International Greetings has now released its final results for the year ending 2015. These took me by surprise somewhat, as I wasn’t expecting them so soon!

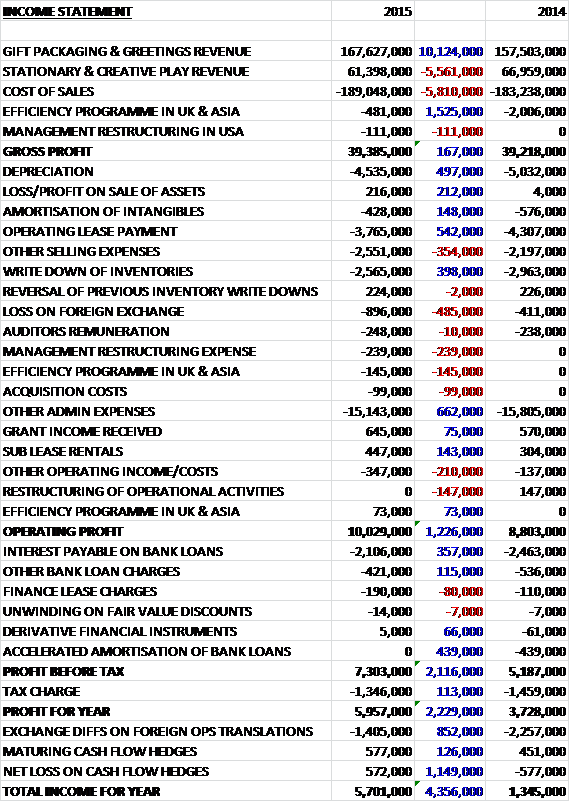

Revenues increased this year when compared to 2014 as a £10.1M growth in gift packaging and greetings was only partially offset by the £5.6M decline in stationary and creative play sales. Cost of sales also increased but far less was spent on the UK efficiency programme, which this year related to the investment in high definition printing in Wales, to give a gross profit just £167K ahead. As far as selling expenses are concerned, we see a near £500K fall in depreciation and a similar decline in operating lease payments and in other expenses we also see a £398K decline in the write down of inventories. In addition, the forex loss doubled to £900K and there were some other one off costs such as the management restructuring expense after the US CEO sadly passed away along with the admin costs for the efficiency programme. In all, this gave rise to an operating profit £1.2M above that of last year.

Operating costs fell during the year as better bank terms and lower debt reduced the interest payable and there was no one-off accelerated amortisation of bank loans that occurred last year. The tax charge was also £113K lower so that the profit for the year stood at £6M, an increase of £2.2M year on year.

