Sainsbury have now released their interim results for the year ending 2014.

Revenues for the half year increased by an impressive £524M year on year. Obviously cost of sales also increased but at a slower rate so gross profit was up by £62M. Admin expenses were actually slightly lower than last year but a lower profit on property sales was not enough to cause a reduction in operating profit, with it being £33M up. Finance costs were not that different from last year and a slightly higher tax bill meant that the profit for the period was £29M higher than last year at £340M. There were a number of one off items that affected profits. These included a £158M service credit due to the closure of the pension scheme to future accrual; an impairment of £92M for write downs where the group no longer intend to build supermarkets following a review; costs of £17M in relation to the ongoing purchase of the bank and cost of £13M as a result of a provision for a commercial item (this might be related to the legal challenge with Tesco’s own brand products. In the second half the group expects one-off costs including £11M of costs due to the closure of the defined benefit pension scheme, £25M for the bank to transfer to a new platform and an unknown amount of one off costs relating to the purchase of the bank.

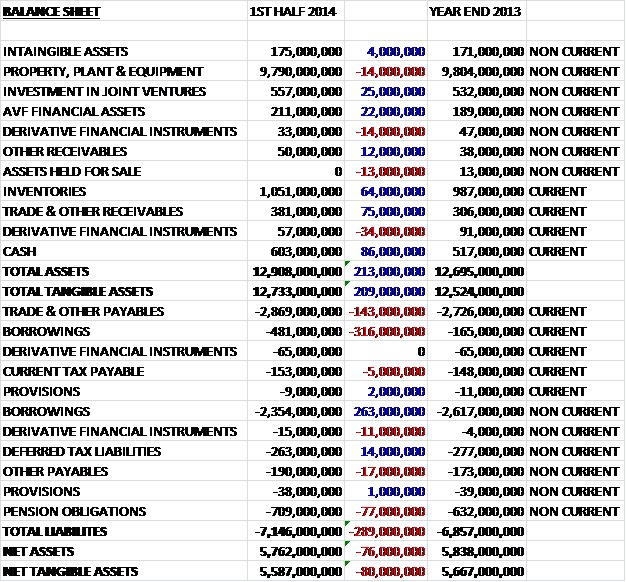

Overall total assets at the half year point were £213M higher than at the end of last year. There were not actually that many huge changes but some of the largest increases were seen under trade & receivables (up £75M); cash (up £86M) and inventories, up £75M. These were counteracted by a number of small falls with the largest being a £48M reduction in the value of derivative financial assets. Total liabilities, however, were also higher than at the end of last year with a few big increases – trade and payables increased by more than receivables, up £143M, pension obligations increased by £77M and total borrowings were up by £53M. There were no large falls in liabilities so total liabilities increased by £289M which gave a fall in net tangible assets of £80M to £5.587M. This is rather disappointing but I try not to get too excited about half year balance sheets as results can sometimes be weighted to the second half of the year.

