Keller has now released their final results for the year ended 2018.

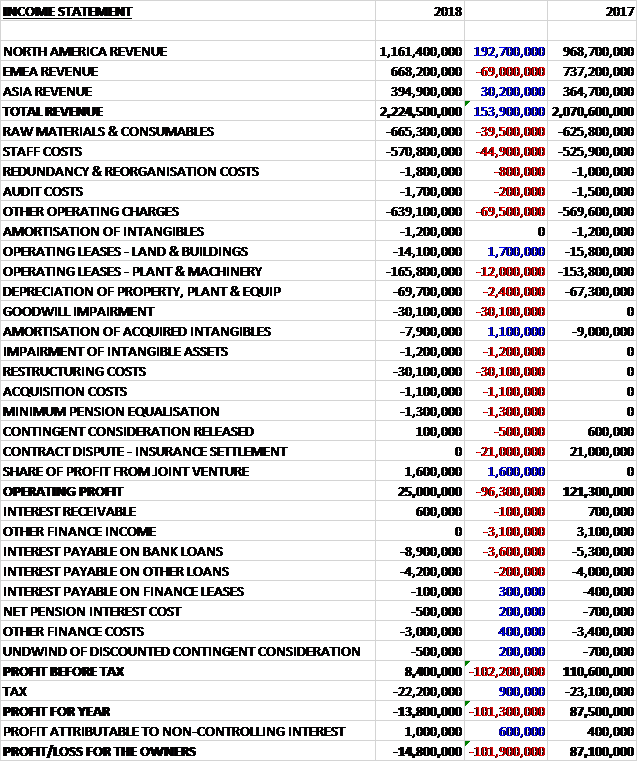

Revenues increased when compared to last year as a £69M decline in EMEA revenue was more than offset by a £192.7M growth in North America revenue and a £30.2M increase in Asian revenue. Raw material costs increased by £39.5M, staff costs grew by £44.9M and other operating charges were up £69.5M. Operating lease costs increased by £10.3M and depreciation increased by £2.4M. There was a £30.1M goodwill impairment and £30.1M restructuring costs along with a £21M reduction in insurance settlements following last year’s contract dispute. All of this meant that the operating profit was £96.3M lower. Finance income reduced by £3.2M and interest costs on bank loans were up £3.6M before a £900K fall in tax charges gave a loss for the year of £14.8M, a detrimental movement of £101.9M year on year.

When compared to the end point of last year, total assets increased by £59.8M driven by a £42.8M growth in cash, an £11.9M increase in plant, machinery and vehicles, an £11.9M increase in trade receivables, a £10.6M growth in land and buildings and a £7.7M increase in inventories, partially offset by an £18.1M growth in goodwill, and a £12.4M increase in deferred tax assets. Total liabilities also increased during the year as a £15.3M decline in accruals was more than offset by a £99.5M increase in loans and borrowings and a £19.7M growth in advance billings and other payables. The end result was a net tangible asset level of £291.9M, a decrease of £9.4M year on year.

