![]()

Sainsbury have now released their final results.

Revenues for the year were up by just over £1B at £23.3B, £1B of which were online sales, up by 20%. An increase in cost of sales, employee costs and operating lease payments, however, mean that the Gross profit is just £66M up on last year. There was a £20M Transaction cost related to the on-going purchase of Sainsbury Bank that did not occur last year, £5M of internal restructuring costs and a £26M increase in other admin expenses, which, when combined with the £15M less in profit from the sale of subsidiaries meant that operating profit was only £13M up on last year.

The profit for the year was £16M up on last year at £614M as a pension financing charge was counteracted by a lower tax charge. Total income for the year was £90M lower than last year at £361M as the group was severely affected by a £366M actuarial loss on the pension scheme. Overall this is not a bad result, but the profit does not seem to have moved on that much from last year and the pension valuation is becoming a bit of a worry.

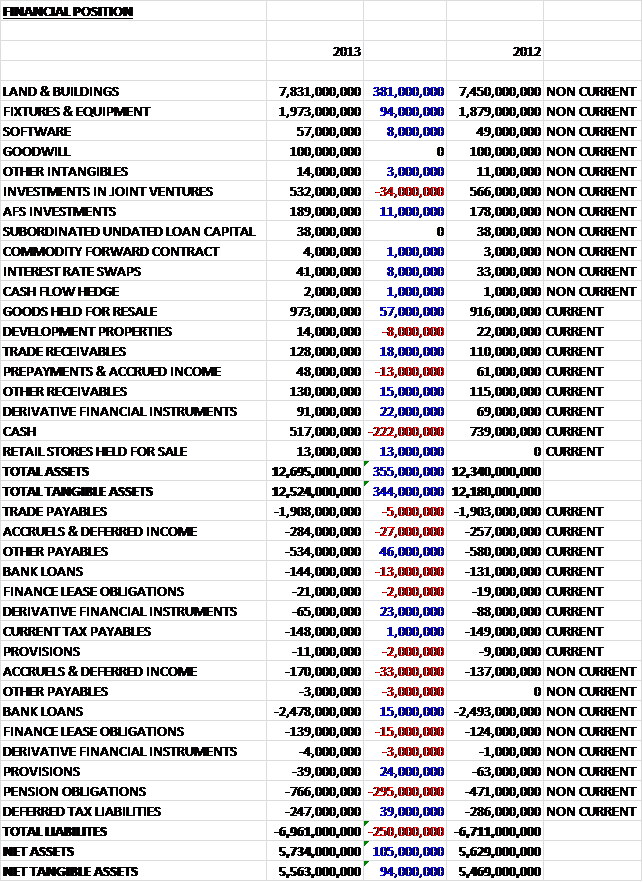

Total Assets for the year increased by £355M. The largest increase was the value of land and buildings, up £381M on last year, followed by fixtures and equipment (up £94M), showing that Sainsbury is continuing to invest in its store portfolio. Another major increase was the value of inventories, again showing the larger store portfolio. This was somewhat mitigated by a £34M reduction in joint venture values, reflecting a revaluation of some of the property held in joint ventures, and a £222M reduction in cash levels.

As far as liabilities were concerned, the largest increase by far was the £295M hike in pension obligations, followed by a £60M increase in accruals and deferred income, which partly relates to the accounting for leases with fixed rental increases. The increase was lower than that of assets, however, so net tangible assets increased by £94M to £5.563B.

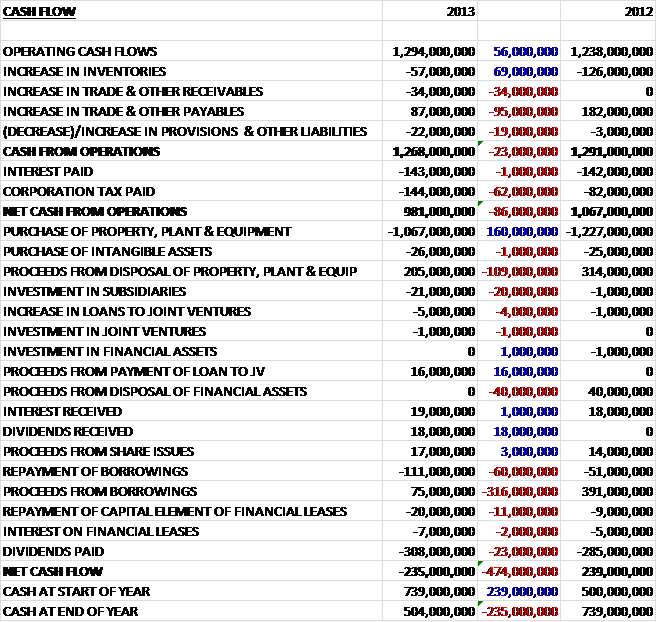

Compared to last year, cash from operations fell by £23M due to an increase in trade and receivables and less of an increase in payables. The net cash from operations of £981M was further affected by a £144M corporation tax charge (£62M higher). All of this cash was then swallowed up by £1.067B of capital expenditure, leaving a negative cash flow after this. This was made worse by a £21M investment in subsidiaries and a net £36M repayment of borrowings (compared to a net £376M receipt from borrowings last year). Dividends of £308M were also paid out during the year. The group did benefit from an £18M dividend received, however. Overall then, the group had a net cash outflow of £235M, compared to an inflow of £239M in 2012. When it is considered that there was a £412M swing in loans going out, the resulting difference from last year is -£62M, which seems to have been accounted for by a £109M reduction in proceeds from the sale and leaseback of stores.