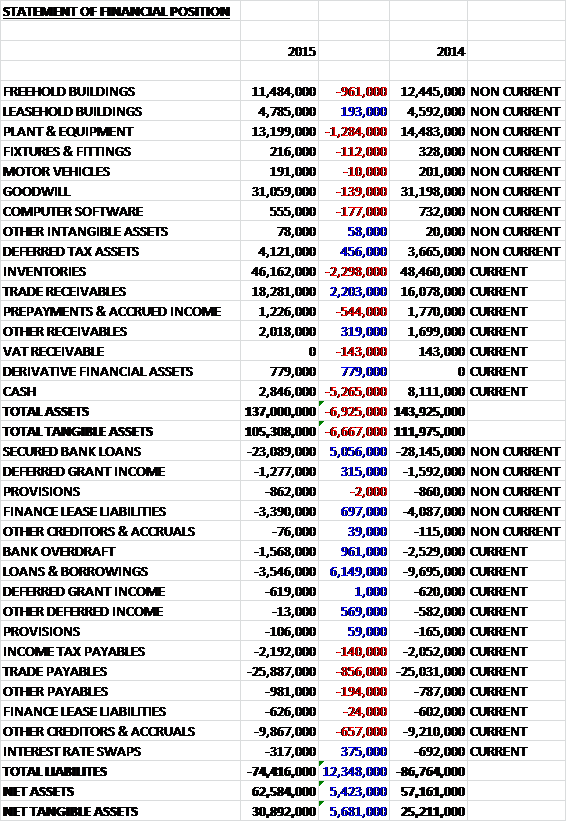

When compared to the end point of last year, total assets fell by £6.9M driven by a £5.3M fall in cash, a £2.3M decline in inventories and a £1.3M decrease in the value of plant and equipment, partially offset by a £2.2M increase in trade receivables. Liabilities also fell during the year due to a £6.1M decline in current loans and borrowings, a £5.1M fall in secured long term bank loans and a £961K decline in the bank overdraft. The end result is a £5.7M increase in net tangible assets to £30.9M which seems quite a good result. There are currently £22.7M worth of operating leases outstanding which seems to be fairly well covered.

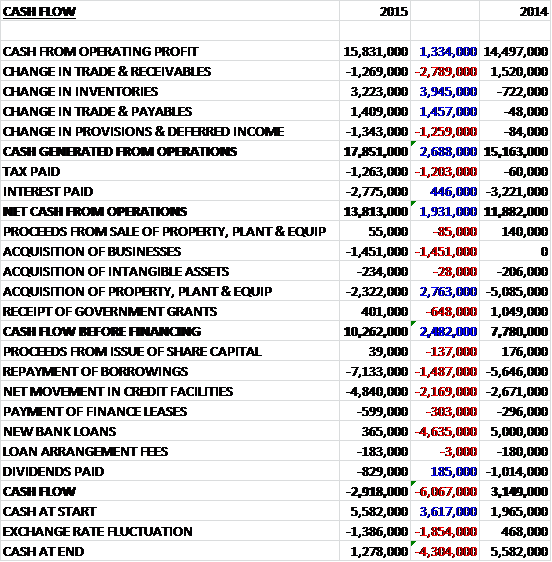

Before movements in working capital, cash profits increased by £1.3M to £15.8M. After changes in receivables and payables broadly cancelled each other out, a fall in inventories, particularly in the US, meant that the cash actually generated from operations increased by £2.7M to £17.9M. We then see less interest paid but much more tax when compared to the negligible amount last year so that net cash from operations stood at £13.8M, an increase of £1.9M year on year. Capital expenditure was lower than last year at £2.3M for property, plant and equipment so even after the £1.5M spent on acquisitions and £648K less in government grants, free cash flow increased by an impressive £2.5M to £10.3M. This, along with some of the cash from last year, enabled the group to pay back £11.6M of borrowings to give a cash outflow for the year of just under £3M and a cash pile at the year end of £1.3M. Despite the low amount of cash to end the year, this is exactly what I like to see – a company using its free cash to pay back loans.

Profits at the UK and Asia business were £4.5M, an increase of £2.8M year on year. During the year the group upgraded compliance standards in their facilities in China which led to the record sales of 74 million Christmas crackers. They are now geared for even greater performance levels having invested in semi-automated processes for cracker manufacturing which became operational during spring 2014 along with enhanced production capability in gift bags and greeting cards. These upgraded facilities have enabled them to secure a three year contract for the sole supply of single greeting cards to the UK’s largest pound shop and record levels of gift bag orders that have been achieved for shipment during 2015.

The group will continue to grow sales of licensed products with stationary and creative play categories being consolidated under the Copywrite brand in the UK. Sales of the Disney Frozen and Despicable Me ranges were noteworthy and continued to thrive into the new year alongside an updated selection of other licensed products.

The European business had a profit of £3.2M, a growth of £600K when compared to 2013. This growth occurred despite challenging overall market conditions due to excellent levels of manufacturing efficiency and record sales volumes. The second full year of using the new printing facilities in Holland, along with highly competitive product offerings resulted in a continued growth of market share. The acquisition of Enper in June has been fully integrated and strengthened market share in the Benelux region and management seem to be on the lookout for similar acquisition opportunities in the future.

