Gemfields is a miner of coloured gems, specifically emeralds and amethysts from Zambia and Mozambique rubies. The group’s assets include Kagem Mining, a 75% owned (the Zambian government owns the other 25%) producer of emeralds which happens to be the world’s largest accounting for 20% of global production; Montepuez Ruby Mining, a 75% owned (25% by Mwiriti) ruby licence in Mozambique thought to have the potential to produce about 25% of the world’s rubies when up and running; Faberge, acquired in 2013 that enables the group some control over the end users of the gems they mine; Kariba Minerals, a 50% owned (50% ZCCM Investments) amethyst mine in Zambia and various exploration licences covering emeralds, rubies, sapphires and garnets in Madagascar. They have now released their full year results for 2014.

Revenues were up across all business sectors with Zambia revenue more than doubling to $87.8M and Mozambique posting a maiden £33.5M revenue. There was a $29.8M increase in purchases/inventory and a $6.7M increase in royalties and taxes but the gross profit was still some $71.4M higher than last year. Labour costs increased by $8.9M with rent and marketing costs also increasing to give a profit before tax some $56.4M better than last year before a $17.3M increase in tax meant that profit for the year increased by $39.1M to $16.3M.

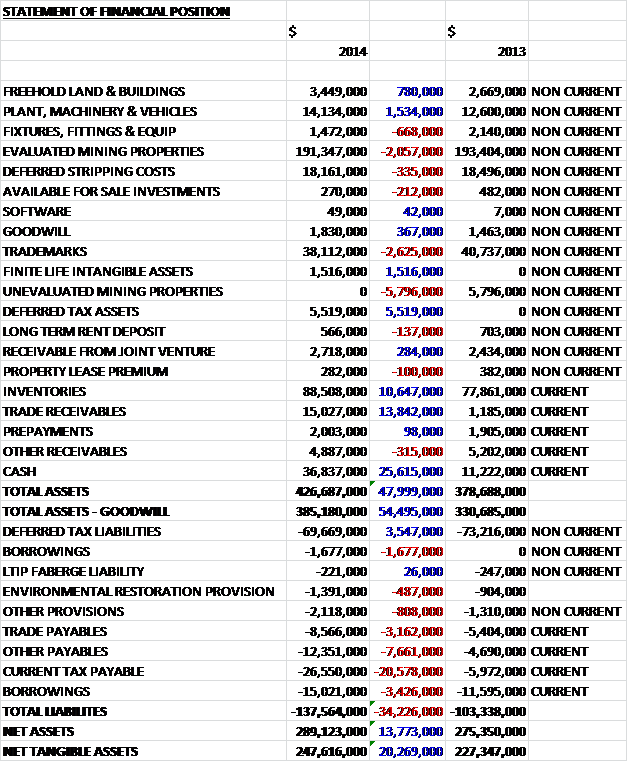

When compared to last year, assets increased by $48M, driven by a $25.6M increase in cash, a $13.8M growth in trade receivables and a $10.6M increase in inventories, partially offset by a $5.8M reduction in unevaluated mining properties as properties were evaluated and transferred to tangible assets. Liabilities also increased during the year, mainly due to a $20.6M increase in current tax payable and a $7.7M growth in other payables. These changes meant that net tangible assets increased by $20.3M to a healthy $247.6M.

Before movements in working capital cash profits of $62.5M were some $59M ahead of last year. A large increase in receivables and a near doubling of tax was offset slightly by an increase in payables so that net cash generated from operations was $45.7M, a $64.5M reversal on last year. Out of this cash the group purchased $3.7M of intangible assets, $8.7M of tangible assets and spent $7.6M on stripping costs (costs incurred in opening up new ore areas) to give a cash flow before financing activities of $25.5M. A maiden dividend was paid to the Zambian government, which was counteracted by a net $5M of new borrowings to give a very strong cash inflow of $26.1M compared to the $25.8M outflow in 2013.

