N Brown has now released their interim results for the year ending 2018.

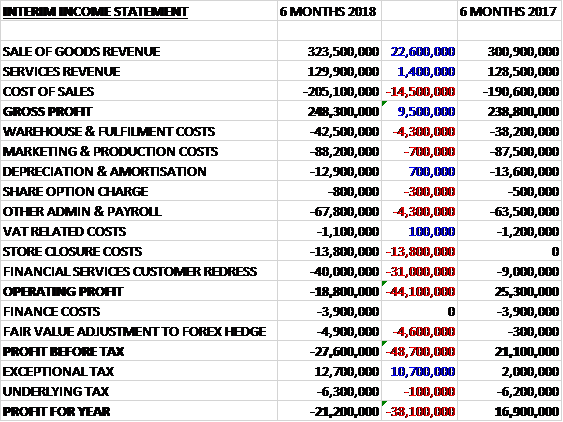

Revenues increased by £24M and with cost of sales up only £14.5M the gross profit grew by £9.5M. Warehouse and fulfilment costs increased by £4.3M and marketing and production costs rose by £700K, although this was offset by a £700K reduction in depreciation and amortisation, although this is expected to rise in H2. Other admin and payroll costs increased by £4.6M, partially due to the double running IT costs and further recruitment. There were also two large non-underlying costs, with a £13.8M store closure charge and a £31M growth in financial services customer redress costs. This all meant that the group saw a £44.1M swing to an operating loss. We also see a £4.6M increase in losses related to the forex hedge but these costs have given rise to a tax receipt, which was up £10.6M. This all meant that the loss for the period was £21.2M, a detrimental movement of £38.1M year on year.

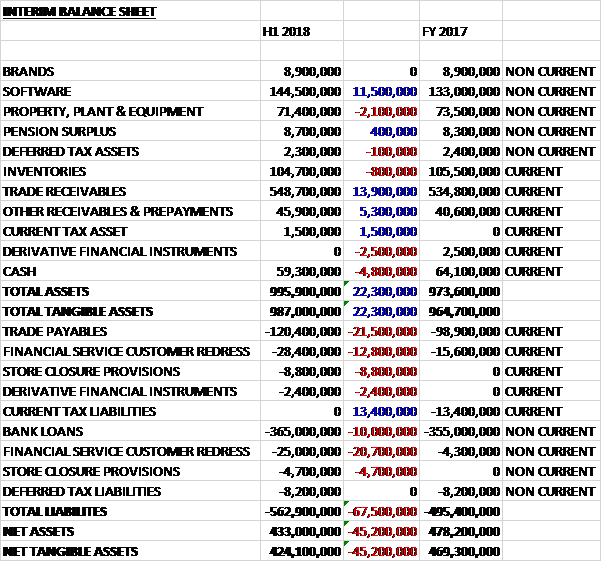

When compared to the end point of last year, total assets increased by £22.3M, driven by a £13.9M growth in trade receivables, an £11.5M increase in software and a £5.3M growth in other receivables, partially offset by a £4.8M fall in cash, a £2.5M decrease in derivative financial assets and a £2.1M decline in property, plant and equipment. Total liabilities also increased as a £13.4M fall in current tax liabilities was more than offset by a £21.5M growth in trade receivables, a £33.5M increase in financial service customer redress, a £10M increase in bank loans and a £13.5M increase in store closure provisions. The end result was a net tangible asset level of £424.1M, a decline of £45.2M over the past six months.

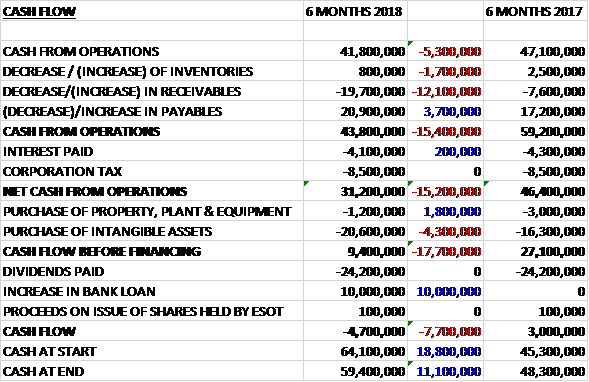

Before movements in working capital, cash profits declined by £5.3M to £41.8M. There was a small cash inflow from working capital but this was lower than last time and the net cash from operations was £31.2M, a decline of £15.2M year on year. The group spent £20.6M on intangible assets and £1.2M on property, plant and equipment to give a free cash flow of £9.4M. This didn’t come close to covering the dividends of £24.2M so the group took out £10M of new loans to give a cash outflow for the period of £4.7M and a cash level of £59.4M at the period-end.

