Laura Ashley have now released their results for the year ending 2013

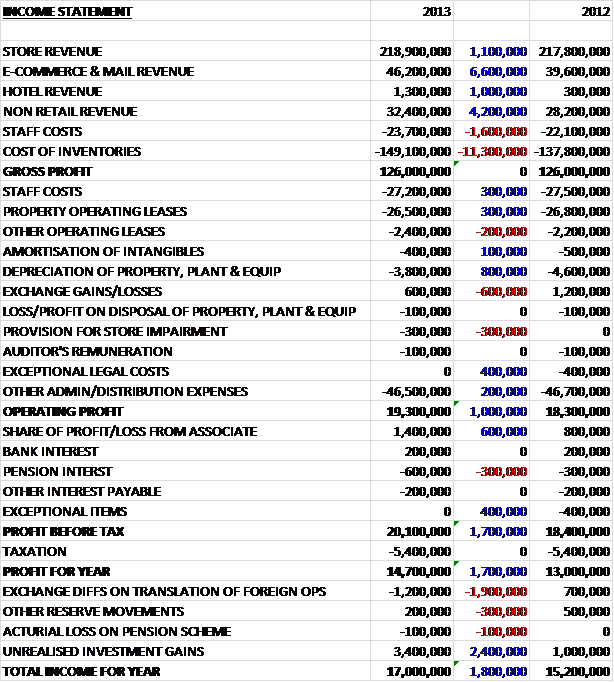

Although store revenue was fairly flat, this year saw another increase in e-commerce and non-retail, plus the first real revenue contribution from the hotel. The actual profit contribution from stores was down, however, with an increase in contribution from E-commerce and non-retail. The hotel was marginally loss making in the period. Costs of sales were also up, however, to leave the Gross profit completely flat at £126M. As far as other expenses were concerned, there was not much change on last year with the biggest being a £800K fall in depreciation. These slight changes in admin costs meant that the operating profit was £1M better than last year, at £19.3M. The group also received a better return from the associate (Laura Ashley Japan) and an unchanged tax charge left the profit for the year £1.7M higher at £14.7M. Total income for the year showed a similar increase as adverse exchange differences were counteracted by an increase in unrealised investment gains.

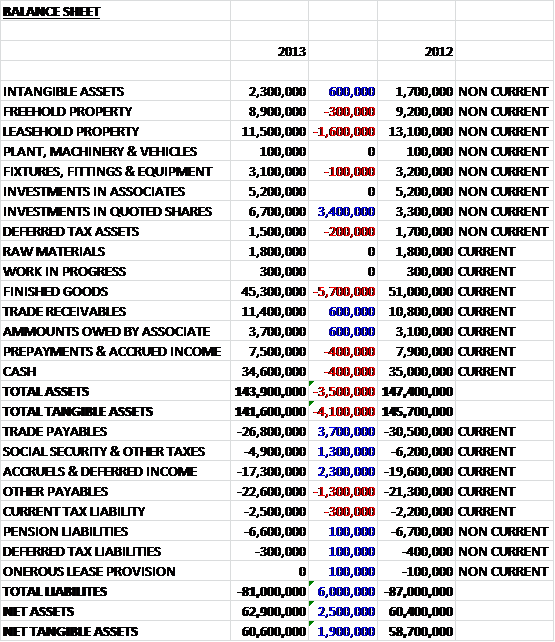

Overall Total Assets were down by £3.5M year on year, with a £3.4M in the value of investments in quoted shares being counteracted by a £1.6M reduction in the value of leasehold property and a £5.7M reduction in inventories. Liabilities fell by £6M, driven by a £3.7M fall in trade payables, a £2.3M reduction in deferred income and a £1.3M reduction in social security payables. This meant that net tangible assets were £1.9M better off at a very healthy £60.6M.

