Sylvania Platinum has now released its final results for the year ended 2016.

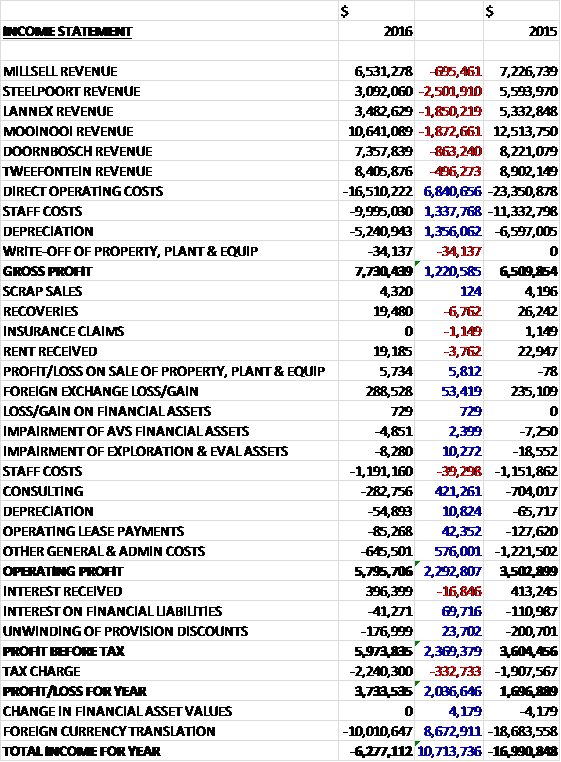

Revenues declined across all businesses when compared to last year as a result of the lower platinum price, with particularly large falls at Steelpoort, Lannex and Mooinooi. Direct operating costs, staff costs and depreciation all declined as well to give a gross profit $1.2M above that of last year. We also see a $53K increase in the forex gain, a $421K decline in consulting costs and $576K fall in other general & admin costs to give an operating profit $2.3M above that of last year. Finance costs came down somewhat but the tax charge increased by $333K which meant that the profit for the year was $3.7M, a growth of $2M year on year.

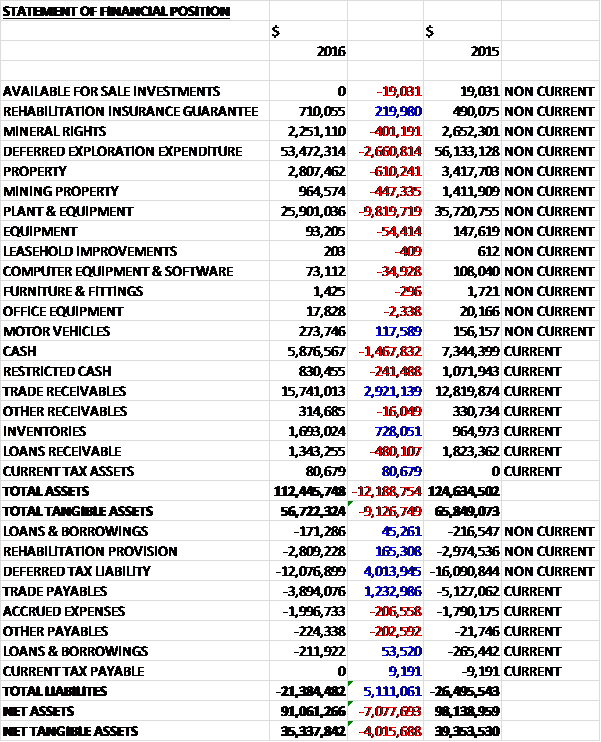

When compared to the end point of last year, total assets declined by $12.2M to $112.4M, driven by a $9.8M fall in plant & equipment, a $2.7M decrease in deferred exploration expenditure and a $1.5M decline in cash, partially offset by a $2.9M growth in trade receivables. Total liabilities also fell during the year due to a $4M decline in deferred tax liabilities and a $1.2M decrease in trade payables. The end result was a net tangible asset level of $35.3M, a decline of $4M year on year.

