Tristel has now released its final results for the year ended 2016.

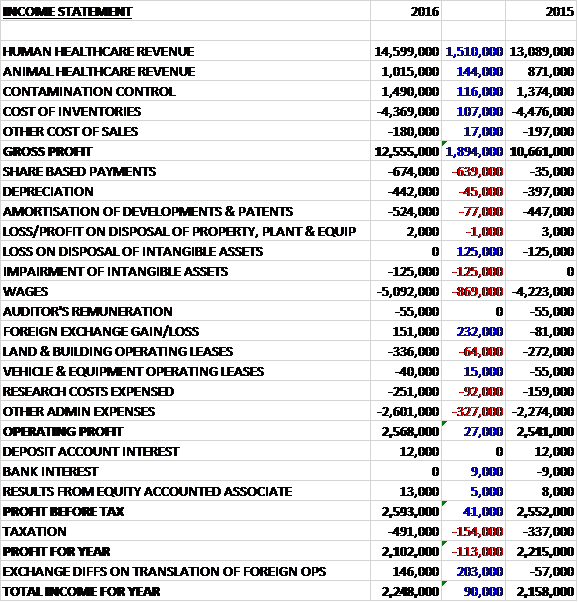

Revenues increased when compared to last year with a £1.5M rise in human healthcare revenue, a £144K growth in animal healthcare revenue and a £116K increase in contamination control revenue. We also see a modest decline in cost of sales so the gross profit grew by £1.9M. Share based payments increased by £639K and amortisation was up £77K with wages increasing by £869K. There was a £232K favourable movement in forex gains but operating leases were up £64K, R&D costs increased by £92K and other admin expenses saw a £327K rise to give an operating profit broadly flat, increasing by just £27K. This was wiped out by an increase in tax charges, mainly relating to deferred tax, and the profit for the year came in at £2.1M, a decline of £113K year on year.

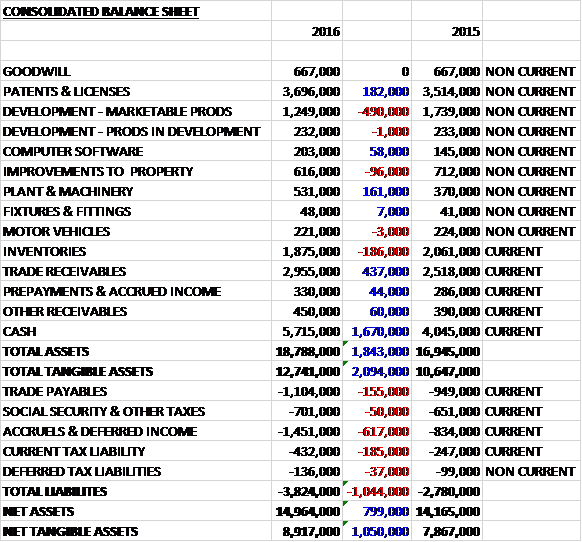

When compared to the end point of last year, total assets increased by £1.8M, driven by a £1.7M growth in cash and a £437K increase in trade receivables, partially offset by a £491K decline in the value of development costs. Total liabilities also increased during the period due to a £617K growth in accruals & deferred income, a £185K increase in current tax liabilities and a £155K growth in trade payables. The end result was a net tangible asset level of £8.9M, a growth of £1.1M year on year.

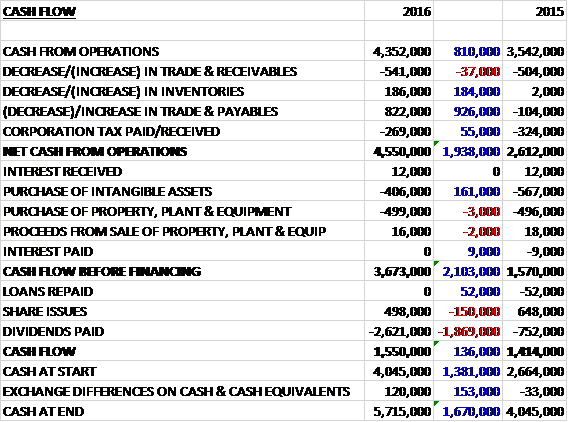

Before movements in working capital, cash profits increased by £810K to £4.4M. There was a cash inflow from working capital compared to an outflow last year so the net cash from operations came in at £4.6M, a growth of £1.9M year on year. The group spent £406K on intangible assets and £499K on tangibles to give a free cash flow of £3.7M, of which £2.6M was spent on dividends so the cash flow for the year was £1.6M and the cash level at the year-end came to £5.7M.