Profits from the bank were just £2M, affected by the £20M of costs relating to the purchase of the 50% held by Lloyds. The property investments also only contributed £2M due to a reduction in the value of the properties. This compares to £16M and £12M respectively last year. To put these numbers into context, the retail stores earned £784M in profit. Without the one-off costs, the bank at least would have increased profits.

The group intends to take full ownership of the bank and therefore have signed an agreement to buy the 50% owned by Lloyds at the cost of £248M, £193M of which will be a cash payment. They see the full control of the bank as an important part of their diversification strategy. The group have also opened up pharmacies in 270 stores and the energy business has seen an 83% increase in customers – I cannot see where the energy business’ results are listed though so I do not know how much was made on energy. Clothing also showed strong growth, showing a strong double digit increase. In addition, the group has a GP office in 35 stores and a dental surgery in 12.

Convenience stores is another area that Sainsbury have been aggressively expanding into during the last few years and sales this year were up by 17% driven by new openings and some like for like increases. Online is another growth area, up by 20%. Growth in credit cards was 17% as the bank’s card is strengthened by the offer of Nectar points. Other areas of growth within the bank were insurance, with business up 67% and travel money, up 35%. During the year, Sainsbury purchased a majority stake in Anobii, which now operates as Sainsbury e-books and signed a deal with Rovi to supply an on demand video streaming service.

One area that Sainsbury has traditionally done well is on special occasions such as Christmas and Easter. This year, the UK had many such occasions with the Olympics and Jubilee celebrations. Homeware in particular was boosted by this effect. The group continue to open new space, with 14 new supermarkets and 87 new convenience stores being opened during the year. Sainsbury continues to trade on its values as a commercial advantage and Sainsbury is once again the largest fair trade retailer in the world. Sainsbury continues to have a successful own brand and it grew 5% on last year and now accounts for half of all food sales. The premium brand fared particularly well, with sales up 10%. It is here that Sainsbury’s reputation as a reliable and honest provider really pays dividends as it emerged completely unscathed from the horsemeat scandal that hit other supermarkets.

In order to plug the gap in the pension scheme, the group transferred £501M of property in 2011 to a partnership via a sale and leaseback program. The pension scheme’s interest in the partnership nets it about £35M a year over 20 years and in 2030, the property will revert back to Sainsbury ownership for a cash payment equal to the remaining funding deficit, up to a value of £600M. This is either quite an elegant solution to the funding issue or a ticking time bomb, I can’t quite work out which. Currently the net pension obligations stand at £688M, up by £233M on last year and the pension deficit is a bit of a concern going forwards.

Net debt at the end of the year was £2.2M, up by £182M over that of last year. At the end of next year, the group expect net debt to hit £2.6B as capital expenditure continues to outstrip the cash received by the group. The cash outflow is a little disappointing but underlying cash flow was actually better than last year. Profit for the year was up marginally, as were net tangible assets as a reduction in cash and higher pension obligations were counteracted by a greater investment in property. Going forward, there is a commitment of £248M to purchase the half of the bank that the group do not currently own. Clearly there is an element of risk here but it is an interesting diversification for Sainsbury to attempt. There is going to be £100M of capital injection over three years to maintain the appropriate ratios, mitigated by a £60M repayment of dated loan stock. In addition, the bank will also incur non-underlying transition revenue costs of £170M and transition capital expenditure of £90M, in order to build and move onto the new banking system so this is starting to look a bit expensive. Having said that, the group have indicated that the transaction is expected to deliver cash payback within eight years. Operations wise, the big growth areas were the convenience stores and online sales.

Overall then, not that much progress has been made, and it does concern me a bit that the capital expenditure is higher than the cash received, which in the long term it would be good to get under control. Having said that, it has been a difficult market over the last year and Sainsbury seems to be faring better than other UK supermarket groups. The dividend is currently 4.7% and covered 1.8 times by earnings, which the board aim to increase to two times earnings. The P/E ratio is a rather good value 11.4 which looks pretty good to me and I think that the shares may be slightly undervalued at the moment. I may look to buy more on weakness.

Sainsbury have now released their first quarter trading update. It seems to contain more of the same really. Like for like sales are up 0.7%, with total sales up 3.6% driven by homeware, with kitchen electrical sales up 34% and cookware up 23%; convenience stores with sales up 20% (19 news stores have been opened) and online sales, up 16%. I do not consider anything to have materially changed since the last update.

On 2nd October, Sainsbury released an update covering the second quarter. Overall, total sales were up 5% and like for like sales up 2.1%. For the first half of the year, sales were up 4.4%. During the quarter the big drivers were online sales, up 15% and convenience sales, up 20%. General merchandise also continued to grow and the rate was over twice that of food. During the period, the group launched a new mobile service in a joint venture with Vodafone so it will be interesting to see how that gets on. As far as traditional stores were concerned, there were 31 new convenience stores opened and 5 new supermarkets. Overall this is yet another strong result, and it is business as usual for Sainsbury.