Kalibrate has now released its interim results for the year ending 2015.

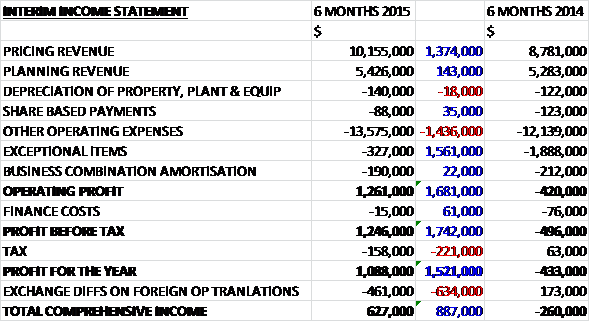

Revenues increased when compared to the first half of last year with a $1.4M increase in Pricing revenue and a $143K growth in Planning sales. Operating expenses also increased but the large reduction in exceptional items helped operating profit increase by $1.7M. After a slightly higher tax bill, the profit for the half year stood at $1.1M, a favourable swing of $1.5M, almost exactly the same as the reduction in exceptional items.

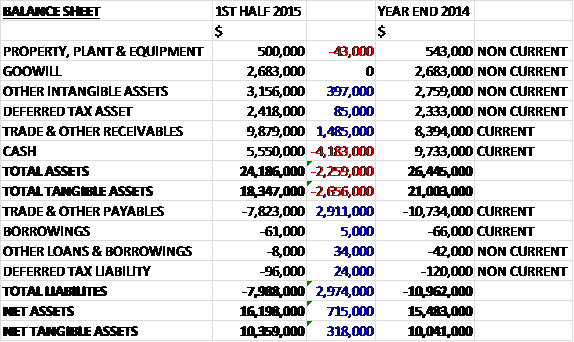

When compared to the end point of last year, total assets decreased by $2.3M driven by a $4.2M fall in cash, partially offset by a $1.5M growth in receivables. Liabilities also fell during the period due to a $2.9M decline in payables to give a net tangible asset level of $10.4M, a $318K increase when compared to the end of 2014.

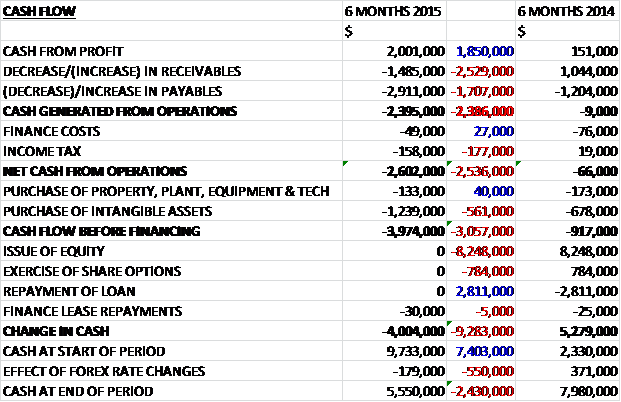

Before movements in working capital, cash profits increased by $1.9M before an increase in receivables, relating to a few transactions that closed near the year end, and a decrease in payables meant that there was a cash outflow of $2.6M from the operations compared to an outflow of $66K this time last year. After capital expenditure and a small amount of finance lease payments, the group lost $4M in cash during the six month period to give a cash level of $5.6M at the half year point which seems to be quite a disappointing performance.

During the period the group did not lose a single customer with 100% client retention which is really rather impressive. The group also managed to sign an additional four of their clients onto both their pricing and planning services, bringing the total using both up to 31. Good progress has been made in expanding the global footprint by adding clients in the new markets of Mexico, Brazil, Kenya and the Philippines with India, Mexico and Kenya all announcing that they are planning on deregulating their markets.

Revenues at the Pricing division increased by 16% as a result of new license sales and selling into both new and existing clients but underlying operating profits fell by $128K to $874K. The group now has 22 managed services clients, an increase of 10 from the start of the year and the focus remains on converting existing clients as well as adding new customers to the managed services offering and they are in the process of increasing operational and sales resources to support this growth potential. Planning revenues increased by just 3% but underlying operating profit increased by more than $200K to $904K driven by a 43% growth in North American business that was offset by declining revenues in Japan due to a reduction in site count in the country. There has been increased interest in Europe where the business has signed agreements to conduct market studies in Ireland and Finland.

