Redrow has now released their interim results for the year ending 2019.

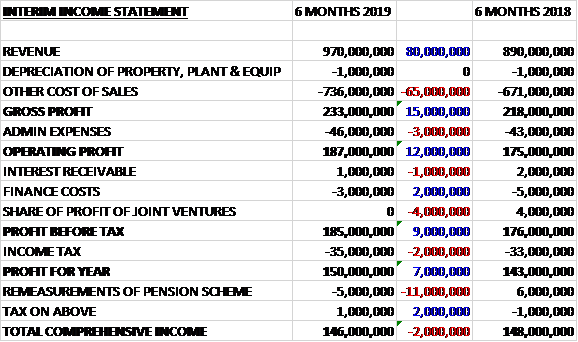

Revenues increased by £80M when compared to the first half of last year. Cost of sales also increased to give a gross profit £15M higher. Admin expenses were up £3M but net finance costs reduced by £1M. After a £4M reduction in joint venture profits and a £2M increase in tax charges, the profit for the period came in at £150M, a growth of £7M year on year.

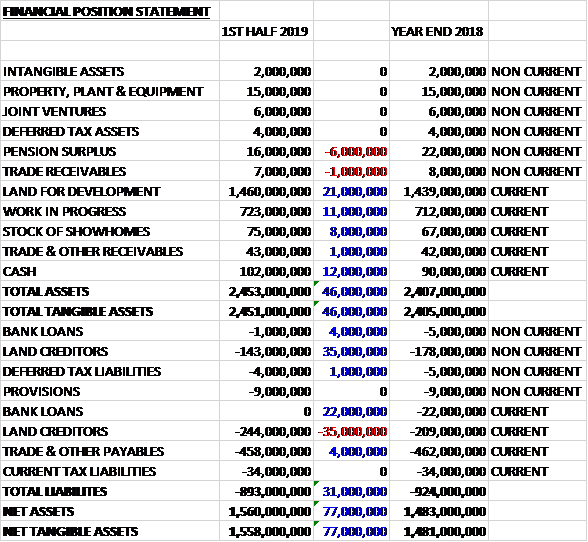

When compared to the end point of last year, total assets increased by £46M driven by a £21M growth in land for development, a £12M increase in cash and an £11M growth in work in progress. Total liabilities declined during the year due to a £26M reduction in the bank loan. The net tangible asset level was £1.558BN, a growth of £77M over the past six months.

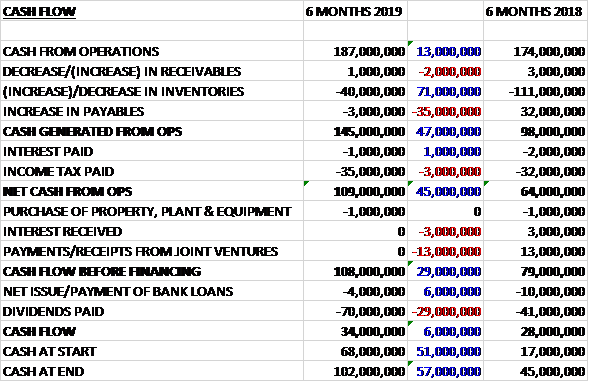

Before movements in working capital, cash profits increased by £13M to £187M. There was a cash outflow from working capital but this was lower than last year and after tax payments increased by £3M the net cash from operations was £109M, a growth of £45M year on year. The group spent just £1M on capex to give a free cash flow if £108M. They then spent £4M on paying back bank loans and £70M on dividends to give a cash flow of £34M and a cash level of £102M at the period-end.

Revenue from private legal completions increased by 4% and from affordable completions nearly doubled. The average selling price of their private homes increased by 4% and affordable homes by 15%, mainly due to the growth of the Southern business.

The sales rate per outlet per week for the period was 0.61 compared to 0.64 in the first half of last year. Sales were negatively affected towards the end of the year as a result of the political uncertainty surrounding Brexit and the effect of high stamp duty, which has disrupted the normal trade up/down sizing market. Despite this the value of reservations in the period was in line with last year.

At the end of the year they had a record order book of £1.2Bn, up 11% on December last year and over the period they have experienced a reduction in cost pressures with sub contract, materials and labour markets all easing.

They continue to see good opportunities in the land market but have taken a cautious approach to land acquisition, preferring to concentrate on select sites. Their owned and contracted current land holdings are in line with the end of last year at 27,540 with the forward land holdings of 30,500 also in line.

The market during the run up to the festive period and the first two weeks of 2019 was subdued by macroeconomic and political uncertainty but sales over the last three weeks have bounced back with reservations running at similar levels to last year’s strong market activity. Overall private sales for the first five weeks of 2019 were down £10M but given the record £1.2BN order book the board are confident that this will be another year of significant progress for the group.

The board are proposing a 30p per share cash return through a B share scheme.

At the current share price the shares are trading on a PE ratio of 7.1 which falls to 6.8 on the full year consensus forecast. After an 11% increase in the interim dividend the shares are yielding 4.9% which increases to 6.3% on the full year forecast. At the period-end the group had a net cash position of £101M compared to £63M at the year-end.

Overall then this has been a strong period for the group. Profits were up, net assets increased and the operating cash flow improved with plenty of free cash being generated. Both completions and prices were up in the period but Brexit has caused the market to slow down over Christmas. It seems to be back to normal now though, the order book is good and cost pressures are down. The forward PE of 6.8 and yield of 6.3% also looks good value. Of course, Brexit is looming large and buying a housebuilder at this time carries some risk but these shares look too cheap to me and I think I might buy back in.