TT Electronics have now released their final results for the year ended 2018.

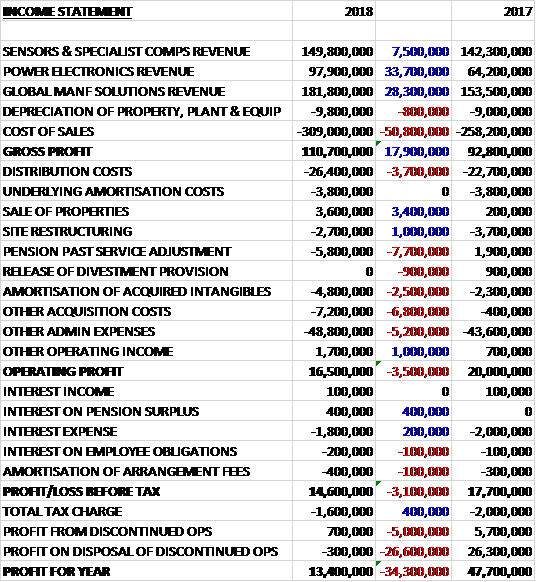

Revenues increased when compared to last year due to a £33.7M growth in power electronics revenue, a £28.3M increase in global manufacturing solutions revenue and a £7.5M growth in sensors and specialist components revenue. Cost of sales increased by £50.8M to give a gross profit £17.9M higher. Distribution costs were up £3.7M, there was a £7.7M detrimental swing in pension past service adjustments, amortisation of acquired intangibles were up £2.5M, acquisition costs were up £6.8M and other admin expenses grew by £5.2M. Offsetting this somewhat was a £3.4M profit from the sale of properties, a £1M decline in site restructuring costs and a £1M increase in other operating income to give an operating profit £3.5M below last year. There was a decline in net interest costs and the tax charge was down £400K to give a continuing profit for the year of £13M, a decline of £2.7M year on year.

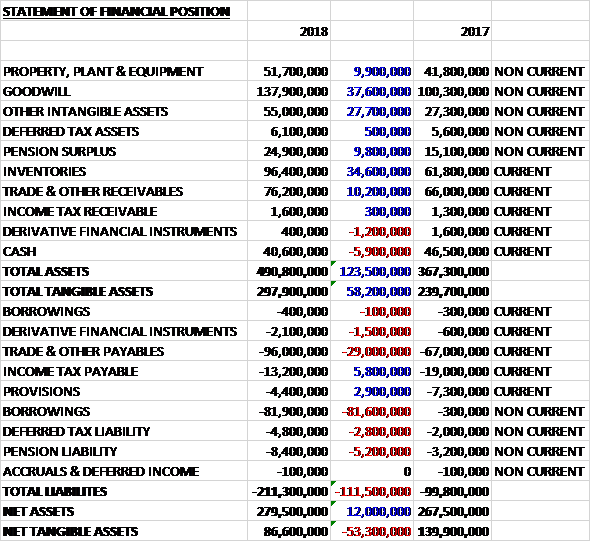

When compared to the end point of last year, total assets increased by £123.5M, driven by a £37.6M growth in goodwill, a £34.6M increase in inventories, a £27.7M growth in other intangible assets, a £10.2M increase in receivables, a £9.9M growth in property, plant and equipment and a £9.8M increase in the pension surplus, partially offset by a £5.9M decrease in cash. Total liabilities also increased during the year due to an £81.7M increase in borrowings and a £29M growth in payables. The end result was a net tangible asset level of £86.6M, a decline of £53.3M year on year.

