Murgityroyd has now released their interim results for the year ending 2017.

Revenues increased by £1.1M when compared to the first half of last year, only about a quarter of which was due to the acquisition, with the rest of the growth due to the depreciation of Sterling, and cost of sales grew by £573K to give a gross profit £503K up. Admin expenses also grew, however, which meant that the operating profit declined by £637K. The tax charge declined by £149K which gave a profit for the period of £1.1M, a decline of £484K year on year.

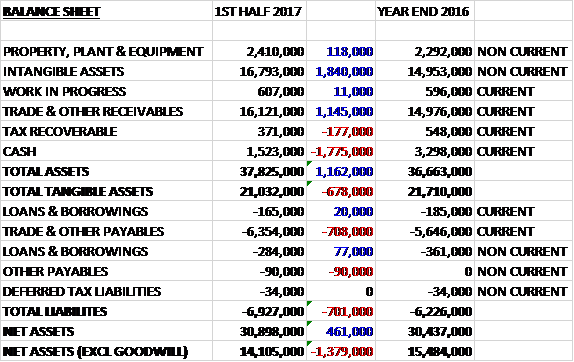

When compared to the end point of last year, total assets increased by £1.2M driven by a £1.9M growth in intangible assets and a £1.1M increase in receivables partially offset by a £1.8M decline in cash. Total liabilities also increased due to a £798K growth in payables. The end result was a net tangible asset level of £14.1M, a decline of £1.4M over the past six months.

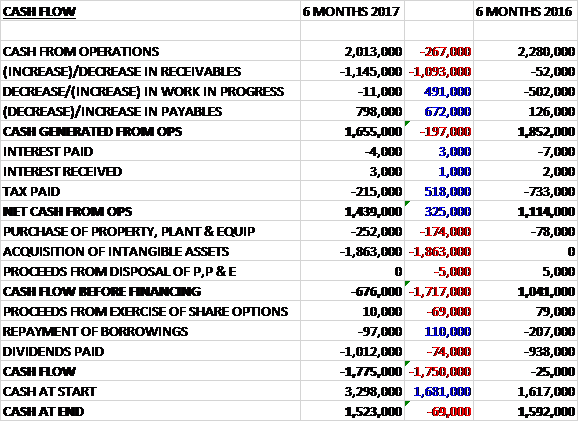

Before movements in working capital, cash profits declined by £267K to £2M. There was a modest cash outflow from working capital but after tax payments declined by £518K the net cash from operations comes in at £1.4M, a growth of £325K year on year. The group spent £1.9M on intangible assets and £252K on property, plant and equipment which meant that before financing there was a cash outflow of £676K. The group also paid out £1M in dividends which meant the cash outflow for the period was £1.8M and the cash level at the period-end was £1.5M.

As can be seen the profit declined during the period despite the forex tailwind. This reflects acquisition and integration costs, and additional investment in business development and marketing activities along with slower than expected underlying revenue growth. The professional fees in connection with the acquisition amounted to £57K and the net operating cost of the investment in Nicaragua totalled £216K. Measures have been taken to address the level of admin expenses in the second half of the year including the scale of investment in business development activities.

The central Scotland operations have recently been consolidated in Glasgow following the bringing together of the London operations in Croydon which has saved office rental costs of over £100K on an annual basis. Additional efficiencies will also accrue from the continuing automation of processes as well as a reduction in the scale of business development and marketing investment in the second half of the year. The introduction of a new online annuities platform in November 2016 is an example of the investment made in systems and has already directly led to new recurring GSS revenue being secured.

Revenue from the group’s GSS, employing paralegals, specialist formalities, search and docketing staff, and patent and TM admins continues to represent about 34% of total revenue with the remainder being produced by the attorney practice groups.

The EUIPO stats show that there was an increase in EU TM applications filed in 2016, up 4,600 to 135,000. During the year the group have therefore seen the sevenths consecutive year of growth with the number of applications filed setting a new record.

The full impact of the Brexit vote is not known and it is too early to evaluate with certainty the longer term consequences on the business and on the EUIP market more generally. Management remains confident however that the geographic spread of their activities and customer base puts them in a strong market position. After the UK’s exit from the EU the group will also continue to have both operations and subsidiaries in the bloc.

During the period the group acquired certain assets of MDB Capital and Patentvest based in Nacaragua for a total consideration of £1.8M. The business does not have any net assets so this entire total was recorded as goodwill. As expected the business made a loss in the first half but it is expected to be earnings neutral for the year as a whole and earnings enhancing thereafter.

Since September there has been a change in Government in the US, the UK’s exit from the EU is starting to take shape, the question of a second referendum on Scottish independence remains and volatility in forex markets have continued. We have also seen the first interest rate rise in the US and inflation beginning to rise on both sides of the Atlantic. The long-awaited introduction of the UPC may also finally take place in 2017, bringing with it new challenges and opportunities for patent attorneys in Europe. Trading in the second half of the year is expected to be in line with historic levels, and is in line with management’s revised expectations for 2017.

At the current share price the shares are trading on a PE ratio of 11.1 but this increases to 13.4 on the full year forecast. After the interim dividend was increased by 5.2% the shares are yielding 3% which grows to 3.1% on the full year forecast.

Overall then this has been a rather disappointing period for the group. Profit was down, net tangible assets declined and the operating cash flow fell with no free cash being generated after the acquisition. The acquired business has been a drag on results in the first half which should be negated in H2 but the flat underlying revenues (at constant currency) is more of a concern. With a PE of 13.4 and yield of 3.1% the valuation is probably about right given the uncertainty.

On the 6th April the group released an update covering trading in Q3. Revenue increased by 6% to £11.3M and the underlying trading result was much improved on the first half performance and ahead of revised internal forecasts for the period. This seems positive if the momentum can be kept going.

On the 3rd July the group released a trading update covering 2017. Total revenues in the second half were £22.8M, representing a 5% increase on the equivalent period last year. Trading for the second half has been in line with expectations and represents a significant improvement on the first half.