Telecom Plus has now released its final results for the year ending 2015.

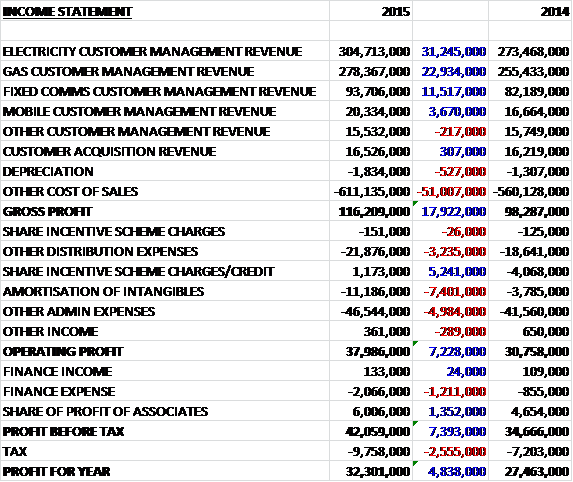

Revenue increased considerably when compared to last year with a £31.2M growth in electricity, a £22.9M increase in gas, an £11.5M growth in fixed communications and a £3.7M increase in mobile. Cost of sales also increased, of course, to give a gross profit some £17.9M ahead of last year. We then see distribution costs increase by £3.2M reflecting higher commissions paid to partners, a £7.4M increase in amortisation of intangibles due to the agreement with N Power kicking in and a £5M increase in other admin expenses (mainly relating to increased staff costs), partially offset by a credit relating to the share incentive scheme which arose as a result of the falling share price. Finance expenses increased by some £1.2M during the year due to the higher loans but there was a £1.4M increase in the share of profit from the associate before a higher tax bill meant that the profit for the year came in at £32.3M, an increase of £4.8M year on year.

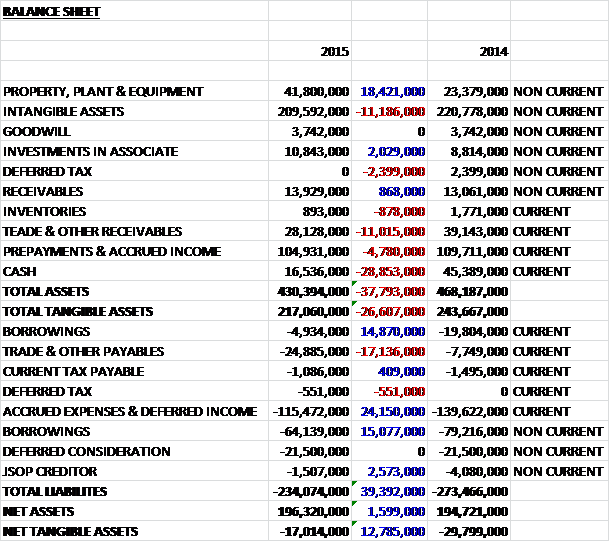

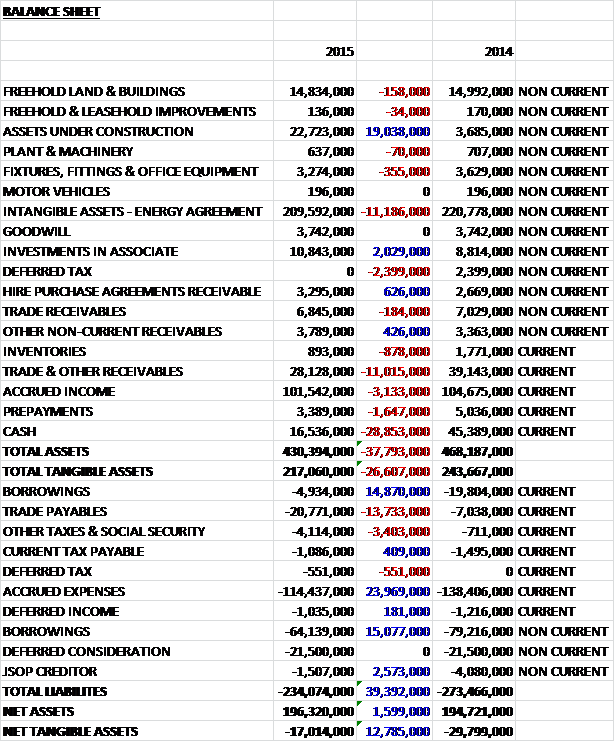

When compared to the end point of last year, total assets fell by £37.8M, driven by a £28.9M fall in cash, an £11.2M decline in intangible assets, an £11M fall in receivables, a £4.8M decrease in prepayments and accrued income, and a £2.4M fall in deferred tax, partially offset by an £18.4M increase in property, plant & equipment and a £2M growth in the investment in an associate. Liabilities also fell during the year as a £24.2M fall in accrued expenses & deferred income, a £30M decline in borrowings and a £2.6M decrease in the JSOP creditor was partially offset by a £17.1M increase in payables. Overall, net tangible assets increased by £12.8M but they remained negative, at -£17M.