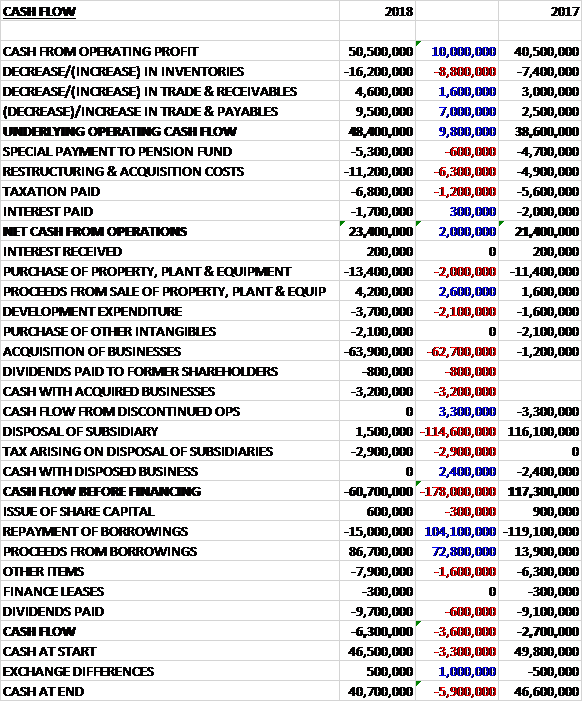

Before movements in working capital, cash profits increased by £10M to £50.5M there was a cash outflow from working capital which was broadly the same as last year but there was a £600K increase in payments to the pension fund, a £6.3M growth in acquisition costs and a £1.2M hike in tax payments to give a net cash from operations of £23.4M, a growth of £2M year on year. The group spent £13.4M on property, plant and equipment, £3.7M on development expenditure, £2.1M on other intangibles and £63.9M on acquisitions to give a cash outflow of £60.7M before financing. They took out a net £71.7M of new loans, paid out £9.7M and spent £7.9M on “other items” which meant the cash outflow for the year was £6.3M and the cash level at the year-end was £40.7M.

The underlying operating profit in the Sensors and Specialist components division was £21.3M, a growth of £2.5M year on year with revenue up 5% due to increased volumes in optical sensing and power management. During the year they announced a joint venture with UniRoyal for sensing and power management devices. The partnership will combine the group’s design engineering and worldwide distribution channels with UniRoyal’s penetration in the Asian market and higher volume manufacturing capabilities.

The division achieved strong growth in their sensing and power management lines as a result of market demand, particularly in products that measure current, with three notable new contract wins. They also saw growth from a platform of products that they identified as a priority in 2015 and have been in a ramp-up phase over the last three years. They continued to invest in the development of further platforms and launched five new sensing and power management products during the year.

Their optical sensors also saw good revenue growth. They won a new contract for a navigation system for an aerospace and defence customer and a new contract with a Taiwanese electronics manufacturer of products used in robotic automation. During the year they launched a quick response customisation programme resulting in 28 new orders of higher level assemblies for their optical sensor platforms, helping customers get their products to market rapidly.

The underlying operating profit in the Power and Connectivity division was £8.4M, an increase of £2.2M when compared to last year, with the Stadium acquisition contributing £3.5M. Revenue increased by 52% due to the acquisitions with organic revenue decreasing by 4% as expected due to the absence of the high margin one-off sales relating to the last time buy activity from a site closure in the US. In the second half of the year organic revenues increased by 4%.

During the year they have benefited from revenue growth from aerospace and defence product lines that were outsourced to them from OEM customers in 2017. They also benefited from increased demand for their power controls for navigation products in defence applications.

Following an increased focus on key account management, the division grew its revenues with these customers in aerospace and defence by 10%. The macro trend towards more electric aircraft continues to drive demand. They won a development contract to supply power modules for a new E-Taxi system on the Airbus A320. The system will power the aircraft using electricity rather than the jet engine during taxiing to and from the runway, resulting in reduced carbon emissions.

They made progress with their connectivity offerings, securing a partnership with a major distributor of IoT solutions based around single board computers. They saw good growth in the second half of the year across these offerings. They also launched a range of connectivity platform products to drive growth for future years. The IoT hardware platform product range has the ability to be rapidly customised for end customer requirements. An example application is for a European medical customer where they had good growth this year. This connectivity device is used to remotely monitor medical equipment and patients in their homes or care centre.

The underlying operating profit in the Global Manufacturing Solutions division was £11.3M, an increase of £4.8M when compared to 2017, of which £800K was due to the Stadium acquisition and £1.1M from the Precision acquisition) with revenues up 19% and 8% organically driven by the continued strength of the offering to Chinese and other Asian customers. They have also seen good growth from medical customers.

The strong performance also reflects improvements made in strategic business development, including training all their customer facing staff during the year. This has resulted in the development of strategic partnerships with their customers in addition to winning 14 new customers during the year, all of which will deliver multi-year revenues. They extended their strategic partnerships with their key customers, including an industrial labelling and packaging device company where they provide full system integration as well as value engineering support for the new customer’s new product development.