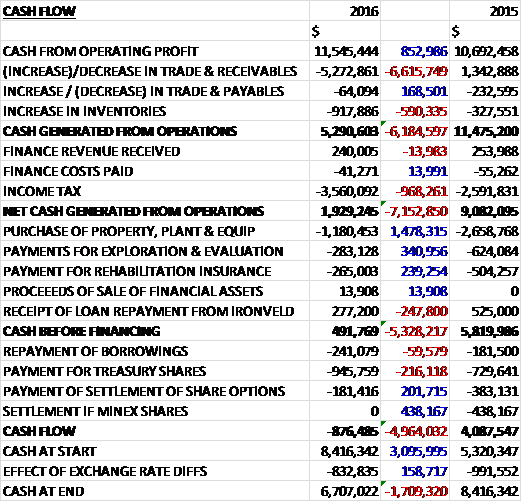

Before movements in working capital, cash profits increased by $853K to $11.5M. There was a large cash outflow from working capital, with an increase in receivables and after tax payments increased by $968K, the net cash from operations was $1.9M, a decline of $7.2M year on year. The group spent $1.2M on property, plant and equipment, $283K on exploration and $265K on rehabilitation insurance but they received $277K in loan repayments from Ironveld to give a free cash flow of $492K. After the group then spent $946K on shares for employee awards, $181K on the settlement of share options and $241K in repaying loans, the cash outflow for the year came in at $876K and the cash level at the year-end was $6.7M.

The segment result at Millsell was $2.8M, a growth of $162K year on year; the segment result at Steelpoort was a loss of $823K, a detrimental movement of $1.5M when compared to last year; the segment result at Lannex was a loss of $1.6M, broadly similar to 2015; the segment result at Mooinooi was $1.2M, an improvement of $1.4M year on year despite some production interruptions from an electrical substation fire; the segment result at Doornbosch was $2.9M, an increase of $81K when compared to last year; the segment result at Tweefontein was $3.2M, a growth of $1M when compared to 2015.

The past year was characterised by further declines in platinum prices with the year opening at $1,082 per ounce, dropping to $814 in January and ending the year back at $1,021 per ounce. The group produced 60,643 ounces this year, an increase of 5% over 2015 and cash costs per ounce decreased by 28% to $437 per ounce. Group EBITDA in H2 rose to $7.2M from $3.6M in the first half of the year.

While the overall plant feed head grades were slightly higher than in last year, the PGM feed grades were 5% lower at 4.03g/ton. Plant feed tons for the year were up 2% to 2,179,468 tons and PGM plant recovery increased by 13% to 43%. More disciplined production management, improved plant stability and continuous proves improvement initiatives helped maintain stable feed tonnages and achieve the higher PGM recovery efficiencies. The group are now able to build on this by expanding their metallurgical plant infrastructure in order to achieve higher process efficiencies at lower overall production costs through the execution of project “Echo” which aims to transform the Millsell, Doornbosch, Tweefontein and Mooinooi dump and ROM operations from single stream milling and flotation circuits to primary and secondary milling and flotation circuits over the next two to three years.

A year-long strategic review of the tailings retreatment operations, which is made up of between 60% and 70% of dump material, and 30% to 40% of current arisings, has revealed an opportunity to maintain PGM production of around 60,000 ounces and substantially prolong group production at this rate for many more years subject to the host mine holding chrome output at a steady state.

Project “Echo” addresses the SDO’s diminishing and finite life and focuses on improving PGM

recovery efficiencies by adding secondary milling and flotation modules to existing operations over the next two to three years. Without this, current SDO operations will tail off to about 40,000 ounces by 2021. Capex of about $12M, to be funded from group cash flows, will be spent over the next four years to bring this project to fruition.

At Harriet’s Wish, Aurora and Cracouw exploration, the group submitted financial guarantees in order to provide for the reduced financial security for rehabilitation as required by the DMR, and notarial execution of the mining right for this project occurred in December. In terms of the MPRDA application to transfer the right to mine iron ore, vanadium and heavy minerals to Ironveld was granted in April. They also concluded the notarial cession of this right and the documents were lodged with the Mining Titles Office for registration. The group intend to proceed with a water use license application but this process will be delayed as transfer of the title deeds from the deceased original landowners to lawful occupants and descendants will need to be facilitated.