The market for coloured gemstone is robust and there is a rising consumer demand in globally, particularly in the US, China and the EU. This has led to an increase in price for emeralds, which the group expect to see continuing

Profits in Zambia amounted to $28.3M, an increase of $21.4M over last year. During the year Kagem completed its third high wall push back and commenced its fourth in order to extend the pit size by a further 75 metres and to open up new areas of ore for future production. The programme is expected to deliver four years of open pit ore production and increase the overall rate of mining. Decent volumes of ore and gemstone production were achieved in the first half of the year but the second half was impacted by high rainfall, grade volatility and delays in initiating the fourth phase of the pushback programme. During the year gemstone production fell by 33% to 20.2M carats of emerald and beryl. There is a trial underground mining project at the mine but ground conditions have been challenging, slowing the rate of the project. A total of 184,935 carats were produced, less than half that of last year and due to the continued viability of open pit operations, it is likely that in the short term underground mining is only going to continue on a trial basis. During the year, $2.9M was invested in new mining and other equipment at Kagem, including the washing plant and security arrangements.

Exploration-wise at Kagem, in Libwente it has been established that the Mesoproterozoic Muva sequences containing pegmatites, quartz and quartz-tourmaline has high levels of potential and at Fibolele a second phase of bulk sampling identified gemstone producing structures. Kagem held three emerald auctions and completed one direct sale of material during the year. The first auction held in Zambia auctioned higher quality stones where all 583,448 carats were sold generating $31.5M and achieving $54 per carat. The second auction held in Zambia was of lower quality rough emeralds and beryl and saw 4.94M carats being sold generating $16.4M of revenue at $3.32 per carat. The third auction saw 620K carats of higher quality emeralds being sold, generating $36.5M at $59.3 per carat. The direct sale involved 11,286 kg of Kagem’s lowest quality beryl that had failed to sell at auction for $3.5M. After the end of the balance sheet date, another auction was held for lower quality emeralds and beryl which raised $15.5M at an average price of $3.61 per carat, which was a decent improvement over the last lower quality material auction.

At the Kariba amethyst mine, the Zambian governments transferred its 50% stake to ZCCM Investments, in which they own an 87% holding. A number of factors have impacted the mine’s development and both joint venture partners have provided a further $200K during the year after providing $1.25M each in the prior year for new equipment and improved infrastructure and as of the end of the year, all of the major rehab, capital and construction projects have now been completed. These improvements have led to the quantity of commercial and medium quality production increasing by 70%. After positive bulk sampling results, a new virgin area lying between the two older pits is now being mined and a new CCTV system has been installed.

Profits in Mozambique were $14.4M, an improvement of $19.4M over the loss incurred in 2013. Bulk sampling during the first part of the year concentrated on the Maninge Nice, Central and Glass A areas but during Q4, there was a shift in focus towards the newly discovered Mugloto area where the overall grade is lower but the quality of rubies is higher, the result being a decline in the total number of carats mined but an increase in overall value. In total approximately 6.5M carats of ruby and corundum were extracted and the total cash operating costs were $10.9M and cumulative project expenditure stands currently at $34M with a resource and reserve statement expected by mid-2016. The first auction for rough ruby and corundum was held in Singapore and comprised both high and lower quality material. In the auction, 1.82M carats were sold and revenues of $33.5M were generated at a price of $18.43 per carat which means that the revenues from this first auction alone have nearly covered the costs of the whole project.

One problem the group has been having with the Montepuez ruby mine is that of security. The license area is big and the stones are close to the surface which has encouraged illegal mining on the site. The improved security arrangements involving the local security team, external security contractors and the Mozambique police have been reasonably effective in reducing the numbers of illegal trespassers compared to when the group took the license over.

Losses in the UK were $32M, an increase of $16M compared to the losses last year. Faberge losses were $15.1M, a deterioration of $7.8M compared to the losses in 2013. During the year the division underwent a successful transition with efforts focused on containing costs, improving product flows and increasing customer understanding with the group also looking to leverage Faberge’s global growth potential. The division has created a number of new designs and launched several events and advertising campaigns in order raise awareness in the brand, including raising a considerable amount of money for charity. In April, a significant marketing event was hosted in Harrods which generated record monthly sales for the Faberge concession in the store. The division’s cost to the group remains within budget and new products were well received by customers across key markets.

Other profits, relating to traded auctions, sales and marketing offices, were $20.7M, an improvement of $22M when compared to the small loss last year. The first standalone traded emerald auction held in India saw 145,952 carats of high quality traded rough emeralds sold generating $8.5M at $58 per carat. The second traded emerald auction, also held in India, comprised of high quality Zambian and Brazilian emeralds and saw 268,000 carats sold generating $13.5M. Following the presidential election and the resulting improving security environment the group now expects to increase activity in its exploration assets in Madagascar next year.