The profit at the USA business was £2.1M, a fall of £900K year on year despite strong sales growth which benefited this year from a weak end to 2014 due to the adverse weather conditions that occurred at that time. During the year the gift wrap manufacturing facilities near Savannah were enhanced by the installation of new automated case packing equipment which was fully operational from Spring 2014. During the new year, new, high speed paper conversion facilities will be installed. The sales growth included expansion in the neighbouring markets of Canada, Mexico and South America and in the US growth was achieved within the major supermarket and discount channels. The working capital situation in the US was vastly improved during the year through a 36% reduction in inventory levels.

The Australia business had a profit of £1.1M, a decline of £1M when compared to last year. Performance was impacted by an overall slowdown in the country’s economy and a recent investment in logistics facilities that enables the group to improve order fulfilment levels to an increasing base of retail customers across the country. The focus for the coming year will be on executing plans to improve profitability rather than trying to increase sales.

In recent years the market the group operates in within the UK has undergone some changes and experienced value and innovation by the traditionally dominant supermarkets, the expanding market presence of discounters, the prolific growth of pound shops and the ever expanding online presence of new and existing customers. In mainland Europe the group plans to continue to leverage its position as the number one European player in gift packaging, working mainly with the major retail chains but also seeking opportunities in new channels and territories across the continent. In the US there has been success through nationally based grocery chains, discounters and $1 retail specialists. At the same time, the well-established gift wrap company range of premium products has consolidated its market position. Further growth opportunities have been established and traction gained in South America and Canada, both through partnerships with US-based customers and through indigenous customers.

In Australia, the closure of one of the country’s largest discount chains impacted the business and the market overall. The strategy has been to seek new channels of distribution offering both FOB and domestic order fulfilment whilst providing customers the full availability of the portfolio of products available from the group as a whole. This has enabled the group to expand their presence to neighbouring countries such as New Zealand. The business has also expanded its upscale activities including premium brands such as Card Couture as well as the full range of Tom Smith crackers, cards and gift packaging. Although from a small base, the group has also experienced growth in other regions such as Asia, Africa and the Middle East.

After the successful investment in Europe and the UK, the group are looking at investing in the US and Australia to improve margins to levels closer to the European business. In general the group also looks to improve on their rather thin 3.7% pre-tax margins by increasing the balance of own brand products and non-Christmas business along with efficiencies in sourcing and manufacturing which should already help improve margins for the next year after the investment in the Swansea manufacturing facilities last year. Another factor that affects margins is the increase of the lower margin FOB business delivered to major customers at ports in China. The group will still target this FOB business as it enables high volume orders and avoids other costs and risks associated with domestic delivery.

The group is somewhat susceptible to exchange rate changes and a 10% strengthening of Sterling against the Euro and US dollar would reduce profit by £25K and £617K respectively so the GBP/USD is definitely the one to keep an eye on. It has been stated, though, that the significantly weaker Euro rates at the end of the year are likely to impact more materially in next year’s results through translation of overseas earnings. Additionally, the relative strength of the US Dollar can materially impact prices out of China, most notably due to the weakness in the Euro and Australian dollar which will reduce margins on products out of Asia to those regions.

On the 5th June 2015 the group acquired Enper Giftwrap for a cash consideration of £1.5M which generated goodwill of £509K. Had the purchase taken place at the start of the year, turnover would have been £229.5M. Now that the investment in Wales is complete, the site at Aberbargoed may become available for sale which offers the opportunity to release cash in the near future and in addition the group is in the third year of a five year period by which a company has the option to purchase part of another under utilised site for a price of £2.4M (the book value is just £800K)

Going forward, management expects that now they have improved their financial position and management team, opportunities exist to grow in all regions, both organically and through acquisitions.

