GVC has now released its preliminary results for the year ending 2014.

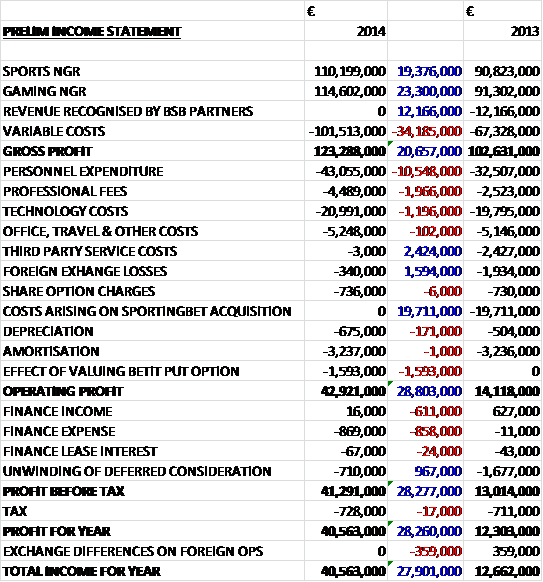

Revenues increased considerably when compared to last year with a €19.4M increase in sports revenues and a €23.3M growth in gaming revenue with increases seen in both Europe and Latin America, and with an increase in variable costs the gross profit was some €20.7M above that of last year. We then see a €10.5M increase in personnel expenditure, mostly due to a €7.3M increase in incentive schemes, a €2M growth in professional fees and a €1.2M increase in technology costs, somewhat offset by a €2.4M reduction in third party service costs and a €1.6M decline in foreign exchange losses. We then see the lack of the €19.7M of costs relating to the Sportingbet acquisition that occurred last year and a €1.6M charge relating to the effect of valuing the Betit put option. Finance income fell considerably which was exacerbated by an even larger increase in finance expenses due to the retranslation of the Sterling denominated William Hill loan, offset by a decline in the unwinding of deferred consideration which meant that after a tax charge broadly flat on last year, the profit for the year was €40.6M, a €28.3M increase when compared to last year.

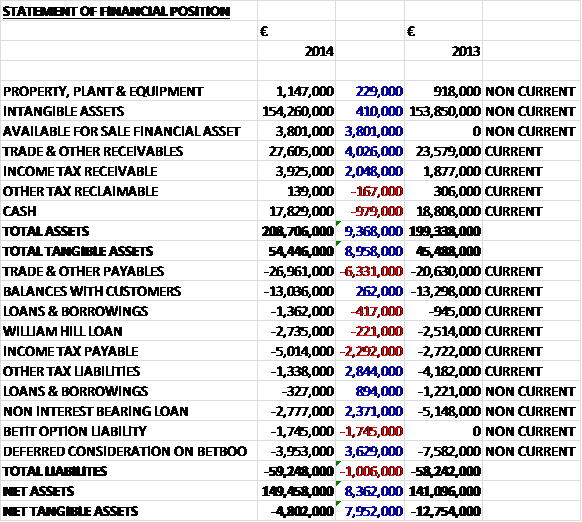

When compared to the end point of last year, total assets increased by €9.4M driven by a €4M increase in receivables, a €3.8M growth in the value of available for sale financial asset relating to the Betit investments and a €2M growth in tax assets, partially offset by a €979K fall in cash levels. Liabilities also increased during the year as a €6.3M increase in payables a €2.3M growth in income tax payable and a €1.7M relating to the Betit option liability was partially offset by a €3.7M fall in deferred consideration on the Betboo acquisition, a €2.8M decline in other tax liabilities and a €2.4M fall in the William Hill loan which meant that net tangible assets were some €8M ahead of last year at a negative €4.8M which seems like a decent improvement.

