Newmark Security has now released their final results for the year ended 2017

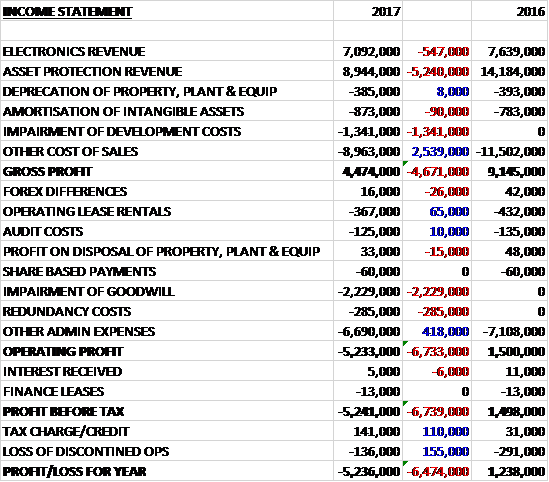

Revenues fell when compared to last year due to a £5.2M decline in asset protection revenue and a £547K decrease in electronics revenue. There was a £1.3M impairment of development costs but other cost of sales decreased by £2.5M which meant that the gross profit was £4.7M lower. We also see a £2.2M impairment of goodwill and redundancy costs of £285K, although other admin expenses decreased by £418K which meant that the operating loss saw a detrimental movement of £6.7M. Finance costs remained broadly the same but the tax credit increased by £110K and the loss from discontinued operations decreased by £136K. All of this meant that the loss for the year came in at £5.2M, a detrimental movement of £6.5M year on year.

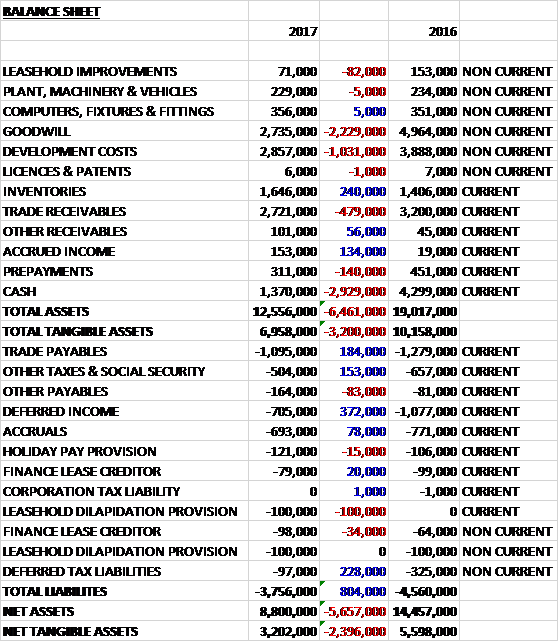

When compared to the end point of last year, total assets declined by £6.5M driven by a £2.9M decrease in cash, a £2.2M impairment of goodwill, a £1M impairment of development costs and a £479K fall in trade receivables. Total liabilities also declined, mainly due to a £228K fall in deferred tax liabilities, a £372K decline in deferred income due to lower levels of advance payments from customers and a £184K decrease in trade payables. The end result was a net tangible asset level of £3.2M, a decline of £2.4M year on year.

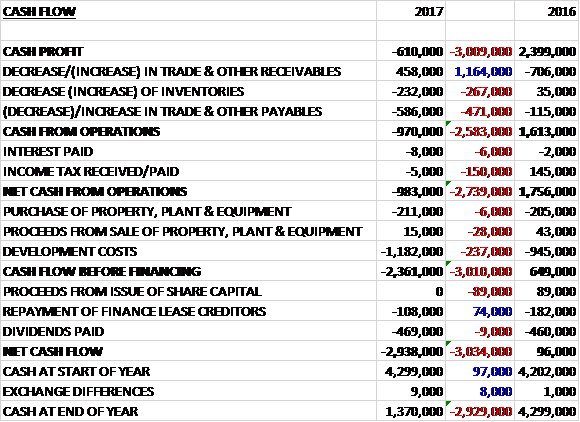

Before movements in working capital, the group saw a £3M swing to tax losses of £610K. There was a small cash outflow from working capital but this was less than last time. There was a £150K fall in tax income, however, which meant that the net cash outflow from operations was £983K, a detrimental movement of £2.7M year on year. The group then spent £1.2M on development costs and £211K on property, plant and equipment to give a cash outflow of £2.4M before financing. They also paid out £469K in dividend and £108K on finance leases to leave a cash outflow for the year of £2.9M and a cash level of £1.4M at the year-end.

Although the opportunity pipeline has grown, the conversion into sales has been slower than expected. The continuing economic uncertainty has affected customer spending plans with proposed programmes being severely delayed or cancelled.

Excluding impairments, the loss for the Electronic division was £708K, a deterioration of £547K year on year. Access Control revenues declined by nearly 13%. This was a very difficult trading period for the business as the group experienced reductions in revenues in its legacy access control platform, Janus, while revenue from its current Sateon offering was affected by the delayed release of the most recent variants. Due to Microsoft and Intel migrating away from platforms and operating systems that support 16-bit applications such as Janus, the revenues from that product line continued to decline in line with expectations.