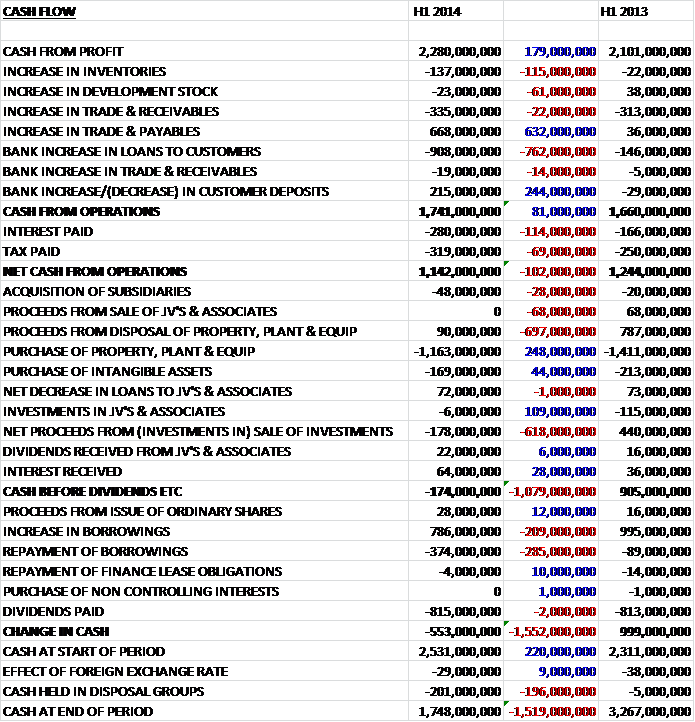

Cash profits were slightly higher than during the same period of last year before a big increase in payables was almost exactly counteracted by increases in receivables and inventories. The movements were more favourable than last year and cash from operations was £58M better than last year at £695M. A higher tax payment took its toll on net operating cash, however, and this was up by a more modest £36M at £566M. Once again, this was almost entirely eaten up by capital expenditure which was £152M lower at £457M before £143M received from store sale and leaseback operations meant that cash before financing was £243M, £189M up from last time. There was then a net £87M in new borrowings counteracted by £225M of dividend payment but the cash change in at the end of the half was a decent £93M. When it is considered that store sales accounted for £143M and new borrowings £87M, this is not so swish.

The joint ventures are not making a great deal of money with underlying profits at the bank £12M, exactly the same as last year and the same is the case with the property joint venture with underlying profits of £8M also the same as in the first half of last year. After the effects of one off items at the bank the actual profits were only £3M in the first half.

For the last few years there has been an ongoing legal case between HM customs and Amina, the company that administers the Nectar scheme regarding the accounting for VAT on the redemption of Nectar points in store. In June the court ruled in favour of Amina thereby potentially enabling Sainsbury to recover some historic VAT payments and the group are currently in discussion with HM customs regarding this.

Once again Sainsbury recorded quarterly sales growth, the 35th consecutive quarter that they have done so, driven by strong performances in own-brand, non-food, convenience and online food along with favourable summer weather. Total sales during the half year excluding fuel were up 4% with a 1.4% increase in like for like sales (all the more impressive when it is considered that the comparison last year contains the Olympics and Queen’s diamond jubilee). Like for like sales growth in the second half is expected to be somewhat lower due to a strong comparable last year. Underlying profit was even more impressive, up by 7%. Non-food and the own brand food are increasing sales at over twice the rate of branded groceries with the premium own brand showing double digit growth. The basics range is being relaunched after it recorded a marginal sales decline during the period which should help sales there. The convenience business is providing growth of 20% year on year with two new stores opening a week. The other driver of growth is online groceries which increased sales at over 15% and now turns over more than £1B and the group have been awarded online retailer of the year – I am not sure how much margin there is in the online grocery business though.

As mentioned above the profits at the bank were flat but the group is intending to build the bank into a high trust and ethical bank. The timing is pretty good as there is likely to be a gap in the market following the well-publicised problems at the Co-Op bank. A new pet insurance product was launched during the period and Travel Money increased sales by 20% over the same period of last year. The group are on track to take on full ownership of the bank in early 2014 with the transition expected to take three years. There will clearly be some associated costs involved here but hopefully long term this will be a good move for the group.

There are a number of new areas that Sainsbury is moving into. They are building a new mobile network in a joint venture with Vodafone offering customers double Nectar points on their grocery and fuel spend in Sainsbury as a sweetener. A video on demand service was launched in April that will shortly give customers the ability to buy or rent films via a download service. These two new joint ventures made a £2M loss due to start-up costs. The other main new business is health services for customers with in store pharmacies, GP offices and dental surgeries. In addition, the group also opened their fourth outpatient pharmacy at King’s College Hospital with more to come over the next few years.

There are continued attempts to improve operational efficiency with a new warehouse management system being rolled out that increased productivity by nearly 10% and improved pick accuracy. The group have also added a large clothing facility near Bedford and a dedicated convenience store depot in South London to help that growing market.