At Volspruit, in Q1, a biodiversity and wetland offset strategy was delivered to LEDET and the DMR. This forms the basis of implementing remediation towards zero net impact should planned mitigation during the mine’s operation prove to be insufficient. In the form of an addendum to the environmental impact assessment, the documents were submitted together with the comments and responses report following public review. Unfortunately, in Q3 the group was informed that the EA application had been refused. Their advisors believe that the reasons for the refusal indicated that LEDET had not duly considered the contents of the addendum and they submitted an appeal in June.

They continue to await the outcome of the mining right application from the DMR, believing that a decision will be reached when the appeal of the EA has been concluded. They intend to proceed with a WULA although this will require preliminary detailed civil designs of all dam facilities. As this will incur additional costs, it has been postponed pending the decision on the MRA and EA.

At Grasvally, a mineral resource statement, which declared a resource over the entire strike length of 5.2km of the known chromite body on the prospect of the project, was completed in Q2 which was necessary to exercise a mining right over the resource. The MRA for Grasvally was submitted in Q1 and public participation meetings were held in February. Stakeholders at these meetings requested an assessment of potential loss of agriculture and income should the project proceed. The DMR then granted a 50 day extension to the submission of the EIA, which was finally submitted in May with the decision being awaited.

In addition, the WULA for the opencast mining and waste rock treatment was submitted to the Department of Water and Sanitation in June and they also await a decision on this application. During Q2, the group announced that they intended to sell this asset. An international agent was appointed to manage the process but unfortunately due to the recent performance of the chrome market, potential purchasers have been slow to show an interest, although this is expected to change as the market improves.

Dump reprocessing remains the primary focus of the group and the board see insufficient tangible improvement in capital markets to warrant exploration and the board has indicated that they would sell the Grasvally chrome opportunity. Progress on this has slowed due to continued difficult chrome market conditions. There are signs that chrome ore markets are recovering and there is renewed interest in the Grasvally project but the board will not rush into a process that does not capture the full value of the project.

During the year, project development costs of $150K were spent in examining an opportunity outside South Africa in a related business for the reclamation of value from substantial dumps but given to political risks and uncertainty attached to the project, the group decided not to proceed.

Community protests have had some impact on operations this year.

Interestingly the chairman has commented on the decline in the share price. He has re-iterated that the company will not be seeking further funding but notes that there has been some sell-down among the group’s larger shareholders, mostly as a result of portfolio adjustments and an ongoing weak AIM market.

Platinum demand has ended its fourth successive year in deficit while supply rose 19%. The group believe the refusal of South African producers to match supply and demand has continued to cause platinum to sink below the $900 per ounce mark during the year. Platinum demand is, however, growing in tandem with the automotive sector while jewellery is starting to show signs of life due to the collapse in price. Despite this, above ground stocks continue to fund deficits and no meaningful price activity is evident.

Obviously the group is very susceptible to the change in platinum group metals. A 10% movement would lead to an $827K increase or decrease in profits. The group is also somewhat susceptible to changes in the South African Rand which is something to bear in mind. Weakness means a decline in most costs but also a fall in the value of assets.

After the year-end, in July, the DMR approved the Section 11 application to transfer the portion of the Mining Right held by Hacra Mining and Exploration for heavy metals, iron and vanadium to Ironveld in terms of the Ironveld transaction entered into in August 2012.

Going forward, based on current resources, plant infrastructure and operational performance, the group should have a similar production performance next year, and with planned expansion projects over the next few years, they should be able to maintain production levels at around 58,000 to 60,000 ounces for many years going forward.

At the current share price the shares are trading on a PE ratio of 10.2 but unfortunately I can’t find any forecasts for the coming year.

Overall then this has been a bit of a mixed year for the group. The profit actually increased year on year due to lower costs, perhaps related to Rand weakness. Net assets declined, however, and the operating cash flow decreased due to a large growth in receivables. The cash profits increased but there was no free cash flow of note. Operationally all of the plants seem to have improved performance apart from Steelpoort – there is no indication as to what happened there to give such a poor outturn.

