Goodwin has now released their interim results for the year ending 2019.

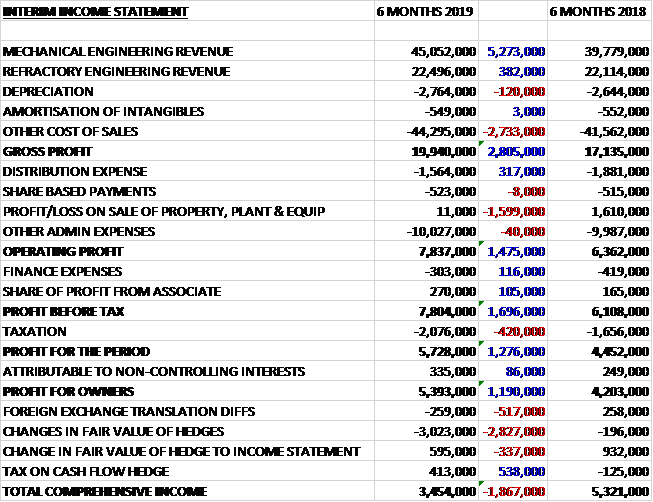

Revenues increased when compared to the first half of last year due to a £5.3M growth in mechanical engineering revenue and a £382K increase in refractory engineering revenue. Depreciation was up £120K and other cost of sales increased by £2.7M to give a gross profit £2.8M. Distribution expenses declined by £317K but there was a £1.6M reduction in profits from the sale of property relating to last year’s sale of land in India, plant and equipment which meant the operating profit was £1.5M higher. Finance expenses were down £116K and there was a £105K growth in profits from associates and after tax charges increased by £420K the profit for the period came in at £5.4M, a growth of £1.2M year on year.

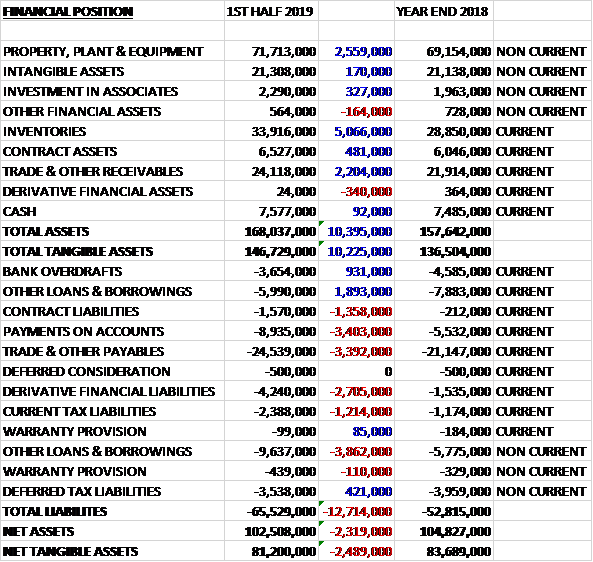

When compared to the end point of last year total assets increased by £10.4M driven by a £5.1M growth in inventories, a £2.6M increase in property, plant and equipment and a E2.2M increase in receivables. Total liabilities also increased due to a £3.4M increase in payments on accounts, a £3.4M growth in payables, a £2.7M increase in derivative financial liabilities, a £2M growth in loans and a £1.4M increase in contract liabilities. The end result was a net tangible asset level of £81.2M, a decline of £2.5M over the past six months.

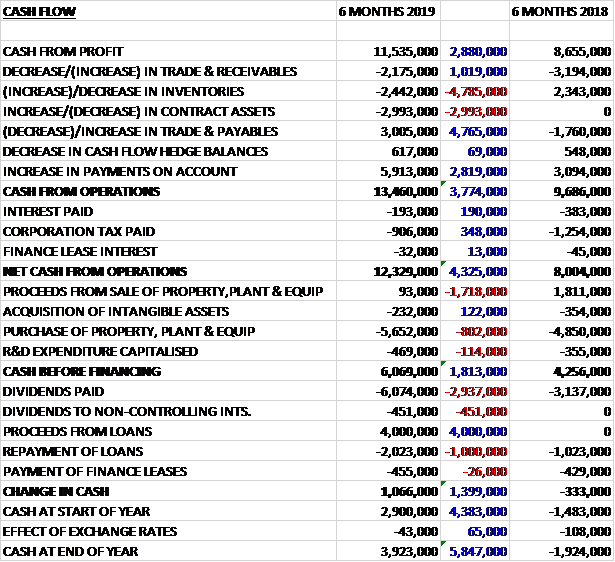

Before movements in working capital, cash profits increased by £2.9M to £11.5M. There was a cash inflow from working capital which was slightly better than last time and after interest declined by £190K and tax payments fell by £348K the net cash from operations was £12.3M, a growth of £4.3M year on year. The group spent £5.7M on property, plant and equipment, £469K on R&D and £232K on acquisitions to give a free cash flow of £6.1M. This was all paid out in dividends so a new £2M loan offset £455K of finance lease payments to give a cash flow of £1.1M and a cash level of £3.9M at the period-end.

The profit in the mechanical engineering division was £4.5M, a growth of £1.8M year on year. The profit in the refractory engineering division was £4.9M, a decline of £459K when compared to the first half of last year.

The current work load stands at £99M compared to £84M a year ago. The order book continues to improve in both quantity and quality of earnings in both divisions. The oil and gas order input is stable and the increase on the mechanical engineering side of the business relates to new markets such as naval shipbuilding and nuclear waste reprocessing. Prior to the end of the first half of the calendar year the group expects to win some substantial orders that will allow activity to take a step forward.

Going forward, group activity and profitability levels are expected to increase over the next year. Whilst there is an increased workload the board expect the second half profits to be similar to the first half as it will take about six months to ramp up the activity levels and take the work through first piece sample approvals. Subject to significant new business being won, however, they expect 2020 to be busier and more profitable than 2019.

The activities in India continue to grow and to accommodate further growth of their pump and investment casting powder manufacturing activities there they have purchased 2.6 more acres of land adjacent to their four acre site to accommodate the further expected growth over the next three years.

At the current share price the shares are trading on a PE ratio of 28.3. I can find now forecasts but if we assume the second half will come in close to the first we are looking at a PE ratio of 20.6 for the year. Last year the shares yielded a dividend of 2.7%.

Overall then this has been a good period for the group. Although net assets declined, profits were up and the operating cash flow improved with enough free cash generated to just about cover the dividends. The good performance is due to mechanical engineering markets such as shipbuilding and nuclear waste decontamination. In addition, the work load is increasing and some substantial orders are expected to be received shortly. Business seems to be booming but this is reflected in the price of the shares with a PE of 20.6 and dividend yield of 2.7%. They look to be priced about right to me.

On the 2nd April the group announced that it had finally developed a silica free investment casting powder for which it has applied for a patent. This new powder can be used by jewellery manufacturers to cast gold, silver and brass jewellery castings without them having to change any of their existing equipment. This is the conclusion of over six years of R&D work and will allow casting manufacturers to work in an environment free of respirable silica.

This will allow the group to address the jewellery investment casting manufacturing market in the US as until now it had been forbidden for any group business to sell products containing respirable silica into the country. As the product is a premium one, it should allow an improvement in gross margin and profits earned in the refractory division over the coming years.