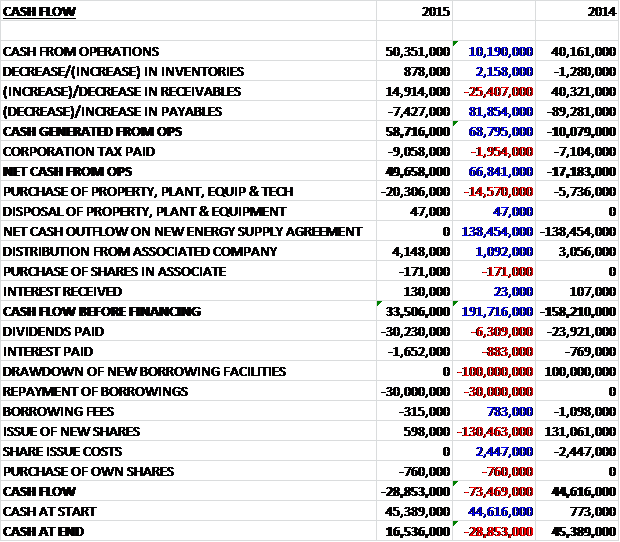

Before movements in working capital, cash profits increased by £10.2M to £50.4M. This increased further due to a decline in receivables from payment timing differences on the energy purchasing agreement with N Power, a situation that is likely to reverse next year, but a much lower fall in payables meant that the cash generated from operations increased by £66.8M to just under £50M after tax. After the group spent £20.3M on capital expenditure, mostly relating to the refurb of the head office, and received £4.1M from the associate, there was a free cash flow of £33.5M available. This covered the £30M loan repayment but not the £30.2M in dividends so for the year there was a cash outflow of £28.9M to give a cash pile at the year-end of just £16.5M.

Next year the group is expecting a modest rise in working capital requirements due to the costs associated with funding the growth in the mobile business (the provision of premium handsets on 24 month contracts), an increase in the number of Minis provided to partners on hire purchase agreements and the cost of providing partners with tablets on 30 months interest free credit. On the other hand, capital expenditure should reduce as the group finishes refurbishing their new office HQ.

This year has provided the most competitive trading conditions that the board have yet seen where a sustained fall in wholesale energy prices over the last 18 months and aggressive promotional activity by a number of new entrants into the energy market, who have not hedged their energy costs at historically higher prices, has combined to create a record gap between the introductory fixed price deals available to those who switch and the standard variable tariffs paid by the majority of domestic customers. This has been exacerbated by the group’s competitors using the higher margins earned on legacy customers to help fund new introductory deals which is something the group does not do and expects that will be addressed in due course through regulatory intervention and reductions in standard variable tariffs as larger suppliers reflect the prevailing lower level of commodity costs.

Although the group remains on track to achieve their medium term target of one million households, it is now apparent that the path towards this will not be a straight line with growth being higher during periods when market conditions are favourable and slower at times like this when the competitive environment is more challenging.

The profit at the Customer Management segment was £53.5M, an increase of £10.6M when compared to last year. The increased profitability seen reflects organic growth over the past couple of years along with the additional margin contribution from the supply arrangement with N Power, partially offset by the higher costs associated with leakage within the national gas distribution network than had previously been anticipated. Revenue growth was constrained by a fall in average energy consumption from the domestic membership base due to a mild winter and the impact of energy efficiency measures that have been delivered by the industry over the last few years with the average revenue per member falling from £1,304 to £1,279.

The group has delivered some 200,000 more services during the year with growth spread across all services with 58,753 residential members now taking all five services from the group with some 66,898 now taking the “Double Gold” bundle, a 44% increase over the past year. Indeed, the percentage of new members taking the bundle has been steadily increasing from 21% in Q1 to nearly 28% in Q4. During the first two months of Y/E 2016, following the recent changes to the proposition, the percentage has increased to over 29%.

The group continues to do well with regards their customer service having been shortlisted as best telecom service provider at the Moneywise annual awards. As such, the group also does not offer heavily discounted one-year introductory deals to new members, unlike many of their competitors with both new and existing customers paying identical amounts for the same packages. The good customer service has filtered through to a consistently positive net promoter score of +45 in an industry where some suppliers achieve negative scores and British Gas has a score of +23. Indeed, this represents the second highest of more than 60 brands.