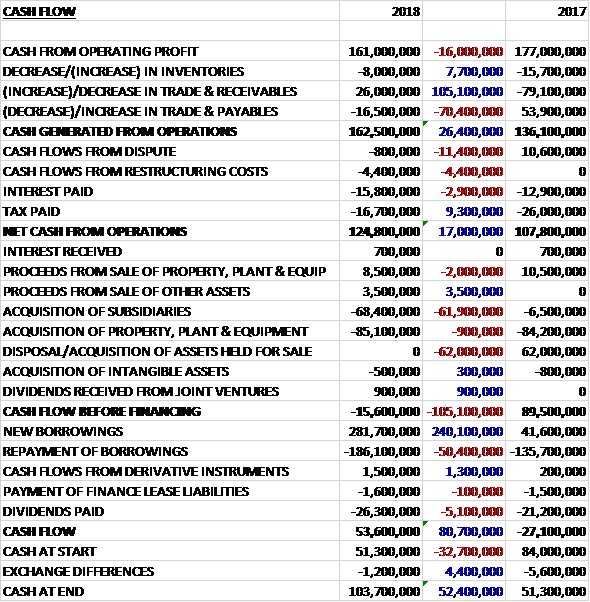

Before movements in working capital, cash profits declined by £16M to £161M. There was a modest cash inflow from working capital compared to cash outflow last year. There was no insurance cash from the contract dispute, which was £10.6M last time, restructuring costs were £4.4M and interest payments increased by £2.9M. Tax charges were down £9.3M, however, to give a net cash from operations of £124.8M, a growth of £17M year on year. The group spent £85.1M on property, plant and equipment and £68.4M on subsidiaries to give a cash outflow of £15.6M before financing. The group took out a net £95.6M of new borrowings and paid out £26.3M in dividends to give a cash flow of £53.6M for the year and a cash level of £103.7M at the year-end.

The underlying operating profit decreased by £12.1M with the headwind of adverse forex rates causing a further 3% reduction to the constant currency call of 8%. Moretrench contributed 9% so the group’s organic performance saw a 17% reduction.

The operating profit in the North American division was £78.6M, a decline of just £100K year on year, although underlying profits were up 3% on revenues that increased by 24%. Without Moretrench, however, organic profits fell by 9% with the adverse raw material pricing at Suncoast being the biggest factor. All of the businesses had good revenue growth, benefiting from positive market conditions. The overall margin declined, reflecting a decrease at Suncoast due to raw material cost increases as well as general adverse North America project mix and performance in the second half compared to a strong second half of 2017. Hayward Baker saw strong revenue growth but profit below the record level last year. The integration of Moretrench has gone well. Cost reductions exceeded plan and the nine months of profits were ahead of original expectations. They are now starting to see revenue synergies, with Moretrench’s specific niche products of ground freezing and dewatering being offered throughout the group.

The three US piling businesses all improved revenue and profit. In Bencor there has been no change regarding the adjustment due to the scope increase on a large term contract. They continue to negotiate the adjustment with the client and remain confident of the position they have taken. Suncoast had healthy revenue growth but its profits reduced by £7M as a result of increases in steel prices that it was unable to pass on to customers in full, and the record rainfall in Texas in September and October. The margin has now been restored by passing the costs on to customers.

Keller Canada is making good progress on the east coast but continues to operate in difficult markets in the west. The business substantially grew its capability in Vancouver and is now better placed to take advantage of the strong market on the west coast of Canada. Going forward, the year-end order book of work to be undertaken over the next year was 19% above last year, giving confidence for 2019.

The operating profit in the EMEA division was £39.7, a decline of £13.6M when compared to last year. The underlying operating profit was down 24% on revenues that declined by 24%. This significantly lower result was a consequence of two large projects coming to an end in the first half of the year, including the Caspian project. The completion of these projects resulted in a benefit of £16M compared to £45M last year and outside of these two projects, the performance in the region improved considerably.

All the core businesses in continental Europe continued to benefit from a sound market environment and performed well. South East Europe recorded another record year and the operations in Germany continued to grow on the basis of ongoing high demand and extended product offerings. The UK experienced a generally hesitant commercial investment climate but major infrastructure projects are developing, including HS2, and the board expect the market for geotechnical work to pick up towards the end of 2019, extending well into 2021.

The operations in the Middle East experienced a relatively quiet year following the completion of large projects in Abu Dhabi and Egypt. New projects continue to develop slowly resulting in lower utilisation in the second half of the year. They have secured some new projects in the region and on the basis of improving fundamentals they see the prospects for the Middle East as positive.

The French speaking countries business performed solidly, helped by good performance in North Africa. Their geotechnical portfolio of near-shore marine solutions, stone columns to mitigate liquefaction and a range of piling solutions has secured some interesting projects, particularly in Morocco and Algeria. The French domestic market was characterised by good demand around Paris leading to niche opportunities across the country.

