Interserve splits its business into four different segments. Support services are the provision of outsourced services to public and private sector clients in the UK and Middle East. Construction is the design, construction and maintenance of buildings and infrastructure in the UK and Middle East. Equipment Services is the design, hire and sale of formwork, falsework and associated equipment. Finally, investments are mainly involved in the maintenance of the group’s PFI framework investments. The most important end user sectors are Commerce, Defence, Infrastructure, Health and Education.

Within support services, the group provides facilities management, where they maintain buildings and estates, providing services to people working/living there. Other services include healthcare, employment services, waste management and training. In the UK a continuing trend towards outsourcing is opening up the market for companies like Interserve. The outsourcing market is substantially less developed outside the UK and the second largest market Interserve is active in is the Middle East. Here they provide building repair, plant maintenance, health & safety training and assurance services to the oil and gas sector. This region is a good opportunity for growth and the group is making some investments in this area.

Within construction, the group provide all technical and commercial aspects of building and engineering services including constructing the buildings, providing services to companies constructing the buildings and interior design and fit-out. Some of the projects abroad include infrastructure, roads, rail, port schemes, power, water and drainage and services internationally also include joinery, steelwork and specialist temporary buildings. In the UK, most of the business is in the public and utilities sectors.

Their Equipment services brand is RMD Kwikform and designs and provides specialised framework, falsework and shoring equipment. The business is most active in the UK, Middle East and Australia but has also opened branches in India, Chile, Panama and Kazakhstan.

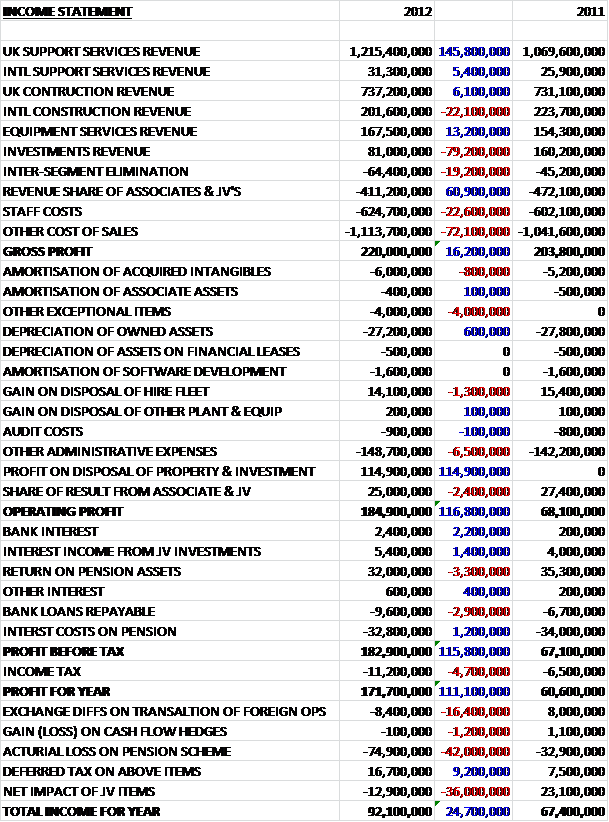

Interserve have released their full year results for the year ending 2012, starting with the income statement.

Revenues for the year were a bit of a mixed bag. The largest revenue source, UK support services, fared well as the group took on more outsourcing work from the government and international support services also did quite well, increasing revenues by over £5M on a small base. Equipment services continued its recovery, increasing revenues by over £13M. Things were not so good for International Construction, however, as revenues from this sector reduced by £22M to £202M as there has been lower demand in some countries. There are some signs of improvement in UAE and Oman with Qatar are also showing some increased infrastructure development. The other sector to fare badly was the investments revenue, which nearly halved to £81M as Interserve sold off a large amount of its PFI investments (the investment in the University college hospital London was sold for £33M to Unicorn Holdings; stakes in two subsidiaries that held 19 PFI investments were sold for £85.5M and the remaining assets held for sale, at a valuation of £51.2M were transferred to the pension scheme). There were also some increases in costs of sales but overall the gross profit was up by £16.2M on last year, at £220M. The £5.4M of interest relating to joint ventures are to do with the PFI assets sold, so this income will not be repeated next year. The group indicate that the income from investing the proceeds will cancel this out. That remains to be seen.