JD Williams revenue was £81.1M, an increase of £5.3M year on year. Within this the JD Williams brand was up 12% and Fifty Plus was down 5.2% as expected. The migration of Fifty Plus is now complete. For the new Autumn Winter season they have refreshed the JD Williams brand proposition, launching JD Williams “The Lifestore”.

Simple Be revenue was £64.5M, a growth of £11.2M when compared to the first half of last year where the group made significant ladieswear market share gains against what remains a subdued consumer backdrop, The We Are Curves marketing campaign really seems to be resonating and gaining traction.

Jacamo revenue was £33.5M, an increase of £2.1M when compared to the first half of 2017. Their delivery subscription launched in February and has been successful with a double digit increase in both order frequency and net sales per customer. They will be extending a delivery subscription to other brands in the future. They also teamed up with Tom Morgan from the Undateables to promote their own-brand summer range.

Traditional segment revenues were £68.1M, a growth of £2.9M year on year as actions taken to address performance worked well.

Secondary brand revenue was £76.3M, an increase of £1.1M when compared to the first half of last year. Within this, Fashion world and Marisota both achieved good performances but Figleaves saw a revenue decline as the new management team restructured the business and optimised their marketing approach. High and Mighty revenue declined as they reduced marketing spend ahead of the new site going live.

US revenue was £8.1M, an increase of 6% year on year but down 4.4% at constant currency. The group stepped up their marketing investment towards the end of the period in order to drive new customer recruitment. Ireland delivered revenues of £8.5M, up 17% or 7.4% at constant currency.

Overall, revenue from the store estate was £10.6M, a decline of £900K due to the closure of five dual fascia Simply Be and Jacamo stores as a result of weak footfall and significant future business rate increases. These stores contributed £5M revenue and a loss of £2M in 2017.

Within the 1.1% increase in finance revenues, interest payments grew low single digits and non-interest lines were down double-digits. The improvement in the quality of the loan book was reflected in the gross margin performance, which was up 150bps. They had an encouraging performance recruiting new credit customers who rolled a balance, with an increase of 13% compared to the first half of 2017. This was driven by both the good product revenue performance in the new half and encouraging early results from the trial offering a lower APR for qualifying new customers. This trial continues ahead of the rollout of full variable APR functionality in 2018.

The new IT platform is now live on the High and Mighty and US sites, which includes a new Financial Services system on the High and Mighty site. The programme has now been substantially scaled down, reducing costs, and the in-house IT change team are now delivering enhanced functionality through fortnightly releases. The approach going forward will be to prioritise the developments that deliver the highest returns such as Global Ship Anywhere and Mobile Apps. The timescale for migrating other brands onto the new platform is expected to start in Q2 2018.

There are a number of future growth levers identified by the group. They are looking to increase the number of third-party brands on their websites and similarly are looking to sell capsule ranges of their own products on other retailers’ sites. In addition, they are looking to international expansion with the US being the first priority.

The most recent customer satisfaction score of 83.7% was lower than previously, although ahead of the sector average. The decline was driven by a fire at a delivery partner’s distribution centre which caused significant delivery problems for a small group of customers.

As can be seen there are two large exceptional costs incurred during the period. The group has identified flaws in certain insurance products which were provided by a third party insurance underwriter and sold by the group to its customers between 2006 and 2014. Following an assessment of the cost of potential customer redress, an exceptional charge of £40M was recognised during the period.

Also, during the period five loss making retail stores were closed which has resulted in a non-recurring cost of £13.8M in respect of asset write-offs, onerous lease provisions and other related store closure costs.

In addition there are a number of tax disputes ongoing. They have provided for a total of £5.4M in respect of future payments expected to be made in settlement of some historical tax positions. In addition, they continue to be in discussions with HMRC in relation to the VAT consequences of the allocation of marketing costs between the retail and credit businesses. At this stage it is not possible to determine how the matter will be resolved. An unfavourable settlement of these cases could result in a charge to the income statement of up to £46.8M and a cash payment to HMRC of up to £22.7M but a favourable settlement would result in a repayment of tax of up to £53.1M and an associated credit to the income statement of £29M so this could go either way!