There are a number of risks that coma along with this kind of business. As with any commodity business, the group is affected by gemstone prices and demand which are linked to world economic conditions. Operating in Africa comes with political and security risk and tax changes could be enacted with little warning. Only last year the Zambian government decided that all auctions had to take place within the country. There is a risk of theft from the mines, as has been seen at the ruby mine in Mozambique in recent years.

The group has a number of capital commitments outstanding including $4.7M for the purchase of mining equipment in Kagem, $26.3M for the overburden removal in Kagem and $3.6M for the purchase of mining equipment in Montepuez. The group has a major shareholder in the form of PRF, a subsidiary of Pallinghurst Resources, who own 47.9% of the group which gives them some influence over the Gemfields, although an agreement has been set out whereby they are manages autonomously and operated for the benefit of its shareholders as a whole.

After the end of the balance sheet date the group entered into a joint venture with EWGI in order to progress opportunities in the Sri Lankan sapphire and gemstone sector via three Sri Lankan subsidiaries which will be 75% owned by Gemfields. Under the agreement, the company has a 75% interest in 16 exploration licences for a consideration of $400K.

At current share price the P/E ratio stands at a hefty 47.8 but this reduces to 17.8 next year, still on the high side but there is a lot of growth factored in. There is no doubt that this has been a good year for Gemfields. The Zambian operations continue to be profitable with more recent auctions obtaining better prices and the Ruby mine in Mozambique seems to be making good progress with the first auction revenue already covering project costs. The net assets increased by $20.3M and there was a very strong cash inflow which is always good to see. It is still early days for the ruby mine though, and the thefts are a bit of a concern. Additionally, there seems to be a lot of overburden removal to be factored in, although this could be normal as I don’t have the knowledge of the industry to decide. Overall then, this seems to be a great looking business, although probably fairly priced, which I may look to enter on any share price weakness.

On the 14th November the group released a statement covering the first quarter of the year. The Kagem mine yielded 6.3M carats with operating costs of $1.48 per carat, an increase on the $1.06 per carat during the same quarter of last year. The fourth phase of the high-wall pushback programme continued to progress well but illegal mining activity within the boundaries of the licence continue and the group are working with key ministries to combat the issue. August saw an auction of lower quality rough emerald and beryl with 11.6M carats being sold, generating revenues of $15.5M. The average price was $1.34 per carat but increased to $3.61 per carat when the sale of the low grade beryl was excluded. The next auction is schedule for the 17th November.

At the Montepuez ruby mine the core infrastructure is largely in place and progress was made towards formalised mining. About 2.9M carats were extracted during the quarter as part of the bulk sampling operation, which was flat year on year due to the lower grades of ore being mined. This also helped explain the increase of unit operating costs from $0.62 per carat last year and $1.48 per carat this quarter. Unlicensed mining activity and asset loss remained a problem during the period but the ongoing security efforts have resulted in an improvement in the situation. The next auction for rubies is scheduled to take place in Singapore in December.

Faberge saw the value of its orders increase by 50% when compared to the same quarter of 2013 and operating costs were 26% lower. The division also completed the relocations of its Geneva boutique. The business introduced a new product category, Objects, with product launches expected in the second half of 2015. At the end of the period the group held cash of $32.2M with total debt of $25.1M including the outstanding balance of $15M at Kagem. Overall market conditions remained upbeat with ongoing enthusiasm from customers although during the period, the president of Zambia passed away which has the potential to cause some instability in the short term.

On the 18th November the group issued a statement covering their auction of higher quality emeralds in Lusaka. The group sold 530K carats generating revenues of $34.9M, and although this was slightly lower than the last auction of higher quality emeralds, it does represent the second highest achieved to date and the overall value of $65.89 per carat was a record.

On the 9th December the group issued a statement covering the auction of higher quality rubies in Singapore. The auction sold 62,936 carats and achieved sales of $43.3M at a remarkable $688.64 per carat. As part of this auction, an exceptional 40.23 carat rough ruby was sold, with the price remaining undisclosed. The next ruby auction will take place before the end of June and will consist of lower quality ruby and corundum. The sales achieved at this auction represent the highest ever that the group has conducted which is clearly an excellent achievement but it will be some time before another auction of high quality rubies takes place.