The admin expenses did not change that substantially but the share of profit from associates and joint ventures fell by £2.4M to £25M. The figure dominating these results, however, is the £115M of profit on the sale of investments (the PFI sales mentioned previously). This huge one off receipt caused the operating profit to rocket by £117M to £185M. Without this sale, there would have been a modest increase in operating profit last year. The other exceptional item of £4M relates to bonuses triggered by the profit made on this sale.

Things were otherwise quite stable but the income tax increased by £4.7M on a low level last year which left the profit for the year £111.1M up at £172M. The total income from the year was adversely affected by an actuarial loss on the pension scheme. Overall this profit was totally dominated by the PFI sale, were it not for that, the profit for the year would have been marginally below that of last year.

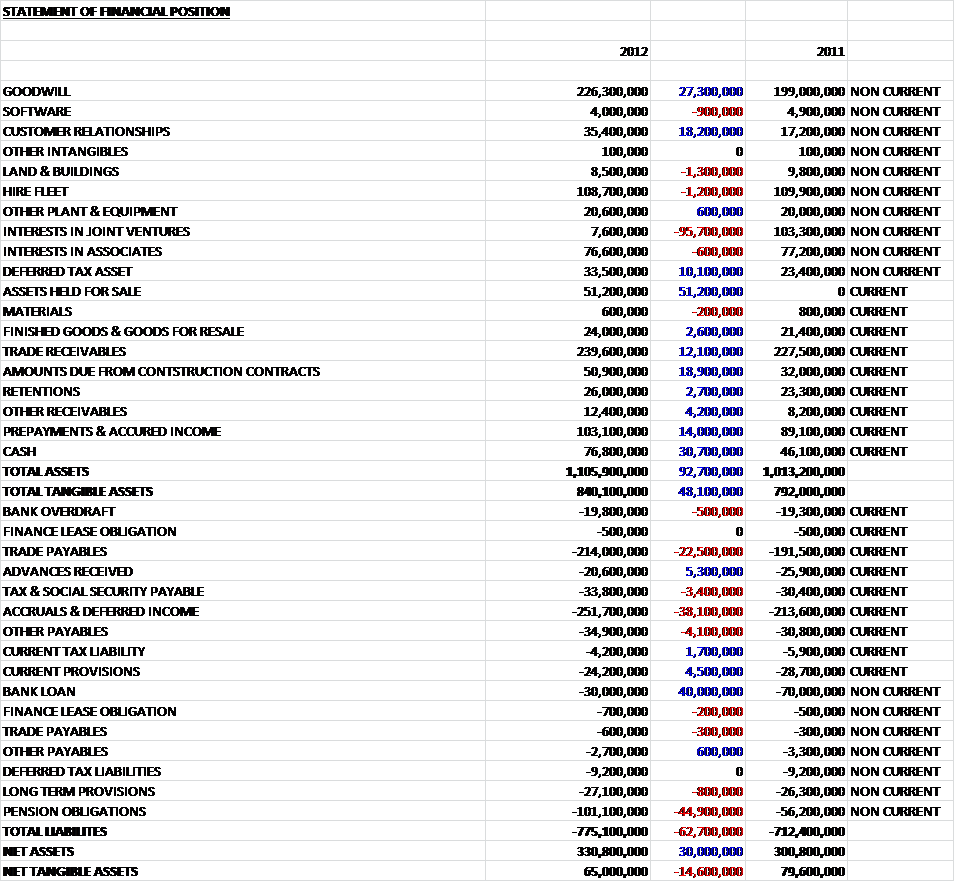

Starting with intangibles – we can see that the acquisitions have come with a substantial amount of goodwill (up by over £27M) and customer relationships. We can see that the investments in joint ventures have been moved to available for sale assets, and in some cases sold (this would be the PFI companies). These sales have given rise to a £31M increase in the cash level. Other large increases in assets include a £10.1M increase in tax assets, a £12.1M jump in trade receivables, a £14M increase in prepayments and a large £19M increase in payments due from construction contracts. All this means that tangible assets were up £48M to £840.1M.