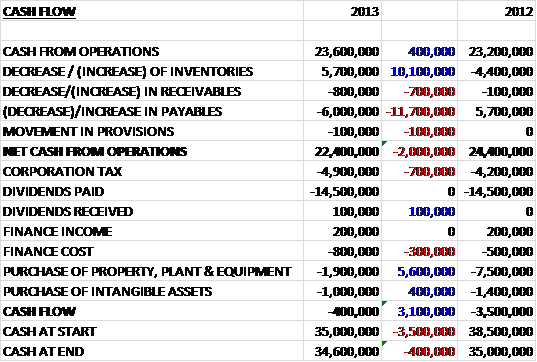

Before changes in capital, the group achieved a cash flow £400K better than last year. A decrease in inventories was more than counteracted than an increase in receivables and a decrease in payables which left the cash from operations £2M lower than last year at £22.4M. The largest cash expense by far was the £14.5M spent on dividends (no change from last year). Otherwise, nearly £5M was paid out in tax but the main difference from last year was the £5.6M less that was spent on the purchase of property and equipment as the previous year included the purchase of the hotel. Overall, the small cash outflow of £400K was £3.1M better than last year and a fairly decent performance.

During the year the group opened 6 new UK stores and closed 5 stores for the on-going re-alignment. Like for like sales in UK stores were actually down by 0.1% and gross margin rates fell by 1.9%. In the UK, online revenues are becoming more and more important, now making up 16% of UK sales and e-commerce sales were up nearly 20% year on year to more than counteract falling mail order sales. The group now sell to France, Germany, Austria, Italy and Switzerland in addition to the UK – so I would have thought more opportunities to expand there. A mobile site has recently been introduced to keep up with the times.

In the UK, furniture is the biggest proportion of sales and it was fairly flat – increasing just 0.5% on last year. Home Accessories did very well, increasing by 7.6% and apparently is becoming more relevant for gifting, giving a boost in sales. Decorating sales ticked up ever so slightly, up 0.7% and this sector is still an import driver for other areas. Unfortunately fashion sales fell by 5.6% year on year after a poor second half of the year. During the year, the group re-launched their fragrance, “Number 1” and sales of that are apparently going well.

Franchise revenues continue to be a more important source of income and they increased by 13% on last year with stores in 28 countries, including new ones in Russia, Poland and the Baltic States. Licensing income is also becoming an important source of profit as this increased by 17% year on year. Licences were awarded for conservatory furniture and shower enclosures during the year. The hotel has now been refurbished and will be launched as a Laura Ashley boutique hotel shortly. It will be interesting to see how the hotel, purchased from Corus hotels (also mostly owned by the same Malaysian outfit as Laura Ashley) adds to profits in future and whether this is a new venture for the group or just a one-off.

This year has got off to a decent start, with the group announcing like for like sales up by 2.7% for the first two months. Overall this is a fairly good update, it is clear that a falling contribution from the UK stores is being counteracted by increased online sales, franchises and licences and Laura Ashley seems to be adapting to the changing retail environment fairly well. One area of slight worry is the slightly negative cash flow but given the large cash pile and lack of debt, this is not a pressing concern. The current yield is a very good 6.9%, and is just about covered by earnings. The P/E ratio of 14.3 shows that this share is not as undervalued as it once was but it is difficult to safer source of a 6.9% return anywhere else. Still worth topping up in my view.

On 21st May, Laura Ashley announced that they will be paying a special dividend of 0.5p per share. Apparently this is to commemorate the 60th anniversary of Laura Ashley. The dividend is not covered by earnings and is taken from the cash reserves. It seems like a rather arbitary reason for a special dividend and is perhaps a way to reduce the cash pile. In any event, it was a nice surprise as a shareholder.

On 13th June the group released an interim statement. In the release, the say that total retail sales fell by 0.6% due to a weak performance in the fashion sector. They attempted to blame this on the weather – I am having none of that! E-commerce sales growth was 4.4% and 10 new franchise shops were opened. This profit warning was a bit of a disappointment but it is still possible to turn this around and I am not overly worried yet.