During the year they delivered strong operational improvement in their UK operations. They won six new contracts in the UK, including aerospace and defence contracts for a European aerospace OEM and a new contract for a military aerospace programme. They have been increasingly focused on key account management and this has resulted in a win with a US aerospace systems company following an introduction from their sales teams in the Power and Connectivity division. This contract is to provide systems integration for a navigation processor for commercial aerospace applications.

In April the group acquired Stadium for £45.8M in cash and assumed debt of £13.9M. The business contributed underlying operating profit of £4.3M since acquisition. In addition the group acquired Precision Inc for a cash consideration of £17.6M and a further £3M of contingent consideration. The business contributed £1.1M in profits. The Stadium acquisition generated goodwill of £27.3M and the Precision acquisition goodwill of £6.2M. The Stadium acquisition is performing ahead of expectations with the integration now complete ahead of plan. The integration of Precision is progressing well.

Stadium is a provider of connectivity solutions across industrial, transportation, medical, aerospace and defence markets. As part of the integration the group invested in engineering, business development and talent to strengthen the business. They established a new technology centre in Shenzhen, Chin, for custom engineering for connectivity solutions to help unlock opportunities from the market growth being driven by industrial internet of things solutions. Synergies have been realised including savings associated with the plc costs and the consolidation of sales operations in North America. Procurement and supply chain savings have been identified.

Precision is a designer and manufacturer of precision electromagnetic product solutions for critical applications, primarily in the medical market. The acquisition extends the group’s capabilities by adding new design, simulation and manufacturing capabilities including ultra-fine wire winding. The business provides an enhanced presence for the group in the US, with close proximity to a hub of medical customers in Minneapolis. The technical capabilities in the business have highlighted new opportunities to expand into aerospace and defence markets using the group’s expertise in these sectors. The board anticipate the integration and associated costs to be around £3M.

During the year restructuring costs amounted to £4.9M, of which £2.7M related to costs associated with site restructuring and £5.8M of past service pension charge as a result of UK pensions having to equalise male and female benefits, offset by a profit of £3.6M arising on the sale of a property. There were acquisition related costs of £12M which comprised £4.8M of amortisation of acquired intangibles and £7.2M of other costs associated with the acquisition of Stadium and Precision.

The group has agreed additional fixed pension contributions extending to 2020 amounting to £5.1M and £3.9M over the next two years. They have agreed fixed contributions of £600K per annum through to 2025 relating to the Stadium pension.

Going forward the group enter 2019 with a better balanced business, a strong order book and more self-help opportunities and remain on track to make further progress in 2019.

At the current share price the shares are trading on a PE ratio of 28.7 which falls to 12.8 on next year’s consensus forecast. After a 12% increase in the dividend the shares are yielding 2.8% which increases to 3% on next year’s forecast. At the year-end the group had a net debt position of £41.7M compared to a net cash position of £47M at the end of last year.

Overall then this year has been slightly mixed. Profits fell, but this was due to the pension adjustment costs and acquisition charges. Net tangible assets declined but the operating cash flow improved, although no free cash was generated. The sensors division performed well, as did the global manufacturing division with good demand from Asian and medical customers. The Power and connectivity division also performed OK, but this was due to the acquisitions and like for like results deteriorated due to the lack of the large one-off orders that occurred last year due to a US site closure.

The board seem fairly confident going into the coming year and I would like to see a year of consolidation and organic growth before more acquisitions. The forward PE of 12.8 and yield of 3% look decent enough and I’m tempted to buy back in here.

On the 21st March the group announced that non-executive director Jack Boyer purchased 11,000 shares at a value of £25K.

On the 2nd April the group announced that non-executive director Stephen King purchased 23,000 shares at a value of £51K.

On the 9th May the group released a trading update covering the first four months of the year. They had a strong start to the year with revenue 27% ahead of last year reflecting both business development actions and the integration of Stadium and Precision. Organic revenues increased by 10%. They have seen strong organic growth in both Power and Connectivity and Global Manufacturing Solutions but as expected revenues in Sensors and Specialist Components are unchanged compared to the prior year.

The order book remains ahead of the prior year, driven primarily by Global Manufacturing Solutions, and more than mitigating softer order intake in Sensors and Specialist Components. They have secured a number of new contract wins with both aerospace and medical customers.

In March they acquired Power Partners, a small US power supply provider, which will enhance their technology capabilities in power products and improve their medical market access. The consideration was $1.75M with an additional performance-based amount of up to $1.25M payable over two years.

On the 3rd July non-executive director Ann Thorburn purchased 45,000 shares at a value of £107K.