Brazil and South Africa both experienced a difficult year. Both countries suffered heavy margin pressure requiring the group to adapt their local capacity. They have taken proactive measures to scale back their operations and as a result to maintain bidding discipline. The challenges in South Africa have been compensated to an extent by the group’s strong presence in sub Saharan Africa. They continue to monitor the development of the political situation in Brazil and will respond to developments.

The year-end EMEA order book of work for the next year was around 8% down on last year reflecting the run-off of the large projects. Excluding these, it was 4% down.

The operating loss in the APAC division was £18M, an increase of £1.5M compared to 2017. The underlying loss increased by 10% despite revenue growing by 13%, driven by good increases in India and Australia. The increased loss was due to deteriorating ASEAN market conditions and poor project performance in ASEAN and Waterway, prompting a review of both businesses.

In ASEAN they completed a review of their portfolio. As a result of the deterioration in the Malaysian market conditions and disappointing project performance, they took the decision to downsize the business. They therefore exited their heavy foundations activities in Singapore and Malaysia which have become highly commoditised and continue to see competitive pricing pressure. These activities had a combined annual revenue of around £60M. Going forward, they are focusing on higher margin ground improvement activities such as vibro, grouting and deep soil mixing. The restructuring of the business is now substantially complete although some piling projects extend through the first half of 2019.

In Waterway, they took the decision to exit the highly congested Australian bridge superstructure market and refocus on higher margin marine infrastructure projects. Whilst Austral and Waterway retain their independent brands, they are sharing key leadership roles and functional support between the two businesses. They continue to expect that legacy and lower margin contracts in Waterway will be complete by the end of the first half of 2019. Austral and Waterway are now aligned to pursue a selection of east coast marine projects predominantly in the defence sector.

Austral had a record year due to a strengthening in investment by the mining industry in Pilbara. The business has good tender and prospects lists and is set for another strong year in 2019.

The group’s geotechnical business in Australia saw a year of consolidation as it adjusted to a softening in the property sector and a government shift towards major transport infrastructure expenditure. This segment of the market offers good revenue opportunities but at lower profitability levels. The business returned to profit in 2018 but the outlook for 2019 remains muted. The large Melbourne metro project is experiencing client driven delays that are subject to a claim and this claim is not yet recognised in the 2018 results. The Indian business has a good year and has a healthy pipeline of major infrastructure projects for 2019.

The year-end Asia Pacific order book of work to be undertaken over the next year was down 43%, particularly impacted by a rebasing in ASEAN and with some softening in the three Australian businesses. All three Australian businesses have a strong prospect list, however, and a higher than normal list of tenders under review. A number of significant tenders will be decided late in Q1 2019. Overall the board expect the division to return to profit in the second half of 2019.

In March the group acquired Moretrench America Corp, a geotechnical contracting business operating along the east coast of the US, for a cash consideration of £64.7M, generating goodwill of £9M. In June, they acquired Sivenmark Maskintjanst, a sheet piling specialist based in Sweden, for a cash consideration of £2.1M, generating goodwill of £800K. During the year the acquisitions contributed a net profit of £5.5M.

There were a number of non-underlying items over the year. The amortisation of acquired intangibles relates to the Keller Canada, Austral, Bencor and Moretrench acquisitions. The goodwill impairment relates to the ASEAN Heavy Foundations, Waterway, Franki Africa, Brazil and Wannenwitcsh units, all of which are experiencing significantly depressed trading conditions. The impairment of intangible assets relate to the impairment of the Tecngeo and Franki Africa trade names capitalised on acquisition.

In November the group announced a restructuring programme. They have taken a £30.1M restructuring charge, of which £21.6M was non-cash, relating to asset write-downs, redundancy costs and other reorganisation charges. Affected businesses are ASEAN, Waterway, Brazil and Franki Africa and includes the write-down of surplus equipment to current market values.