Significant investment was made during the year and the Sateon offering was bolstered by the launch of new hardware and software, released in the second half of the year under review as Sateon Advance. While revenue for this variant was slower to materialise than original expectations due to the delayed product release, revenues in the Sateon range as a whole increased by 22% compared to the previous year to £2M. Early revenues and margin from the revised portfolio have been softer than earlier products due to their penetration pricing strategy.

The revenues from the Hong Kong operation unfortunately fell well short of expectations and as this position could not be predicted to significantly improve, the decision was taken to withdraw from the country. This operation incurred an operating loss of £225K in the year which has therefore now been eliminated as a cost in future years.

The group has recently entered into a technology agreement with US-based UniKey Technologies whose patented platform provides a “frictionless at door experience” for the end user. It is anticipated that Grosvenor’s first products incorporating the technology will be seen later in the current year.

Revenues for Workforce Management were similar to the previous year. The natural slowdown of the rollout across the estate of one of the world’s largest apparel retailers negated growth in some new and existing channel partners. Development was focused on the GT-10 employee terminal, launched as a developer kit towards the end of H1. It has an Android based operating platform and negotiations have started with several potential major WFM software providers in the US and Europe who have chosen to invest in creating their own software for the GT-10. It is expected to enter mass production during the first half of this year.

Negotiations continued with some large software vendors with a view to supplying them with variants of the group’s time and attendance terminals. In North America, business development activities increased to leverage the potential that exists for growing WFM revenues as it is felt that the US market remains the region of greatest growth opportunity for both the existing IT series terminals and the GT-10.

Excluding impairments, the profit for the Asset Protection division was £130K, a deterioration of £2.7M when compared to last year.

Revenue in Asset Protection (Safetell) decreased by 37%, partly as a result of the reduced contribution from time delay cash handling equipment sales to the Post Office. Although the business received orders from various long-term customers in retail finance, petrol and food retailing sectors, reduced sales were experienced in the lead up to and after the Brexit vote as many customers put plans on hold. This trend continued with budget cuts in all sectors. The fall in the value of Sterling against the Euro resulted in the increased cost of imported products which reduced margins further. The downturn in orders resulted in a reorganisation within the business which generated cost savings, however.

During the year, new products were developed and certified to UK security standards with the focus on providing counter terror security equipment for staff and customer protection. A distribution agreement was entered into with Gunnebo UK to distribute their Security Doors for Partitioning range within the UK. This enables the business to enter new market sectors. A fixed price supply contract with a leading financial institution entered its third and final year and margins on this contract were reduced due to imported component prices related to the fall in value of Sterling.

Service division revenue was 11% lower than last year. Sales have been challenging for the division as a result of the continuing branch closures that have occurred in the banking sector. Pneumatic upgrades of rising screen systems now generate more than 10% of the total service revenue. The new TC105 control panel used on the rising screen was introduced to the market and installed at many sites. This has proved very reliable and will replace the outdated Surefire control panel going forward.

The group conducted a review of the value of product development costs that had been capitalised previously. They have historically amortised IP-rich development costs over a seven-year period and therefore many assets reviewed were several years old. With the launch of Sateon Advance and a reduction in market demand for older products that is has replaced, a write-off of £1.3M on certain access control development costs was made. Development costs continue to be capitalised in accordance with the accounting policy. This is important because it seems to me that either too many development costs are being capitalised or the amortisation period is too long. This means that the group is likely overstating their profit position.

Within the access control business, although many end users have already migrated from Janus to Sateon, there are a number of large customers that are yet to make this transition. The board therefore believe that the opportunity exists for this to positively impact Sateon revenues in the current year. Going forward, the board expect continued growth in revenue from their new Sateon Advance access control system and counter terrorism products but in view of the ongoing economic uncertainty, they expect this will be a difficult trading year.

The group is loss-making so PE ratios are not going to tell us much. Also, there is no dividend being proposed this year and I can find no forecasts for next year. At the year-end the group had a net cash position of £1.4M compared to £4.3M at the end of last year.

On the 13th November the group announced that it had entered into a new ongoing supply agreement with WorkForce Software. The group will supply WorkForce globally, through sales and leasing, with their IT51 Linux based workforce management terminal with will enable their customers to improve business efficiency and facilitate greater employee satisfaction through accurate time tracking. In addition, they will provide WorkForce with a range of remote support tools on an “as a service” basis.

On the 27th November the group announced that it had won a new contract with a European workforce management provider. Under the contract they will provide a Linux-based OEM variant of their GT-10 workforce management terminal in addition to a range of cloud based support services on a SaaS basis. They will also provide an OEM variant of their Sateon Advance Access Hardware to work with their customer’s existing platform.

The customer funded development work in the contract, itself worth £190K, is being conducted this year and revenues are expected to come on stream in Q2 2018 with the contract value being around €3M over a five year period. Apparently the customer preferred the industrial design of their GT-10 Android-based terminal but recognised the advantages of the hosted SaaS services they provide in their Linux based terminal so they are developing a hybrid solution specific to their requirements.

Overall then, this set of results has been a bit of a disaster. The group is now loss making even when the impairments are ignored, net assets declined and the operating cash outflow deteriorated even further. The Electronic division suffered from delays to Sateon, and the Hong Kong underperformance while the deterioration in the asset protection division was even greater with lower Post Office sales and other customers delaying and cancelling decisions due to Brexit. In addition the service division is suffering due to Bank closures. All in all, these don’t look very investable at the moment and I’m steering clear.