The group has decided to take Tesco to court after the advertising standards authority failed to take the action Sainsbury were looking for regarding the fact that in the group’s view the price comparison between Tesco own brand and Sainsbury own brand was not fare due to it not being the same with regards to provenance and quality. I am not sure if Sainsbury are really looking to get anything out of this other than to draw attention to how ace Sainsbury own brand is!

So, revenues were up by about half a billion pounds and profits were up £29M in the period despite lower property profits. Net assets were down £76M on the end of last year which is almost exactly the amount by which the pension obligations increased with payables and loans also increasing. The cash income during the period was £93M which, although better than last year, was still a bit poor considering the group gained £143M of cash from store sales and there were new borrowings totalling £87M. It is clear that Sainsbury are diversifying into a number of different business and the purchase of the bank is a sign of intent, albeit one that will costs a bit in the short term. At £2.187B net debt was just £25M higher than at the year end point but this is expected to increase to £2.5B by the end of the year, partly due to the bank purchase. The interim dividend was increased by 0.2p to 5p which at the current share price represents an annual yield of 4.1% which is pretty decent given the lack of risk here. There is no doubt that Sainsbury has been the big winner in the race for market share but Tesco are making changes that put it in more direct competition from Sainsbury which is something to look out for. Overall I consider Sainsbury to be worth holding on to for now.

On 8th January the group released a statement covering the quarter to December. It was announced that total sales (excluding fuel) were up by 2.5% but like for like sales were only up 0.2% as weak trading in October and November was counteracted by a strong December and Christmas. Growth came from own branded products, with taste the difference sales up 10%; convenience sales, up 18% and online sales, up 10%. Non-food also grew quickly with Tableware up 25% and Gifting up 30%. The group sold more than 250,000 Christmas Jumpers! It was also another quarter of expansion with 6 new supermarkets, 4 extensions and 19 new convenience stores. Overall there is no denying that this is quite a disappointing update and Sainsbury only just continued its theme of consecutive quarters of like for like growth.

On 29th January, Sainsbury dropped the bombshell that long standing CEO Justin King had decided to step down in July this year. He will be replaced by the current Commercial Director, Mike Coupe. Mike was appointed commercial director in 2010 and was responsible for the trading, marketing, supply chain, IT and online. He has been a member of the board since 2004 when he joined as Trading Director. Prior to joining Sainsbury he was a board director of Big Food PLC and a Managing Director of Iceland food stores. Justin has waived his cash severance payment, which could potentially have been worth up to £1.7M. He had been CEO for the past ten years and is credited with turning round the fortunes of a company that was in pretty bad shape when he took over. It is undoubted that Sainsbury will be losing a very charismatic and capable CEO and I hope that Mike will be able to fill his shoes.

On 18th March, Sainsbury released an update covering Q4 trading. Like for like sales in the quarter were down 3.1%, the first quarterly fall for many years. The market is currently growing at its slowest rate since 2005, partly due to lower food inflation. Own branded products now account for 51% of sales, compared to 47% this time last year so the lower value of those would have affected sales. Q4 this year was also battling strong comparisons last year as Sainsbury received a boost as the horsemeat scandal hit some of its competitors. Also, the late fall of Easter and Mother’s Day, along with the terrible weather are also thought to have an effect. Sainsbury maintained market share at 17%.

General merchandise fared well, with sales of menswear up 23%. The other two growth areas were convenience, up 15% and online, up 6%, which is a bit of a slow down on recent numbers due patly to reduced marketing before the new website is launched next month. There is no doubt that the first fall in sales for many years is a big disappointment but I do feel that there were a number of one-off factors this quarter. It will be interesting to see how Q1 fares considering the timing of Easter. It is encouraging to see Sainsbury maintain market share but the share price has been hammered in recent weeks due to the announcement of Morisson’s that they will be lowering prices to compete with Lidl and Aldi. It seems that the two German discounters are not affecting the group in the same way that they have their competitors but if the other large UK supermarkets start reducing prices, this could have an adverse affect on Sainsbury. I felt the fall in share price was overdone and topped up some more shares but only time will tell if this was a wise decision…