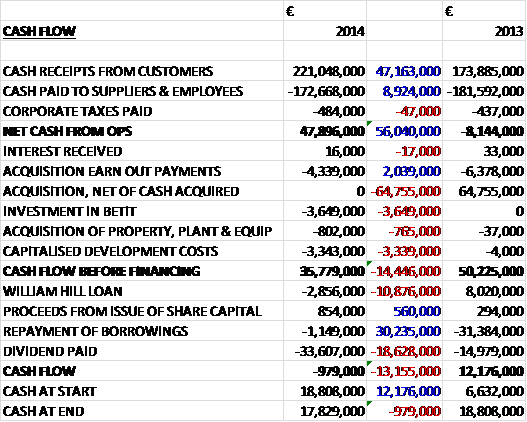

There was an increase in cash receipts from customers and a fall in cash paid to suppliers and employees so that net cash from operations showed a €56M positive swing when compared to last year at €47.9M. Of this, €4.3M was spent on the previous acquisition deferred consideration, €3.6M on the investment in Betit and €3.3M on capitalised development costs to give an impressive free cash flow of €35.8M. The group then paid back some of the William Hill loan and some other borrowings with the rest of the cash going on dividends to give a cash outflow of €979K for the year and a decent cash pile of €17.8M at the end of the year.

The world cup was a success for the group with excellent trading in Brazil and a step-change in the retention and acquisition of customers beyond the tournament. About €7M was invested in marketing around the tournament and some €3.3M was invested in the group’s products which was capitalised as intangible assets. Mobile is becoming the natural choice for players in many markets and continued investment in mobile is seen as key to future success. In addition, the games offering has been broadened through third party integration and the introduction of in-play products is a significant milestone in unlocking additional organic growth opportunities with in-play representing 71% of Sports Gross Gaming Revenue in Q4. Investment in products during the next year is expected to be some 50% higher than this year in order to maintain the group’s market position and improve revenues.

As usual there are some risks and the new tax regime in the UK has shown what can happen – although the group is not that exposed to the UK market. They are looking to further diversify by targeting acquisitions in regulated markets as a foil to the mostly unregulated markets that they are currently engaged in, although if the right opportunity does come up, further unregulated acquisitions would be considered. The group are also rather susceptible to exchange rate fluctuations, not least because the dividends are paid in Euros which could mean the continuing decline of that currency would have an effect on the pay-out. The charge to operating costs due to the declining Euro this year was €300K with a further loss of €500K on the retranslation of the William Hill loan.

One major investment this year was the acquisition of a 15% stake in Betit holdings, a start-up gaming venture focusing on the Scandinavian market. The group pad €3.6M for this stake and they also have a call option to acquire the balance of the outstanding shares between July and September 2017 for a minimum price of €70M with the actual price being determined by the mix of revenues between regulated and non-regulated markets. Should the group not raise the required financing for the deal, the 15% stake can be acquired by the current owners for a nominal consideration.

Going forward, management reckons the group have never been in a stronger position and they look forward to the new year with confidence. Current trading in Q1 2015 is at record levels with sports wagers averaging €4.6M per day, a sports margin of 8.9% (which is actually somewhat lower than was the case during 2014) and an NGR increasing by 18% to €661K per day, producing another quarter of growth. Over the next year the group aims to improve the product offering, particularly mobile, continue growing all markets where they are active and devote more time to non-dilutive investment and acquisition opportunities.

There are a number of short term potential cash outflows over the next year with €2.4M due to the founders of Betboo and another €1.7M due the year after which should finally put an end to the payments for this acquisition which seem to have been dragging on for quite a while. There is also £2.3M (€2.9M) due on the William Hill loan next year with the final £2.3M payment due the year after. In addition there is €1.4M of finance leases payable next year relating to the purchase of software. These payments are similar to those of this year, however, so I am confident that GVC can handle them and increased investment in the product not withstanding should continue to pay the dividends we have become accustomed to.

At the current share price the shares trade on a P/E ratio of 9.3 which seems pretty cheap for a company like GVC. After a year on year increase of 14% the shares now yield an incredible 9.7% and 14c has now been set as the new quarterly dividend benchmark which suggests a similar yield for the year ahead.

Overall then, this is a good set of results. Underlying profits increases over last year, although personnel costs seem to be increasing quickly; net assets improved relating mainly to the Betit investment although net tangible assets remain negative (not really a problem given the industry and the cash generative nature of the business). The operational cash flow improved and there was a strong free cash flow which nearly fully covered the dividend and debt repayments with a big cash pile left despite the slight cash outflow. Next year, investment is increasing in the group’s product with a focus on mobile and in-play offerings which is likely to represent a cost of about €3M extra.