At the year end, net debt stood at £29.4M compared to £36.9M at the end of last year. At the current share price, the shares trade on a P/E ratio 12.9 and yield 0.8%, improving to 11.1 and 1.6% respectively on next year’s forecast after they returned to the dividend list a year ahead of schedule. Going forward, the board has determined that the dividend will be covered at least three times by underlying earnings and the board will target this level going forward, although this will be balanced against attractive opportunities to invest in growth that present themselves and the continued reduction in debt.

Overall then, this was a year of real progress for the group. Profits and net assets both increased and the operational cash flow also improved, aided by tighter US stock control. The group is giving off good levels of free cash even after the acquisition which is being used to pay down debt at a decent rate. The UK, Asia and Europe is performing well after their manufacturing facilities were upgraded last year but times were harder in the US and Australia with the latter being impacted by the closure of a large discount store. The group is looking to invest in the US production facilities going forward to improve efficiency there. Although lower margin, the licensed products of Disney Frozen and Universal’s Despicable Me should provide decent sales and there should be continued improvements filtering down after the investment in Wales, not just operationally but also through cash realised by the potential sale of one of their sites.

The forward P/E looks pretty undemanding, the net debt is coming down nicely and the dividend is nice to have, although at the moment it is not particularly material. The board have flagged up continued Sterling strength as a very real headwind, however, so I shouldn’t get too euphoric over the potential here. Nonetheless, I am comfortable with my current investment here.

the share price had already moved up in anticipation of these improved results so there could be a period of consolidation on the cards.

On the same date, the group announced that CFO Anthony Lawrinson exercised share options over 607,652 shares with an exercise price of nil. Following this, he then sold his entire 667.652 holding realising some £817K!. I have to say this is disappointing on a number of counts. I do think that this number of options with an exercise price of zero is excessive and a bit greedy. In addition, the fact that the CFO now own no shares in the company is also a bit of a disappointment in my view.

On the 1st August it was announced that Chairman John Charlton (through his wife) had sold 10,000 shares at a value of £14.6K. Given that he now owns 667,500 shares, this is not a massive sale by any stretch of the imagination but following the CFO sale previously, this is not a great indication of strength going forward.

On the 26th August the group released a trading update covering Q1. Sales and overall customer order levels already received have been in line with management expectations and the board believe they are on track to deliver against market expectations despite the weak Euro and AUS dollar. In the US, the group has begun a phased programme of investment in the manufacturing facility starting with new high speed gift wrap converting equipment to be installed in early 2016. Also in the region they have extended their relationship with Aldi to the US where they have over 1,000 established stores; they have received a Christmas commitment from one of the largest drugstore chains to feature in over 7,500 stores and they have commenced trading with a chain of over 8,000 discount stores where a range of creative plat products will be launched in Autumn.

There was also some good looking licensing highlights as the group entered into a contract with Disney for the Star Wars franchise on a multi-territory basis; they entered into a licensing contract with Coca Cola, featuring Santa Claus across a range of gift packaging and greetings products in the UK; they have received commitments for over 2 million of creative play products in the UK for Universal Studio’s Minions; and the latest National Geographic product offering across gift packaging, gifting and stationary will be promoted in over 3,000 additional stores.

This all sounds fairly promising. I took some profits in these shares after they quickly increased in value and the directors started selling but I am tempted to jump back in actually.

On the 7th September the group announced that Chairman John Charlton had sold 10,000 more shares at a value of £15K. This is not much and he still owns 657,000 shares but I am not too happy about the continued investor selling here.

On the 20th October the group released a trading update covering the first half of the year. Overall trading was in line with expectations with decent sales revenue and a solid order book supporting the expectations for the full year. In the UK, the group are on track to deliver the expected annual efficiencies resulting from recent investment in the manufacturing operations; in Europe and Australia the businesses have fought weak Euro and Aussie Dollar exchange rates to deliver to expectations and in US, shipping is ahead of seasonal trends (whatever that means). Additionally, net debt should be significantly lower than at the same period of last year. This all seems decent enough, I am happy to hold.