Goodwin has now released its interim results for the year ending 2015.

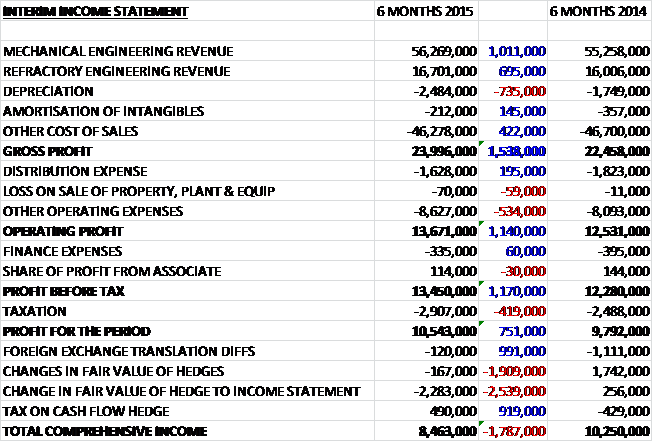

Overall revenues increased year on year driven by increased Pacific Basin and other Europe sales with mechanical engineering up £1M and refractory engineering increasing by £695K. We then see an increase in depreciation offset by a fall in amortisation and other cost of sales so that gross profit was £1.5M ahead of last time. A small increase in distribution expenses was then offset by an increase in other operating expenses before a slightly lower finance expense meant that profit before tax increased by £1.2M which reduced to a £751K increase to £10.5M after higher taxation increased year on year.

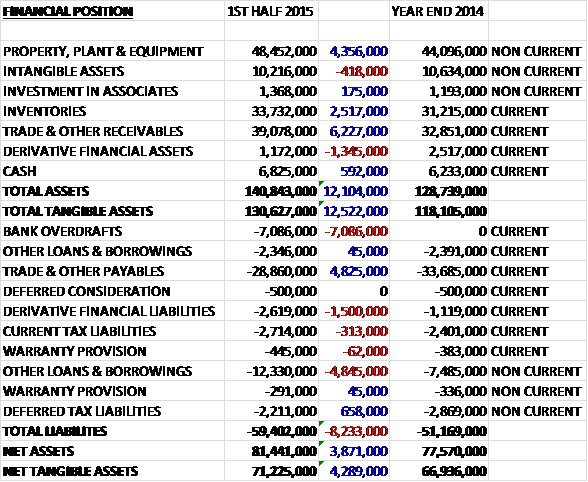

When compared to the end point of last year, total assets at the half year point were some £12.1M higher, driven by a £6.2M increase in receivables, a £4.4M growth in property, plant & equipment and a £2.5M increase in inventories which was partially offset by a £1.3M fall in derivative financial assets. Liabilities also increased during the period due to a £7.1M increase in bank overdrafts, a £4.9M growth in other loans and a £1.5M increase in derivative financial liabilities, somewhat offset by a £4.8M fall in payables to give a net tangible asset level of £71.2M, a healthy £4.3M increase and a very strong balance sheet.

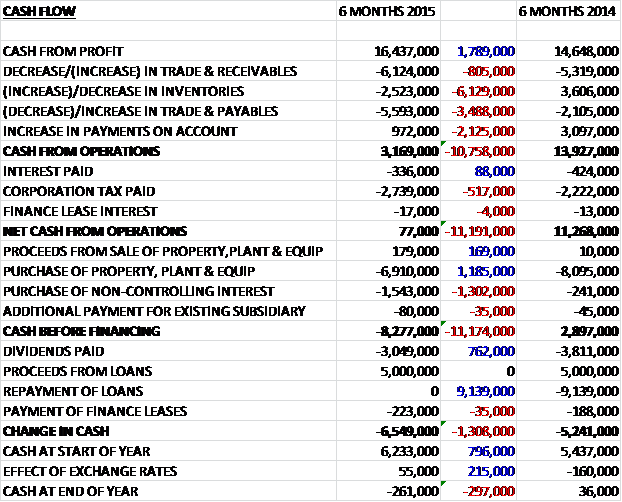

Before movements in working capital, cash profits increased by £1.8M to £16.4M but a huge outflow of working capital meant that cash from operations fell by £10.8M to £3.2M, which after an increased tax bill meant that there was barely any operational cash flow, just £77K. Clearly this was not enough to cover capital expenditure of £6.9M and a £1.5M purchase of non-controlling interests to give a cash outflow of £8.3M before financing. £5M of new loans covered the dividends but there was still a £6.5M cash outflow for the year and a negative cash balance of £261K at the end of the year but management expect to see an improvement in the cash flow position by the year end.

Mechanical engineering profits were £11.4M, an increase of £200K when compared to the first half of last year and profits at the Refractory Engineering division were £2.4M, an increase of £700K when compared to the first half of 2014. The fall off of activity in the oil and gas industry due to the lower oil prices reducing investment at oil companies continued during the period. The group started the year with a record work load of £101M but this steadily decreased as the order input fell behind sales output. This decreasing work load makes it likely that performance in the second half of the year and next year will not be as good as the first half of this year.

The investment in new machinery at Goodwin International is starting to provide benefits and is allowing the group to diversify into markets such as the UK defence industry. The Refractory division continued to grow revenue and profits which is expected to carry on in the coming years. During the period the company acquired the Indian partners’ 20% equity in Goodwin Pumps India and Gold Star Powders India which are both now 100% owned by Goodwin. In the second half of the year the group hopes to win more project engineering business for the foundry and machine shop from both civil markets and UK defence markets.

Goodwin does not pay an interim dividend so the yield remains at 1.9% from the final dividend. At the end of the period the group has a net debt of £15.4M compared to £14.9M at the same point of last year, although it was just £4.1M at the end of the year.

Overall then this is a mixed update as profits increased across both sectors and net assets improved but the cash flow was a bit of a disaster due to a large increase in receivables and a fall in payables meant there was precious little operational cash flow and certainly no free cash flow, although this was flagged up in the last update. The real problem is the falling order book due to the beleaguered oil and gas industry cutting expenditure which is likely to mean that second half performance will not be as strong as this half, a trend that is likely to continue into next year so I will keep a watching brief for now.

On the 13th March the group released a management statement covering trading in Q3. Revenues in the first nine months fell by £5.4M and profit before tax was down £700K to £17.3M. The trading situation is starting to ease down associated with reduced capital expenditure by the oil and gas companies and tighter market pricing. I think that means things are getting worse, and in Q3 trading was certainly not good as at the half year point, profits increased year on year but now they have fallen.

The chart looks pretty horrible, definitely one to wait and watch for now.