Going forward, overall market fundamentals are healthy and the group remain well positioned to benefit from the global trend of urbanisation. In North America the outlook is good with robust markets and solid growth expected, and an improvement in margin anticipated as cost increases at Suncoast start to be fully passed through. In EMEA they benefited from the large, highly profitable projects in the first half of 2018 which will not repeat in 2019. These projects aside, the outlook in the main markets is positive so the board expect progress in the core business.

In Asia Pacific, the decision to exit ASEAN heavy foundations will lead to a revenue decline in 2019. The main Asia Pacific markets remain mixed but the board expect that the measures already taken will return the division to profit in the second half of the year. In 2019 overall they expect revenue to be broadly flat with an improvement in margin and a good recovery in profit. The profit improvement, together with a focus on cash generation, means they expect debt leverage to reduce significantly by the year-end.

At the current share price the shares are trading on a PE ratio of 27.8 which falls to 6.9 on next year’s consensus forecast. After a 5% increase in the total dividend but a reduction in the final dividend the shares are yielding 5.6% which is expected to grow to 5.9% next year. At the year-end the group had a net debt position of £286.2M compared to £229.5M at the end of last year.

Overall then this has been a rather tricky year for the group. Losses worsened and the underlying profit declined, the net asset base fell and although the operating cash flow improved, this was due to working capital movements and cash profits declined with no free cash being generated. Forex movements haven’t helped but the underlying business has faced quite a few problems. The North American business saw organic profits fall due to increased raw material costs, although these have apparently now been passed on and the region’s order book has improved.

The EMEA business struggled due to the fact that there was only six months of the large projects included. This will continue into this coming year and the order book has also declined somewhat. There are also issues in the Brazilian and South African businesses. Asia Pacific has really struggled due to difficult market conditions in Malaysia and some issues in Australia. Actions have been taken to improve this and the board expect a return to profit in the second half of the year.

So, there are tricky conditions here but it does sound as though the group is confident of an improvement so perhaps the shares are worth a punt with a forward PE of 6.9 and yield of 5.9%. Risky but potentially good value.

On the 16th May the group released a trading update. The board’s expectations for the full year remain unchanged. They have experienced modest trading for the year to date and continue to expect profits to have a second half weighting. The order book remains at £1BN, slightly lower than at the same point last year reflecting the restructuring in Asia Pacific. It grew in North America and EMEA.

In North America, the adverse steel cost impact in Suncoast experienced last year is now reversing and margins have returned to more normal levels. Noretrench is performing well and planned cost synergies have been exceeded. Elsewhere in North America, performance in the first four months has been weaker than expected, partly due to mix and partly due to additional costs to recover from the adverse weather conditions in January, but this shortfall is expected to be recovered in the second half.

In EMEA the European businesses are performing in line with expectations with a particularly strong performance from South East Europe. The Middle East is having a much quieter year to date following the completion of major projects and the slow development of new projects. Franki Africa has also continued to struggle and they are managing it closely, although it is bidding on new projects in the region. Brazil remains challenging although underlying performance is slightly improved compared to last year.

In Asia Pacific, the expectation to return to profitability in the second half remains on track. The restructuring and subsequent refocusing of the business in ground improvement is proceeding to plan, asset disposals will generate additional cash, and profitability continues to improve. India is performing to plan. Market conditions and performance across Australia remains mixed with a slower start to the year than expected but a recovery is anticipated for the year as a whole. Austral has been affected in the period by the recent cyclone which as impacted all mining and processing activities in the Pilbara, but is expected to recover well. The restructuring at Waterway is proceeding to plan, and additional action will be taken in response to the further deterioration in the market.

Overall trading performance in the four month period has been lower than anticipated but is on an improving trend. This, together with the final completion of the Caspian project in the first half means that results for the period will be materially lower compared to last year. They continue to expect as much stronger second half, and for full year revenue to be broadly flat, with an improving margin driving a recovery in profit. Net debt has risen slightly since the year-end but is expected to come down again by the end of the year.

This all sounds rather dependent on the second half to me and all a bit risky…