The risks remain, the group is reliant on certain unregulated markets with Turkey being a particular concern, hence the focus on a regulated market acquisition and the collapsing euro is causing a bit of a headache – not just for translation but also with regards to the dividends paid in euros and converted to Sterling and the GBP denominated William Hill loan which gets more expensive as the Euro declines. Trading in Q1, however, was at record levels, although it would be worth keeping an eye on the declining sports margin as to whether this is a one-off or not but with a very cheap valuation and incredible covered dividend, I am happy to continue holding here.

After a long bull run the share price has been consolidating since the end of last year and these latest results have done little to change that. The chart doesn’t look great actually but I will remain a holder.

The annual report is now out that adds a bit of meat to the bones of the prelim announcement, particularly with regards to the balance sheet, so here it is:

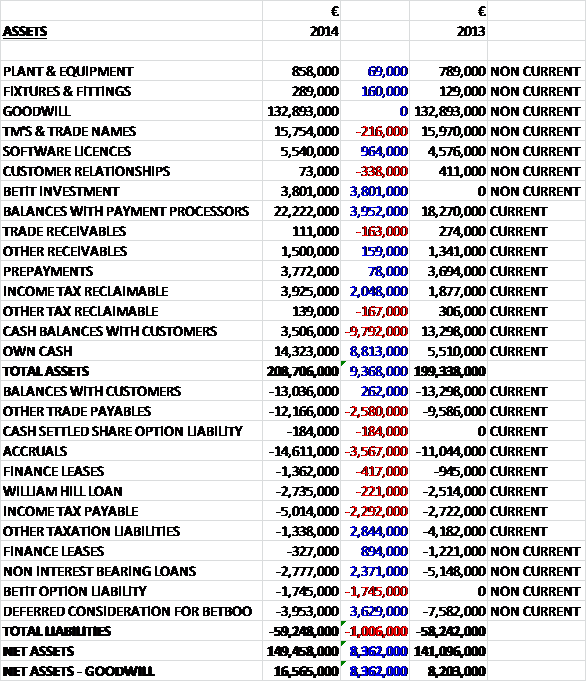

Total assets increased by £9.4M when compared to last year and we can see that this is driven by a €4M increase in balances with payment processors, a €3.8M increase in the Betit investment, a €2M growth in income tax reclaimable and an €8.8 increase in the group’s own cash, offset by a €9.8M fall in cash balances with customers. Total liabilities also increased when compared to last year as accruals grew by €3.6M, other trade payables were up €2.6M, income tax payable increased by €2.3M and the Betit option liability grew by €1.7M, partially offset by a €3.6M fall in the Betboo deferred consideration, a €2.8M decline in other tax liabilities and a €2.4M fall the William Hill loan. I reckon some of those intangible assets are worth something so I have just taken off goodwill from net assets to give a figure of €16.6M, a decent increase of €8.4M when compared to 2013. There are also just over €3M worth of operating lease liabilities not on the balance sheet but this is not too concerning.

There is further clarification of the effect of the weakening Euro with the retranslation of that William Hill loan costing €467K and the retranslation of finance leases costing €160K. I have also re-calculated the current rolling dividend yield using a combination of the exchange rates the company actually used and the current exchange rate for the most recently announced one and this reduces the yield down to 9.2% which is still pretty spectacular.

Another thing that comes to light from the annual report is the huge amount of share options given to the directors. At the end of the year there were 6,806,947 options outstanding. Of these 3,356,947 are exercisable now at a price between 154p and 234p and as a reminder the current share price is about 460p and the value for the directors of these options comes out at a staggering £9.2M! I am not sure why they have not been exercised but a clue to this might come from the 3,450,000 options with an exercise price of 1p that are exercisable if the share price were to stay above £6 for 90 continuous days so perhaps the directors felt the extra dilution would put this in jeopardy. To put it into context, these new options are worth nearly £15.9M which, even when split three ways seems excessive with the total emolument for the CEO being €4.4M during the year and for the non-executive chairman it was €1.5M as each director will receives 100% of their base salary as a bonus if the dividends exceed 54.99c during the year (which was achieved this time).