The gross profit in the Human Healthcare division was £11M, a growth of £1.6M year on year with most of the growth coming from outside the UK. The gross profit in the Animal Healthcare division was £682K, an increase of £125K when compared to last year with most of the growth coming from outside the UK. The gross profit in the Contamination Control division was £848K, a growth of £170K when compared to 2015 with the UK accounting for all of the growth as sales to the EU declined, although the group did make their first sales to outside the EU, accounting for £18K.

The pace of overall top line growth slowed slightly to 12% from 14% last year but overseas sales grew by 22% and 25% on constant currency terms with UK sales up 5%. The board are anticipating overall sales growth of between 10% and 15% over the medium term. They also have an objective of achieving a pre-tax profit margin of at least 15% even whilst investing in the US regulatory project – in comparison the margin last year was 17% and excluding the share based payments, was 19% this year.

Of the capex this year, £170K was spent on product development and testing and £120K on patenting. A further £340K was spent on regulatory approval programmes in 22 countries, which was expensed during the year. Included in this is £130K which relates to the initiative to enter the US which is progressing satisfactorily in accordance with the projected plan.

The group is currently pursuing a US FDA approval for two high level disinfectant products which are both classified as medical devices and require a 510 submission. The products are for Ophthalmology and Ultrasound. By mid-June the guidance notes were agreed and they submitted various scientific protocols for review and comment by the FDA by the end of October. Whilst it may take until early 2017 for all these protocols to be finalised, the group are proceeding to generate much of the data that they expect to be required.

Their plans are not restricted to FDA regulated medical device products, but will also include EPA regulated surface and water disinfection products. In September they made a pre-submission meeting request to the EPA and they will meet Autumn 2016. They have presented a pre-submission dossier to the EPA for the products Fuse for Surfaces, Duo for Surfaces, Jet Gel & Liquid for Surfaces, and Rinse Assure & Filter Shot for endoscope washer rinse water management. They are taking a similar approach for all the products above with Canada’s regulatory authority.

The group’s estimates for the potential value of the North American ophthalmology market is about £8M and the North American ultrasound market approximately £10M. They have made no assessment of how much of this potential market they can penetrate and they have not yet attempted to value the potential market opportunity in surface disinfection and rinse water management.

After the year-end the group acquired from the Australian distributor Ashmed its customer base, stock, fixed assets and staff for a total consideration of £1.1M in cash. The customer base and staff were purchased for £959K, recognised as intangible assets and stock was acquired for £119K. The board expect the acquisition to increase both the sales and gross margins achieved from their Australian business, in addition to being earnings enhancing.

At the current share price the shares are trading on a PE ratio of 34.1 which falls to 17.9 on next year’s consensus forecast. After a small increase in the final dividend, the shares are yielding 3.9% which drops down to 2.1% next year without the effect of the special dividend. The net cash position as the year-end was £5.7M compared to £4M at the same point of last year.

On the 13th December the group released an update where they reported that they expect period on period profit growth in the first half of the year. They expect pre-tax profit to be at least £1.6M compared to £1.5M last year before share based payments. They continue to perform in line with board expectations.

Overall then, the underlying performance this year has been pretty decent. The profit is down year on year due to the excessive share based payments which shows that even the most directed directors can get a bit greedy to the detriment of the company. Net assets improved though and there was a strong operating cash flow with plenty of free cash being generated. Much of the growth came from the human healthcare business and from outside the UK with the current rate of growth expected to continue.

The main event coming up is the FDA application which will consume quite a lot of time and money, but the rewards should be worth it. With a forward PE of 17.9 and yield of 2.1% this is not a value play but there is a decent amount of net cash on the balance sheet, the company seems to be growing fairly steadily and the profit so far in the first half is ahead of last year and in line with expectations so I will continue to hold.