Kalibrate Technologies is a provider of price management and optimisation solutions to the fuel and oil & gas wholesale industries. The pricing division offers a comprehensive fuel pricing solution that leverages historical price, volume, competitor and market intelligence to optimise wholesale and retail fuel pricing strategies. The group’s location solutions allow clients to maximise capital investments across their store network through market and demand analysis, forecast and demand analysis across a number of revenue categories and competitive assessments. They were admitted onto the AIM exchange in November 2013 having been listed by the former parent company, Eurovestech and are headquartered in Manchester. They have now released their final results for the year ending 2014.

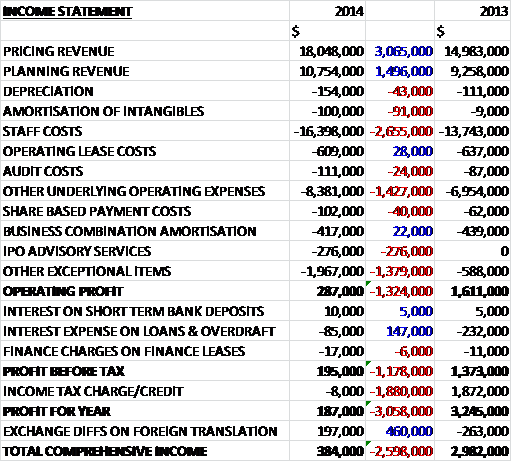

Revenues rose when compared to last year with a $3.1M increase in pricing revenue and a $1.5M growth in planning sales. We also see staff costs increase by $2.7M and other underlying operating expenses grow by $1.4M but exceptional items relating to the IPO meant that operating profit fell by $1.3M when compared to 2013 which became a $1.2M decline after finance costs but the reversal of a tax credit that occurred last year (mainly due to the recognition of previously unrecognised tax losses) meant that profit for the year fell by $3.1M to $195K, although as we have seen, this is down to non-underlying items.

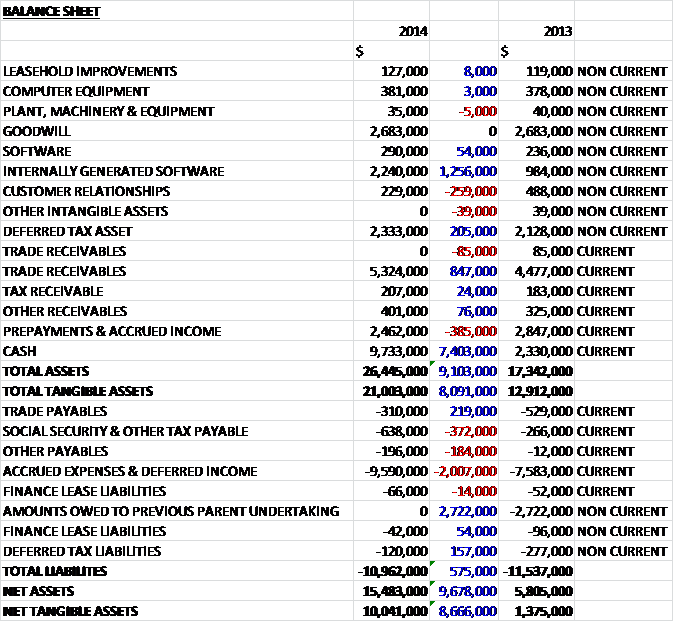

When compared to the end point of last year, total assets increased by $9.1M driven by a $7.4M increase in cash levels, a $1.3M growth in internally generated software and an $847K increase in trade receivables. Liabilities fell during the year as a $2.7M loan owed to the previous parent company was paid off, which was partially offset by a $2M increase in accrued expenses and deferred income. The end result is an $8.7M growth in net tangible assets to $10M and the $1.3M worth of operating leases are well covered here by assets.

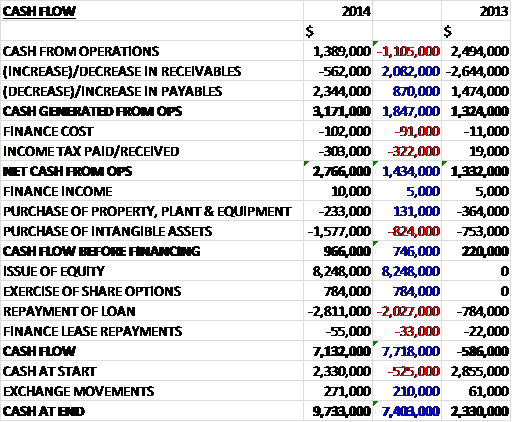

Before movements in working capital, cash profits fell by $1.1M to $1.4M but an increase in payables meant that cash generated from operations increased by $1.8M to $3.2M before this was eroded slightly by higher finance costs and tax so that net cash from operations came in at $2.8M. This was enough to cover the $1.6M expenditure on intangible assets and the $233K spent on property plant and equipment to give a free cash flow of $966K. We then see the effect of the equity issue which raised $8.2M that was partly used to pay off the loan with the rest resulting in a cash inflow of $7.1M to give a cash pile of $9.7M at the year end.

Progress has been made in increasing recurring revenues during the year which grew by $4M to $19.6M and the opening year order book stood at $22M compared to $16.3M at the end of last year. The existing client base has now grown by 12 to include 230 customers. There has also been some expansion into new geographies with a new office being opened in Thailand to support the Southeast Asian business and a new office being opened up in Melbourne, Australia. During the year the group also contracted with a third party offshore development team in Vietnam which should help accelerate the rollout of new supplementary solutions including further mobile technology and the development of new products.