As far as liabilities are concerned, there is a pleasing £40M reduction in the bank loan, to leave it at £30M. Provisions were down by a small amount with the largest proportion taken up by contract provisions, which include the costs of site clearance and other costs. This is where the good news ends, however, as there were large increases in trade payables (£22.5M), deferred income (£38.1M) and pension obligations have increased by a massive £45M to £101M. The actuarial pension scheme deficit was agreed at £150M in the year, before the contribution of the PFI investments being moved to the scheme and future deficit contributions have been set at £12M. That pension obligation increase helped push the group into a lower net tangible asset base than last year and the net tangible assets for this year were down by £14.6M to £65M. This does not seem like a huge amount for a company of this size.

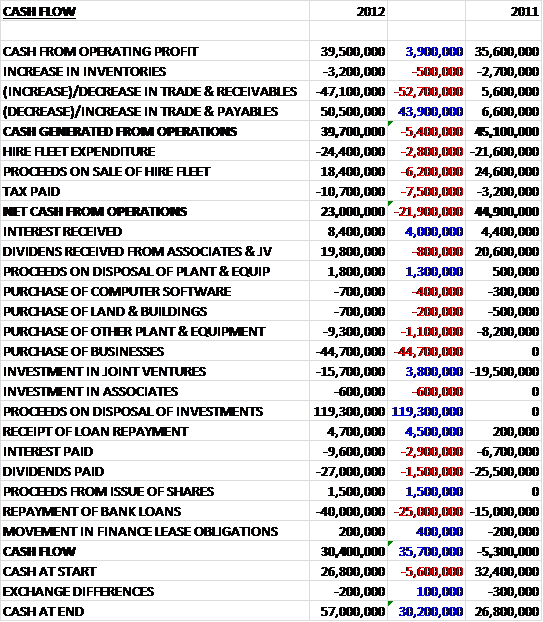

An increase in receivables cancelled out an increase in payables to give a cash flow of operations of £39.7M, which was £5.4M less than last year due to a very big increase in receivables (despite the average credit period on the sale of the goods reducing from 41 days to 37 days). The hire fleet accounted for net £6M of cash and the tax payment of £10.7M was substantially higher than a low level last year which meant that net cash from operations was nearly £20M less than in 2011. The cash receipt from joint ventures was slightly down on last year but was a welcome £20M. The largest income of cash was a one off receipt of £119M from the disposal of a holding in the University College London PFI project and some other PFI investments.

This large cash receipt was spent on purchases of businesses (£44.7M) and the repayment of some of the bank loan (£40M) which leaves £34.6M to be spent on the cash flow. As we can see, the cash flow at the end of the year was £30.4M so this was entirely due to the PFI disposals. Were it not for this, there would have been a negative cash flow here.

Overall then, this cash flow looks impressive at first glance but when it is realised that the positive cash flow is entirely due to the one-off disposal of the PFI investments, it is a little less impressive and if that healthy dividend is going to be sustained, there needs to be a slight increase in cash.

The UK accounts for at nearly 3/4 of the group profits, with the Middle East and Australasia accounting for most of the rest. A modest amount of profit is coming from the Far East, but this figure is increasing. The group incurred a loss on operations in the rest of Europe and the Americas.

During the year, the group made two acquistions. BEST made £1.6M in profit last year and contributed £1.4M to group profits since acquisition and Advantage Healthcare made £2.6M last year and contributed £100K since acquisition. The group has decided that each one is worth between £13M and £14M of Goodwill. After the balance sheet date, the group purchased Willbros Middle East Ltd which owns oil and gas service businesses for a total consideration of £26M, including £19M of Goodwill and intangible assets.