The Opus associate continues to go from strength to strength and it is anticipated that the contribution will be about £6M next year too with an increase expected in 2017. The increase reflects the progress that has been made in supplying gas alongside electricity into the small business and corporate sector, for which they are now buying renewable energy from over 500 small UK generators. The investment in the associate is valued at £10.8M on the balance sheet but the board believes the market value is substantially higher and they are very pleased to have exposure to this rapidly growing, profitable and highly cash generative business.

The loss at the Customer Acquisition segment was £15.5M, an increase of £3.3M year on year. This widening loss reflects the increased promotional activity during the year targeted on recruiting high quality multi-utility new members in a highly competitive market, and a higher proportion of members taking the double gold bundle. Although the cost of acquiring an owner-occupier taking the bundle is generally considerably higher than for a tenant taking fewer services, the board believes the return on investment will more than compensate for these increased costs due to the much longer expected lifetime of the customer.

During the year, a significant number of new partners joined the business, increasing the total registered from 44,056 to 49,539. It seems that through an improved online training course and revised incentive structure, a higher proportion of new partners are making a successful start to their career and improving the effectiveness of new partners is a core focus for the business. They have recently been trialling a new approach to classroom training that has shown some encouraging results which will be rolled out across the UK this year.

As far as customer incentives are concerned, the group have discontinued their previous introductory offer of six months free broadband for all members taking gold bundles and replaced it with a two year fixed price energy tariff and choice from a range of new benefits which are only available to owner-occupiers and available to both new and existing members. This decision was driven by the significant difference in churn rates between different segments of the membership base as the group declines to complete for those customers who change providers every year looking for the best rates. This removal of up-front incentives has not made is easier for the partners to sign up new members, however, and the absolute growth in the numbers is currently running below the target run-rate for the year as a whole. It is therefore likely that organic growth will remain in the mid-single digit percentage until the gap between the introductory fixed price energy deals available to new customers and the variable tariffs charged to most households narrows significantly which should apparently start to happen later this summer.

During the year the group paid over £5.4M in cashback to its customers, an increase of £500K. This is a great incentive to provide as it is funded entirely by the retailers in the programme with some members achieving more than 20% off their utility bill just by using their cashback card to make purchases.

One area that there is a tangible sense of frustration from management is that of regulation. They will shortly be starting to roll out the installation of smart meters for their members in order to ensure that all domestic energy meters are replaced by 2020. There have been continued delays in finalising the specification for the meters, however, which suggests that the original target end date for the programme is no longer achievable and trying to maintain this deadline will likely lead to higher fulfilment costs. Another example is the establishment of “Smart Energy GB” which has a mandate to spend over £85M of customers’ money on advertising the benefits of smart meters through an expensive multi-media campaign featuring two cartoon characters called “Gaz” and “Leccy”. I have pretty much quoted that from the annual results and the disdain from the Chairman is almost palpable!

The group is looking at expanding their offering and later this year they hope to introduce a range of insurance products such as home and motor policies. In the longer term, other potential new services include water, TV and home emergency cover, including boiler cover. One service already being supplied that is a potential growth area is mobile. During the year there was a 23% rise in the number of mobile services provided and penetration within members has now reached 25% with scope for further improvement going forward.

One major issue over the past year has been the fact that some £11M on the balance sheet as accrued income was unlikely to be recovered due to higher levels of industry-wide leakage in the gas distribution network than had previously been thought. It has therefore been necessary to write down the unbilled gas debtor to bring its value in line with the amount expected to be receivable. Due to the more sophisticated way that electricity wholesale costs are reconciled to actual customer meter readings, the effect on this market has been limited to £300K. The board has seen fit to restate these numbers in previous balance sheets rather than take the hit as an impairment.

One potential problem facing the group is the agreement set with N Power for the provision of power. The price paid for energy is set by reference to the average of the standard variable tariffs charged by the “big 6” to their domestic customers, less an agreed amount. This is a good strategy at most times but in the current environment, this price may not be competitive against the wholesale prices available to new and other independent suppliers.

Looking forward, the board are confident that they will deliver record revenues, profits and earnings per share next year and expect to increase the dividend by another 15% to 46p (which is the figure used for FinnCap’s estimate below). Management are expecting pre-tax profits to come in at between £54M and £58M – it is nice to see the board sticking their necks out and suggesting a figure actually.

At the current share price the shares trade on an expensive looking 21.9 times earnings, which falls to 14.9 on FinnCap’s forecast for next year which seems about right. After increasing by 14% year on year, the dividend yield currently stands at 4.6%, increasing to 5.2% next year which seems like a very decent return to me. The group is currently in a net debt position of £74M compared to £75.1M which includes a deferred consideration of £21.5M payable to N Power during Y/E 2017.