Geographically the group achieved a modest 5% revenue growth in North America with the 43% increase in planning sales as a result of cross-selling planning products to existing pricing clients and generating new revenue from additional data reselling to existing clients. The pricing division saw a slight decline in revenues in the region as several clients move to the SaaS model instead of the perpetual license up front model. Revenue in Europe increased by 60% due to the previously mentioned large contract with the major oil company and the signing of several new planning deals in Finland and Ireland. Revenues in the rest of the world fell by 13% year on year as the Japanese market declined due to the reduction in sites to survey, offset by some improvement in market studies in Africa. With the deregulation trends continuing in various countries, the group sees growing demand for both the pricing and planning product lines in the rest of the world with an expansion of the client base in Malaysia and new market studies in Kenya and Morocco. In addition the group completed a consulting consignment for a client in Mexico regarding the deregulation plans in that country which they hope will lead to pricing and planning opportunities there.

In September the group introduced the Kalibrate Cloud platform that houses all of their pricing solutions in one cloud based platform and during the second half of the year they expect to add their planning software product onto the platform. The group has devised the “7E” process that combines information amassed in their data warehouse to provide a score upon which clients can benchmark the seven elements that make retailers successful in their marketplace – pricing, location, brand, facility, operations, merchandising and market. This score allows them to provide strategic consulting advice alongside their software products. The bi-product of providing market planning service throughout various geographies enables the group to amass data that they can utilise to support their clients within the 7E process or allow them to sell the data to other third parties. Most notably, they have up to date traffic statistics at over four million traffic points in North America and various other countries around the world.

The group have now fully implemented their first major multi-country managed services contract for a major oil company’s petroleum retail network that is generating about $2M per annum in recurring revenue. During the year the group also managed to move 9 clients representing $2.9M in bookings from the historic perpetual license structure to the SaaS platform which has helped achieve about $20.7M in annual recurring revenue, up from $19.6M at the start of the year. The order book has increased by 13% to $23.6M at the period end.

The market that the group operates in has recently experienced a significant decline in the market price of petroleum products, along with a collapse in the price of crude oil. In environments such as these the integrated refiners/retailers can experience capital pressures which may lead to delays in capital spending. So far the group has not experienced any effects on its business but it something that management are keeping a close eye on. The group has announced that it plans to invest across the business over the coming years to strengthen the sales and marketing efforts, increase product development resources and adding resources to support growth in the managed services business. These investments are likely to increase the cost base for the company going forward.

As they enter the second half of the year the board remain confident that the group is on track to meet expectations for the year as a whole. The decline in oil price has actually improved margins for many fuel retailers and the group enters the second half of the year with a strong deal pipeline and is on track to meet expectations for the year as a whole. Net cash at the period end stood at $5.6M, some $4.1M lower than at the end of last year and no dividends were proposed during the period.

Overall then this seems to be a solid if rather unexciting performance. Underlying profits were broadly flat and net assets increased slightly, although there was a cash outflow at the operating level which is possibly caused by the move onto the SaaS system for some clients that involve less upfront cash. The fact that the group had 100% client retention during the period is impressive, the order book is improved and there seems to be some decent opportunities in Mexico, Malaysia and Kenya but the reduction in the oil price has the potential to be an issue and the board of flagged up an increased cost base for next year so there could be some headwinds. In conclusion, this is a company that I quite like but progress seems to be a bit slow so far for me.

On the 17th March the group announced that it had secured a contract with NIS in Serbia, one of the largest vertically integrated energy companies in South East Europe with operations in Bosnia, Hungary, Romania, Bulgaria and Serbia. NIS will utilise the group’s retail network planning and location analysis solution to optimize performance of its network of retail outlets that will help it decide where to build or remodel its retail sites. This deal adds three new countries to Kalibrate’s list.

On the 15th July the group released a trading update covering the full year ending 2015. Overall the board expects EBITDA to be in line with expectations.

During the year the group has secured multiple new contract wins which have been secured largely on a SaaS basis which offers longer term client relationships of about three to five years and higher overall gross margins. At the same time they have been converting a number of existing perpetual license clients to SaaS based agreements. This acceleration has had some short term impact on the revenue and cash generated during the year, however. Annualised recurring revenues at the year-end stood at $21M compared to $19.6M at the same point last year and the group’s order book increased by 15% to $41.1M. The cash balance at the same point in time stands at $4.6M.

The group has seen revenue growth in both core geographies and new markets with new perpetual license wins in Q4 with two new North American and one new European fuel retailer. The group has secured new clients for its Planning services in Bosnia, Bulgaria, Chile, the Czech Rep, Ireland, Kenya, Mexico, Romania and Serbia and has also begun to deploy its pricing services in Brazil.

Overall this is a decent enough update in my view but it will be interesting to see what effect the move to SaaS contracts has had on cash flow.