The revenue growth seen in UK support services was primarily down to new business with existing customers. This is exemplified by the relationships with Alliance Boots which grew from a contract providing cleaning services for some stores to total facilities management for the office locations and cleaning services to over 1000 stores in both UK and Ireland. As well as increasing revenue, the group has also worked hard to improve margins. During the year new business was won with Scottish Power, Carphone Warehouse, West Yorkshire Police, Borough of Southwark, London Universities, the Environment Agency and the Defence Infrastructure Organisation which has caused the future workload to increase to an impressive £5.2B.

The division was strengthened by the acquisition of BEST, a Yorkshire based providers of training for people trying to get back to work; and Advantage Healthcare, which provides case management, social care, clinical and nursing services for primary care trusts, private clients and through GP referrals. This increase in healthcare capability helped the group win a contract with Leicestershire NHS Trust to provide complete facilities management and consultancy, supporting at least three hospitals and other facilities. Another area the group is looking to expand into is the justice market, providing facilities management to prisons.

Although UK support services provide the bulk of the revenue, the international support services sector is a growing area for Interserve. Some new contracts include an extension to onside mechanical maintenance to an Oryx gas to liquid plant; a five year service contract and turnaround services to Shell Pearl; a five year contract for plant modification works and maintenance services for Dolphin Energy (both on shore and off shore) and the fabrication and installation of pipework for a Punj Lloyd polysilicon plant.

The group has been investing in new businesses here too, with the acquisition of TOCO, an Oman based business specialising in fabrication, maintenance and repair services to the oil and gas industry and the group are confident about future prospects in this area.

Although revenue for UK construction increased slightly, a more competitive environment squeezed margins and the contribution to profit fell from last year and these low margins are expected to continue in the medium term. Interserve is moving more into growth markets, such as energy from waste and have completed the design and build of a plant in Westbury and have also won a £150M contract with Viridor for the construction of Glasgow’s new residential waste treatment facility. The group also have a contract to renovate an old building in Edinburgh to turn into flats. Other new contracts include a project for a Land Rover factory, contracts with NHS, National Grid, English Heritage and the Highways agency. Future workload currently stands at £900M and whilst the board expect the current year to remain challenging, they feel that this visibility of future work sits them in good stead.

Revenue from International Construction is somewhat less than in the UK but the contribution to profits are similar due to the higher margins. Unfortunately revenues and profits fell during the year due to client caution. Although in the UAE there are signs of optimism, with new contracts including a £11M Fujairah road system project; a £6M region HQ for Habib Bank; a £38M Fujairah city centre shopping centre project; a £49M Jumeirah Beach shopping centre project and a £28M contract for General Electric for an Emirates Airlines engine overhaul facility. The fit out business won contracts for hotels in Abu Dhabi and Ajman.

Conditions in Qatar have been somewhat more subdued but a contract to fit out the main halls and lounges in Doha Airport has been won as have fit outs in two office towers in Doha. Other projects have included a £30M project to build two substations for Hyosung and chilled water piping diversions for Ashghal who are building an expressway in Lusail after the group had previously built a sewage plant for them.

Market conditions in Oman were stable over the period with good levels of activity in defence and industrial development. Notable contracts included a substation for Arabian Industries and work for the new Military Training College in Seeb. The fit out and joinery businesses did well with the completion of the Sohar Court complex a highlight. In the short term, growth in the region is likely to remain subdued but with the World Cup coming to Qatar in 2022 and economic growth forecast in the region as a whole, long term prospects look better.

With higher margins, equipment services is another important area for the group and this business has seen a gradual recovery in their markets. In the Middle East, Saudi Arabia remained the largest market and projects included the provision of equipment to the Roots group at the Mecca Grand Mosque; in Jeddah, their equipment is being used to build the new approach roads to the airport and there are several infrastructure projects in Riyadh.

The business performed well in Oman and projects included the redevelopment of Muscat and Salahlah airports. In the UAE there are signs of more substantial infrastructure projects coming to market and a contract was won to supply equipment for the presidential palace in Abu Dhabi. Conditions in Qatar remained subdued during the period. Things picked up nicely in South Africa with new contract wins for Flicksburg reservoir with Rawacon and the supply of shoring equipment to the Mhlatshane waste water treatment works for Cyclone Construction in Kwazulu Natal. Interserve continued to supply equipment to the Gruluk Bunker in connection with a new power station in Lephalale.