Overall then, this has been a difficult year for the group but I have to say these results look a little more reassuring than I thought. Profit is up, along with net tangible assets – although the group still have a negative net tangible asset base which is not something I like to see usually. Operational cash flow seems strong, although this was enhanced by favourable working capital movements which will reverse next year. Although the group does have a strong free cash flow generation, this year it was not enough to cover the dividend and the debt repayments – I wonder if something may have to give here, although the lower capital expenditure now the HQ is finished should help.

The main issue this year has been that lower wholesale prices have meant that the group’s earlier agreement with N Power is now a hindrance as smaller, independent providers can buy cheaper wholesale gas on the market. This is exacerbated by the cheap introductory offers by some competitor s and Telecom Plus just can’t compete with this. Hence, why they are targeting owner-occupiers and those taking more services which seems to be a sensible approach in the current climate. The group still has good results for customer service so it seems they are becoming more of a quality outfit than a cheap one.

The energy leakage issues is disappointing but it seems this has now been sorted with better estimates now in place – how it went on for so long, I really have no idea though and points to a lack of rigour somewhere along the line. At the current share price, the P/E ratio looks about right but that dividend yield is starting to look interesting. In the short term, growth is going to be constrained but given the relatively depressed share price, I have decided to take my first small position here.

The chart suggests it may be a bit soon to buy but the price has risen above the 50 day moving average and I am feeling bold!

Telecom Plus has now released its annual report for the year ending 2015.

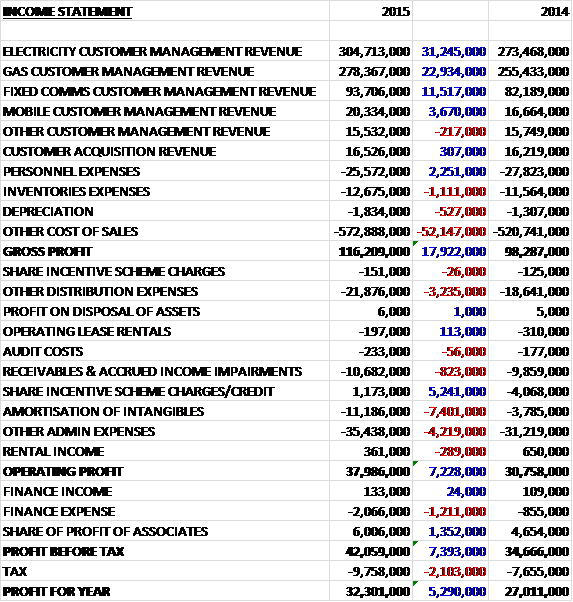

There is not too much here that has now been covered previously but we see that personnel expenses fell by £2.3M, partially offset by a £1.1M increase in inventories expenses. As far as admin costs are concerned, operating lease rentals fell by £113K but receivables and accrued income impairments increased by £823K.

The balance sheet gives a bit more extra information though, as we see that the increase in property plant and equipment is entirely due to the £19M growth in assets under construction which related to refurbishment work on the company’s new HQ which was brought into use after the year end, and that fall in intangible assets is from the amortisation of the energy agreement with N Power as would be expected. On the liabilities side we can see a £13.7M increase in trade receivables which looks a little concerning and also a £3.4M increase in other taxes and social security payable. Accrued expenses did fall by £24M, however.

Including the deferred consideration of £21.5M payable to N Power in December 2016, the net debt position was £74M compared to £75.1M last year. There is negligible operating leases outstanding but there are capital commitments of £2.5M relating to items in respect of the refurbishment of the new HQ, the acquisition of a small office building and the acquisition of the source code of the software underlying the group’s billing system.

We can see from the report that the executive directors are incentivised with regards to adjusted EPS growth, Total Shareholder Return growth and service number growth. It should be noted that CEO Andrew Lindsay had a huge payday with a total remuneration of nearly £2.2M due to LTIP awards. It is difficult to see what he has done to warrant this huge amount.

On the 11th August the group released an AGM statement covering trading so far this year. They confirm that they have continued to trade in line with management expectations since the year-end with further steady mid-single digit growth in the size of their customer base.

Only one of the big 6 suppliers have announced a reduction to their standard variable pricing so far so the board expect that trading conditions will remain challenging until the other major suppliers follow suit, which is expected to happen shortly. The board also welcome the draft findings announced by the CMA with regards to their proposal that standard variable tariffs should be subject to a price–cap in order to protect non-engaged customers who are being over charged by their supplier so that they can use the excel profits to offer attractive short term deals to those who switch.

The important part of the announcement is that they remain on track to meet market expectations for adjusted pre-tax profits of between £54M and £58M in the current year and to deliver a 15% increase in the dividend to 46p per share. So, nothing has changed since the last update but it is always helpful to get some reassurance that there are no additional problems.