserve business in the Middle East. I still consider this company to be a quality investment but feel there may be some short term downside. I will continue to update on progress here.

On the 7th January the group released a trading update. It stated that they were performing in line with expectations. The integration of Initial Facilities is well advanced, as is the preparation for the mobilisation of probation services which are commencing at the start of February. The group has also formed a joint venture with the Rezayat Group in Saudi Arabia to provide facilities management services in the region. With the guidance for full year trading remaining the same, this is a robust update and I will continue to monitor proceedings from the sidelines.

On the 22nd January the group released a statement that Standard Life Investments had purchased 476,902 shares which would have been at a value of over £2.4M.

On the 29th January it was announced that another institutional investor had bought some shares. This time Henderson Global Investors purchased 250,000 shares worth about £1.3M. It seems that someone things these shares bay have been oversold.