In Australia, projects included Gorgon in W. Australia and three other LNG plants on Curtis Island and although the pace of investment in Australia has slowed recently, it still represents and import and relatively stable market for the group. Following the earthquake in Christchurch, the group has been supplying a lot of shoring equipment and framework which has driven very good results in New Zealand. Work in Hong Kong revolves around a new cruise ship terminal and an integrated public transport project. The group had a strong year in the Philippines with demand being driven by projects such as the new arena and stadium complex.

Demand in Europe was generally subdued, reflecting the continued construction pressures in this region and Interserve underwent some efficiency savings to make sure they were well positioned in the smaller market place. Some important projects included the support of a stadium roof in Marseille and Spain where they are working with Horta Costada on plans to increase capacities ahead of the UEFA 2016 tournament in Spain.

For much of the year, conditions in the US were difficult and the group responded with a number of organisational changes but towards the end of the year the construction industry showed some signs of recovery. Elsewhere in the Americas, market conditions were more favourable and there has been increased investment in Chile and Panama with Chile in particular performing well, driven by demand in mining. Interserve are planning a market entry into Colombia too. Going forward, revenues in Equipment Services are predicted to continue to improve.

I feel results for this year were fairly mixed but overall seem quite positive. Revenues were up for most sectors but they were reduced in international construction where Qatar remained subdued and in investments where many of the PFI companies are being offloaded. One big story in these results was the £115.5M made on those PFI sales, which was invested in reducing debt and in three new acquisitions. Net tangible assets are actually quite low for a company of this size and reduced further during the year predominantly due to the larger pension obligations. The positive £30.4M of cash flow was entirely down to the PFI sales and if these sales were taken out (a very crude measurement I know!) then there would have been a negative cash flow of £4.2M, which is no disaster but could be better.

Going forward, the low margin work in the UK looks set to continue as the Government outsources more work to cut down on costs. Internationally, the UAE seems to have picked up and Oman is strong, with Qatar still experiencing some difficulties. Australia is still doing quite well but there is evidence of reduced infrastructure spending recently, which is a bit worrying. Europe, as would be expected, remains difficult but it seems Interserve don’t have a huge exposure there.

I do like Interserve as a company. They seem to be quite well diversified in both products (they don’t rely entirely on construction) and geographically and I particularly like their focus on the Middle East. The dividend has a yield of 4.2% which is not that bad but has been better and the P/E ratio of 10.6 still seems rather cheap despite the increase in share price. I have slight concerns as to how the sale of the PFI assets will affect the bottom line once the revenue from them is taken out and whether the group can maintain a positive cash flow without the one-off sale of PFI investments this year. I think overall I still consider Interserve to be good value.

On 2nd April, Interserve announced a new contract with Magnox who operate 10 nuclear power stations in the UK and seem to be responsible for decomissioning them. The contract is initially for three years and is worth £80M. Interserve will provide a full range of facilities management, including mechanical and engineering maintenance, catering, cleaning, office services, grounds maintenance and civil works. The group is also the sole contractor on a four year framework agreement with Magnox to design and construct facilities to store intermediate level waste. This seems like a good contract win in an interesting sector.

On 3rd April, Interserve announced a new joint venture to develop the Haymarket area of Edinburgh into offices, retail units, hotel accomodation and underground parking. They have invested £10.5M in the project and construction works should be at a value of £150M.

On 13th May an interim management statement was released that stated trading was pretty much as expected. Over £700M of new work was secured in the period.

On 9th July the group released a statement that said they continued to perform in line with expectations with a strong future workload. Short and sweet.

On 15th July the group announced that they had entered into an agreement to acquire Topaz Oil and Gas based in UAE for US$46M. The company provides oil field maintenance, fabrication and construction services to the Middle East, particularly in Abu Dhabi and Fujairah. Current clients include Shell, ADOC, ADNOC, Qatar Gas, RAK Petroleum and Aker Solutions. This seems like a pretty decent opportunity, although not much detail on the financials has been provided.