The global fuel retail market is a highly competitive one and client’s exposure to price volatility and a constantly changing environment ensures Kalibrate’s products and services remain relevant. There is deregulation of fuel pricing in certain countries with the continuing emergence of compliance frameworks and future plans in some areas to deregulate represents an opportunity for the group to expand into these countries with the biggest potential prizes being China and India. The group has successfully completed their contract with the US Government’s National Renewable Energy Lab and the evolution of alternative fuels as a viable alternative to traditional fossil fuels continues with many operators now considering how best to position themselves to supply their consumers with these new fuels.

Underlying operating profit at the Pricing business was $1.6M, flat when compared to last year. Revenues did increase by 20% though driven by new client wins and improved sales into the existing client base with North America performing well. A number of clients were added in Western Europe and the rest of the world grew strongly, albeit from a relatively low base. Underlying operating profit at the Planning business was $1.4M, an increase of $300K when compared to 2013 with revenues growing by 16%. Growth has been achieved in North America, Japan and South Africa together with new areas such as South East Asia and Africa. The European planning business also expanded during the year and this is seen as a more important revenue stream in the future.

Geographically, revenues in North America grew by 30% and this region represents just over half of total sales. The pricing business won a number of new clients included a convenience retailer with more than 400 sites, and an East Coast based 300 site fuel retailer who was previously just a planning client. The data reselling business grew modestly and initial benefits are being seen after an increase in marketing efforts. Europe makes up about a quarter of total revenue and sales increased by a modest 2% with the region delivering a stronger second half performance than first half. During the year new pricing contracts were won in Germany, the Netherlands and Spain and the group was selected by a major Finnish retailer to provide both pricing and planning solutions which is the first time a combined solution was sold to a new client. Operationally the group also completed a nine-country implementation of their software to a European retailer with more than 2,000 fuel sites.

With the rest of the world making up the remaining quarter of revenues, sales here grew by 17% year on year. The core planning businesses in Japan and South Africa remained strong and was supported by growth in Oceania where the group won a SaaS Pricing contract with a 200 store retailer in New Zealand, and South East Asia where they delivered a substantial planning project across Malaysia as the country prepares for deregulation. The group also signed a combined pricing and planning contract in Morocco where their new client was keen to benefit ahead of that country’s deregulation, thereby gaining a first mover advantage in that market.

During the year the group finalised a multi-year contract with one of its existing clients to provide managed services for the petroleum retailer’s entire fuel pricing process and procedures. Also the group won a multi-country managed services contract with a global oil company under which the client will outsource the management of their entire pricing structure to the group. This represents the largest single client ever by value and will generate about $2M per annum over the multi-year term and the contract commenced in July 2014. To date the client has already started to see the benefits of moving to the new platform.

During the year the group launched Kalibrate Cloud which is a cloud based service that will incorporate all of their existing products and services together in one place. Historically the pricing product has been sold through the sale of an upfront perpetual license to a client but there is a trend for IT departments to outsource niche solution offerings and as such the group are positioning themselves to sell more SaaS subscriptions in the future which should help ensure long term client partnerships, enhance forward visibility and increase recurring revenues. As part of this strategy, they are also looking to convert existing clients to a managed services offering. This year the group cross sold their products to nine more clients so that 27 now take both pricing and planning solutions with 14 taking the managed service offering – the management reckon there is the potential for 100 of these type of contracts possible in the medium term.

I quite like it when an annual report has a case study regarding a contract. Here we have a major oil company operating in South East Asia who is looking to benchmark the characteristics and performance of its retail network against best in class global fuel retailers. The contract involved benchmarking across 44 leading retailers across the globe with a subset of the data including outlet counts, facility characteristics, brand and volume performance and the client could compare performance across these factors against retailers from the US, Japan and Malaysia. The outlet share position was plotted for each of the retailers in the study as compared to the optimal outlet position, defined as the point beyond which the retailer would start cannibalising its own network and the client discovered that it was cannibalising its network at a greater rate than the other retailers and opportunities were highlighted for financial improvement for the retail network.

The group makes the majority of its revenue in North America and one European client makes up 9% of sales which would clearly be a loss if they were to disappear. The group does also seem to have quite a lot of receivables that are overdue, with £2.8M this year compared to £1.1M last year, although apparently they relate to a number of independent blue chip customers. There is also some sensitivity to exchange rate changes with a 10% change in the US Dollar against the Euro would impact the result to the tune of $199K. The group is susceptible to an economic downturn which may have an adverse effect on the demand for their services.

At the IPO Neville Davis was appointed as non-executive director. He has a background in general management and finance within the technology sector with experience working with growing technology companies looking to achieve growth via both organic and acquisitive means. Since then the board has been further strengthened by the appointment of Nick Habgood. He is a founder of Azini Capital, a private equity firm that is one of Kalibrate’s major shareholders.

Going forward, with the cautiously improving global economic outlook, the board are going into the new year with confidence that they will be able to deliver against their objectives in the year ahead.

The shares currently trade on a hefty underlying P/E of 23.8 but this reduces to a more sensible 17.1 on N+1 Singer’s forecast for next year. There are currently no dividends being paid or forecasted. Net cash at the year-end stood at $9.6M compared to a net debt position of $500K at the end point of last year, mostly due to the equity fundraising at the time of the IPO.

Overall this is a mixed start to listed life for the company. Profits were down but when the IPO costs and last year’s tax credit was removed, they were broadly flat. Net assets improved due to the equity issue to give a decent looking balance sheet and operational cash flow improved, although looking closer this seems to be a result of favourable working capital movements, to give a free cash flow of nearly $1M. This is an interesting niche and there are certainly opportunities for the company to grow with deregulation in more countries (most recently Malaysia and Morocco) giving scope for geographical expansion and the ability to cross sell their services to existing clients also offering a route to growth. In conclusion then, I do like this company but might wait to see how they bed in to life as a listed entity.