Just after the year end, non-executive director Nigel Blythe-Tinker stepped down from the board. There is not really a huge amount more to add – the balance sheet looks a bit better now that I can see some of those intangible assets are probably quite value trademarks and such like but the hugely rewarding pay for the directors is a concern as it seems rather excessive to me. It doesn’t stop this company being a strong hold for me though.

On the 24th March it was reported that the CEO purchased 21,740 shares at a cost of nearly £100K which brings his interest up to 415,073 and 0.65% of the company. Although he can clearly afford it, it is good to see him putting some of his own money in. Similarly it was also announced that the CFO also purchased shares – in his case 10,000 at a value of nearly £46K.

On the 25th March the Chairman made it three directors as he purchased 12,500 shares at a value of £57,375 to give him a total of 135,075 and 0.2% of the company.

On the 27th March it was announced that the directors were surrendering up all those share options apart from the ones with an exercise price of 1p. Actually, they were not really surrendered as they will receive in cash the difference between the current share price and the exercise price of the shares. This will net the directors almost £9M in cash quarterly over the next two years which is a huge amount of money and will be material to the cash flow of the company. Not only this but the directors will continue to receive a cash payment equal to the dividend attached to the surrendered options every time the dividends are paid over the next two years. This is quite incredible and I am sorry to say seems very greedy to me. They are no doubt talented individuals but these payments seem far too high for a company the size of GVC.

On the 2nd April the group announced that Marathon Asset Management had purchased 81,577 shares at a value of about £81,577. They now own more than 5% of the total shares in the company.

On the 2nd April it was announced that Prudential had purchased shares to take its holding up to 2,325,000 or 3.79% of the equity. Before this announcement, PRU had less than 3% of the company equity so it is good to see such a well regarded institutional share holder join the list.

On the 5th May the group released a trading update covering the first 120 days of the year. NGR averaged €658K per day, an increase of 17.5% on the same period of 2014 on a sports margin that fell from 9.62% to 8.75%. Sports wagers continued to grow, increasing by over 21% to €4,590K per day. Despite the lower sports margin as a result of punter friendly results so far this year, the board continues to be confident for the rest of the year.

On the 19th May the group announced that it had submitted a bid for Bwin.party digital entertainment which would be finance jointly by GVC and Toronto based Amaya.

On the 8th July the group released a statement covering trading in the first half of the year. Sports wagers increased by 19% to €823M although the aggregate sports margin fell from 9.9% to 8.9% due to some “punter friendly” results in the period. This gives rise to an NGR of €120M, a 14% increase on the same period last year but broadly flat when compared to the second half of last year. In Q2, sports wagers reached €412.3M with total NGR up nearly 10% year on year to €661K per day.

The group has a presence in the Greek market via its partner, Centric Multimedia. Following the recent imposition of capital controls by the government restricting the movement of funds both within and outside the country, the group has noticed a softening in plater activity. It is currently too early to forecast whether this will have a material effect on the second half results. The group have declared a quarterly dividend of 14c per share which is slightly lower than the 15.5c declared last quarter but year to date the dividend remains 5% above that of last year.

A brief statement has also been made regarding the proposed acquisition of bwin.party but all that was said is that bwin are determined to work with GVC so that they can finalise their offer over the coming days so it looks like that might be likely to go ahead.

The trading results are decent enough but somewhat flat on the second half of last year and the Greek situation looks as though it might have an adverse effect. Additionally the continued weakness of the Euro is whittling away at the value of the dividend payment. The potential acquisition looks exciting though and I am happy to hold on and collect those dividends until that plays itself out.

On the 27th February the group gave an update on the potential acquisition of Bwin under which Bwin shareholders would receive 122.5p for each share consisting of up to 25p in cash with the balance in GVC shares. The proposal would be financed via a combination of the issuance of new shares to Bwin shareholders and a €400M secured loan provided by Cerberus Capital. In addition, the company intends to raise about £150M through an equity placing of new GVC shares in order to fund restructuring costs, the refinancing of existing Bwin debt and for additional working capital purposes. If a transaction were to be completed, the board believe that cost reductions exceeding €135M per annum would be achieved by the end of 2017.

So the saga rumbles on, the Bwin board seem to prefer 888 as an acquirer but GVC may succeed with this revised bid. It seems like there will be some heavy dilution and a lot of debt if this bid succeeds, although the mooted cost benefits may justify the expense.