On the 15th December the group announced the completion of the acquisition of two individual ruby licences in Mozambique. The licensed will be controlled by a new joint venture, of which Gemfields owns 75% with the other 25% being owned by the vendor, EME Investments. The group paid $3.5M for the two licences, both of which border the existing Montepuez ruby deposit and cover 19,000 and 15,000 hectares.

On the 17th February the group released a statement covering Q2 2015. The Kagem mine produced 5.8M carats of emerald and beryl compared to 3.9M carats in the same period of last year. The grade of 190 carats per tonne was lower than the 224 carats achieved previously due in part to the bulk sampling at the new pits of Fibolele and Libwente. Total operating costs increased by $4.4M due to increased mining activity and unit operating costs increasing from $1.85 per carat to $2 per carat.

The fourth phase of the high-wall push back programme in the main Chama pit continued to be advanced with a total of 4.1MT of waste rock moved during the quarter and it now looks like the project will be completed ahead of schedule. After contributing to the understanding of underground mining conditions in Zambia, the trial underground mining project at Kagem was put on care and maintenance and will lead to a detailed underground mine plan. In the interim, there is flexibility to extend the open pit operations with further push backs. The exploration and bulk sampling activities at the new Fibolele and Libwente pits are progressing well but illegal mining within the boundaries of the Kagem licence are not yet resolved and the group continues to work with key minitries to put an end to the problem. The next emerald auction will be of lower quality rough diamonds and beryl and is scheduled to take place during the last week of February.

The Montepuez ruby mine produced 3.4M carats of ruby ans corundum compared to 2.3M carats during the same period of last year. The grade of 34 carats per tonne compared to 64 last time was partly due to the processing of lower grade portions of the washing plant stockpile. Total operating costs were $5.7M, an increase of $3.4M due to the increased mining activity and unit operating costs fell to $5.24 per tonne with the increased scale of mining driving efficiencies. Bulk sampling at the project continued to provide positive results and further insight into the geology of the deposit and with the core infrastructure largely in place, progress is being made towards formalising mining. Due to the size and nature of the license, illegal mining activity and asset loss remains a key challenge but new infrastructure, a significant security presence and ongoing efforts have resulted in a strong improvement.

During the quarter the group completed the acquisition of controlling interests in two additional ruby deposits in the Montepuez district of the Cabo Delgado province in Mozambique. The licenses are valid for an initial period of 25 years and a new company was formed with the Mozambique government in which Gemfields has a 75% controlling stake. The two licenses do not border each other but do share a boundary with the existing Montepuez deposit and cover 18,400 hectares and 14,900 hectares respectively. The next ruby auction will be of lower quality rough ruby and corundum and is scheduled to take place in India in March.

Faberge seems to have struggled during the year. With a short term shift of focus to various key initiatives set to be rolled out during the second half such as the new updated jewelry collections along with a material decrease in sales from Ukraine and Russia due to the political developments in the region, the value of orders agreed during the period fell by 12% when compared to the same period of last year. Operating costs were 5% lower, however and the business is about to unveil four new watch collections created in collaboration with two leading Swiss manufacturers which will be introduced at the Basel World jewelry and watch fair in March.

In Sri Lanka, a trading license has been obtained and a token shipment of sapphires was made to the group in London. They are in the process of establishing initial infrastructure in Sri Lanka and initiating preliminary geological assessments in areas of interest. At the end of the quarter the group has cash levels of $49.2M and outstanding debt of $30.3M which compares very favourably to the $7.1M of net cash held at the end of last quarter. The board remain upbeat about growth and development in the sector and this along with the increase in cash, potential step up in Ruby production and the new sapphire venture seems to suggest there are still exciting times ahead for the group but I feel with just the lower quality auctions coming up and the difficulties at Faberge, there could be some short term turbulence so I am keeping a watching brief here for now.

On the 2nd March the group announced the results of the rough emerald, beryl and amethyst auction. The emerald auction saw $14.5M generated at an average value of $3.72 per carat which is a new record for the lower quality stones. The downside is that they only managed to sell 3.9M carats, or 39% of the stones offered with the rest not receiving bids. The amethyst auction was the first to be held in Zambia and it saw 27.7M carats of higher quality amethysts offered with the majority being sold at 1.77c per carat, generating $450K. The auction of lower quality rubies is taking place later this month. Whilst the price generated per stone is very good, it is a little disappointing to see that the majority of the emeralds did not sell.