Going forward, at this early stage in the second half, current trading is on track with the plan. A number of changes have been made to the guidance for the full year. The range for product gross margin has been reduced from -120bps – -20bps to 120bps – -70bps whereas financial services gross margin has increased from 0 – 100bps to 100 – 200bps. Group operating costs are now expected to be up 4.5% to 5.5% as opposed to 3.5% to 5.5%. Net debts has been increased from £300M – £320M to £325M – £335M reflecting the increased cash flow impacts of exceptional costs and the growth of the customer loan book. There are also exceptional costs of an additional £2M in H2 as a result of the ongoing tax dispute with HMRC.

At the current share price the shares are trading on a PE ratio of 17.9 which falls to 12.6 on the full year consensus forecast. After the interim dividend was kept the same the shares are yielding 5.1% which is forecasted to remain the same for the year as a whole. Net debt at the period-end stood at £305.7M compared to £286.7M at the end of the first half of last year.

Overall this has been a rather mixed period for the group. They swung to a loss but if we ignore the forex hedging losses, the store closure costs and financial service customer redress, profits would have been broadly flat. Net assets declined, however, as did the operating cash flow and although there was some free cash being generated, this did not come close to covering the dividends.

Core trading at the brands actually looks pretty good, particularly at Simply Be but the group is beset by issues. The financial customer redress is looking more and more expensive, the closure of the loss making stores should benefit the group in the long term, but are a drag in the short term and the dispute with HM customs is rumbling on and could be a real issue going forward. I just think the uncertainties are a bit much here and not adequately covered by the forward PE of 12.6 and yield of 5.1%, which is a shame.

On the 23rd January the group released a trading statement covering Q3. Group revenues increased by 3.2% and the full year profit expectation is unchanged. Simply Be performed well, up nearly 15%, with Jacamo up 4.6%, supported by a strong Christmas campaign and JD Williams increasing by 3%. Secondary brands were down 8.4% and the traditional segment grew by 3.9%.

The relaunch of JD Williams was a success with new customers up 12% and positive reactions from existing customers. This season, Fifty Plus brand customers have received the JD Williams marketing programme which has had mixed success due to the more traditional fashion preferences of some of these customers. This has impacted overall active customer metrics and ladieswear performance which saw an increase of just 0.7%. Actions are being taken to address this and the board are confident in receiving improving response rates from this customer group going forward.

Within Secondary brands, the largest brand, Fashion World, was down high single digits as they diverted marketing investment into their Power Brands. Figleaves revenue was down as expected, with the brand part way through its turnaround led by its new management team. The growth in the traditional segment was driven by the Ambrose Wilson brand, continuing the positive trend reported in the first half.

The US business moved back into positive growth in line with plans, with revenue up 19%. The new marketing strategy, including strong influencer marketing, is working well and they expect performance to continue to accelerate. They are on track to go live with Global Ship Anywhere by the end of the year, which further underpins future international growth.

Financial Services revenue was up 4.5%. Interest revenue was up high single digits whilst non-interest lines were down as planned. They delivered a further improvement in the quality of the customer loan book and this is reflected in their upgraded gross margin guidance. The loan book continues to show healthy growth.

Going forward, the product gross margin guidance for 2018 has fallen considerably, down from -70bps – 120bps to -225bps to -250bps. This is predominantly due to higher promotional activity. Financial services gross margin is expected to improve by +500bps to +550bps compared to +100bps to 200bps previously. This is a result of a further improvement in the quality of the customer loan book, together with several initiatives improving their customer proposition launched during the year. Group operating costs are now +4% to +4.5% compared to +4.5% to +5% previously and net debt is expected to be around £350M compared to £325M to £335M previously, due to the growth in the loan book

Overall I think it is a bit sneaky to paint a picture of growth in revenue and then just mention in passing that this was achieved through higher promotional activity hence the lower margins. Performance is expected to remain as was overall, however, so the fall in the share price might be an opportunity although I do note that the forecasts for 2019 have been slashed so perhaps I should hold off!

On the 19th February the group announced that the new chairman, Matthew Davis, purchased 10K shares at a value of £19.3K.