The platinum price finished the year about where it started – at $1,021 per ounce but on average was much lower than the prior year and unless some supply is taken out of the market, it seems unlikely that a huge amount of headway will be made. Thankfully the group has been able to slash costs, with cash operating costs down to $437 per ounce. They have also been able to maintain production at around 60,000 ounces per year but in order to sustain this, they are going to have to spend $12M on installing secondary milling and flotation modules.

Some of the exploration assets seem to be running into difficulties with licenses so hopefully that can be sorted, and the sale of the Grasvally asset has made slow progress, which is apparently improving now. A ball park figure of what this might bring in if sold would be helpful. With a PE ratio of 10.2, this probably seems about right for now, unless real progress can be made with the Platinum price.

On the 26th October the group released an update covering trading in Q1. The group achieved a new production record of 17,257 ounces in the quarter, representing a 6% increase over Q4 last year and the gross basket price increased 9% to $937 per ounce. The operating cash cost increased slightly to $408 per ounce due to a stronger Rand/$ exchange rate. Revenue increased by 23% to $13M,

Improved PGM recovery efficiencies for the quarter contributed towards higher PGM production despite the PGM feed tonnes and grades being slightly lower than in the previous quarter. The group cash balance at the end of the quarter was $11.1M, a $4.4M increase on the end of the year. Cash generated from operations before working capital movements was $5.6M with movements in working capital reducing this by $1.4M.

Doornbosch and Tweefontein achieved higher PGM recoveries as a result of improved flotation stability and mass pull strategy, while Mooinooi and Lannex achieved higher recovery efficiencies due to improved residence times associated with lower PGM feed tonnes for the quarter. The PGM feed tonnes were slightly lower due to difficulties experienced with the hydro mining at Lannex and lower plant feed stability at Mooinooi, both of which have subsequently been resolved. This has all led to EBITDA increasing by 49% to $5.9M.

At Volspruit, following the submission of an appeal against the decision not to grant Environmental authorisation, the group has also submitted an answering statement in response to comments received from interested and affected parties. They now await a decision as to whether an EA will be granted for the project. At Harriet’s Wish, Aurora and Cracouw, the notarial cession of the right to mine iron ore, vanadium and heavy minerals in favour of Ironveld has been registered in the Mining Titles Office and the company remains hopeful that a mining right of PGMs will be granted shortly.

At Grasvally, the Department of Mineral Resources has granted an amendment to the existing prospecting right to include the processing of the old waste rock dumps. The department of Water and Sanitation visited the site and was provided with an update and status report of prospecting, the development plan and the risks associated with delaying the application. The application is now in its final stages and it is hoped that the issuing of the water use license for processing the waste rock dumps will be issued soon.

On the 30th January the group released a trading update covering the performance in Q2. The group produced 18,562 ounces, an 8% increase on the prior quarter but the gross basket price decreased 6% to $881 per ounce. The group cash cost was down 3% to $417 per ounce. Revenue decreased 11% to $11.6M as a result of the drop in the basket price, a negative price adjustment for Q1 and slightly higher PGM penalties during Q2. Capex increased 209% primarily as a result of the rollout of project Echo.

The higher production was aided primarily by slightly higher PGM feed tonnes and feed grades while the recovery efficiency was slightly down from the previous quarter’s record performance. Based on this solid performance and the expected outlook for the rest of the year, the SDO is expected to exceed the previously stated guidance of 60,000 ounces. EBITDA for the quarter was $3.7M, representing a decline of 34% compared to Q1.

Most operations performed very well during the quarter with Lannex, Mooinooi and Tweefontein achieving the best quarterly PGM ounce production figures in their history. Doornbosch achieved slightly lower performance than the previous quarter, associated with the repositioning of its hydro-mining pump station at the dam. The hydro-mining stability and tonnage feed rates at Lannex and Steelpoort improved during the quarter based on optimisation initiatives with contributed to the overall increase in PGM feed tonnes.

The secondary milling and flotation technology rollout will lead to improved PGM recovery efficiencies, lower PGM production unit costs, increased cash generation and enable the SDO to extend its profitable operating life and to sustain its production profile at 55,000 to 60,000 ounces going forward.

Overall then, operationally things are going well but costs have not fallen as fast as revenues so the lower basket price is hurting the group a bit – perhaps now is not the right time to invest.