Omega Diagnostics has now released its final results for the year ending 2015.

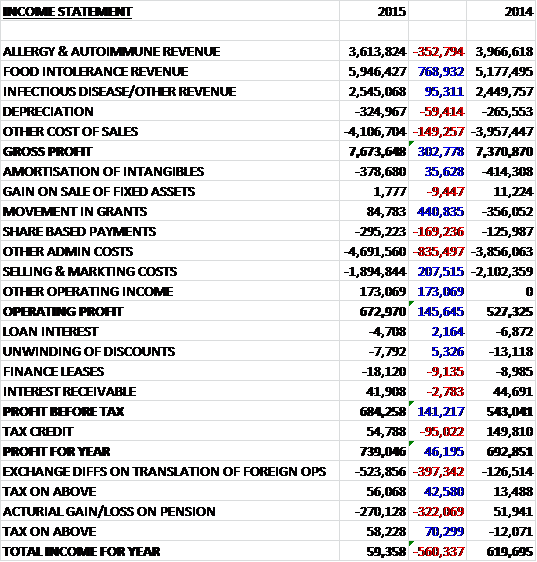

Overall revenues increased year on year as a £353K fall in allergy and autoimmune revenue was more than offset by a £769K increase in food intolerance revenue and a £95K growth in infectious disease revenue. Revenues were adversely affected by currency movements and would have been some £400K higher on a constant currency basis. Cost of sales also increased somewhat to give a gross profit some £303K ahead of last year. The amortisation charge fell year on year and the group also benefited from a £441K movement in grants, although this was offset by a £169K increase in share based payments and an £835K growth in other admin costs due to an increase in costs related to the Visitect CD4 device, a near full year charge for the manufacturing space in India and investment in regulatory staff.

Selling and marketing costs actually fell during the year and £173K worth of “other” operating income comprising of a £74K credit from the UNITAID grant, £54K from a Scottish enterprise grant awarded in 2012 as certain employment targets were met and £45K relating to compensation received from Lloyds bank for previous hedging products the group was required to take out to gain access to funding, meant that operating profit was £146K ahead. There was a £95K reduction in the tax credit, mainly as a result of movements on deferred tax from share based payments, to give a profit for the year of £739K, an increase of £46K when compared to 2014.

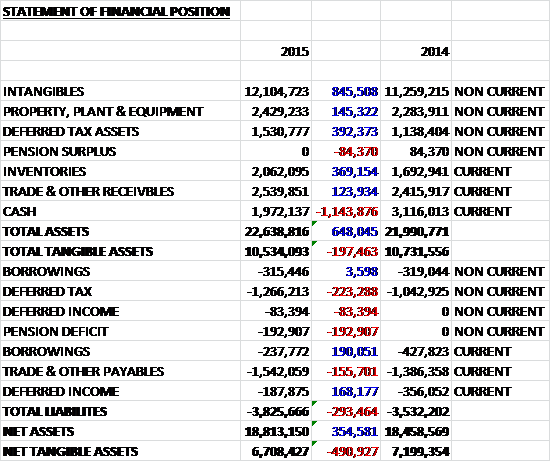

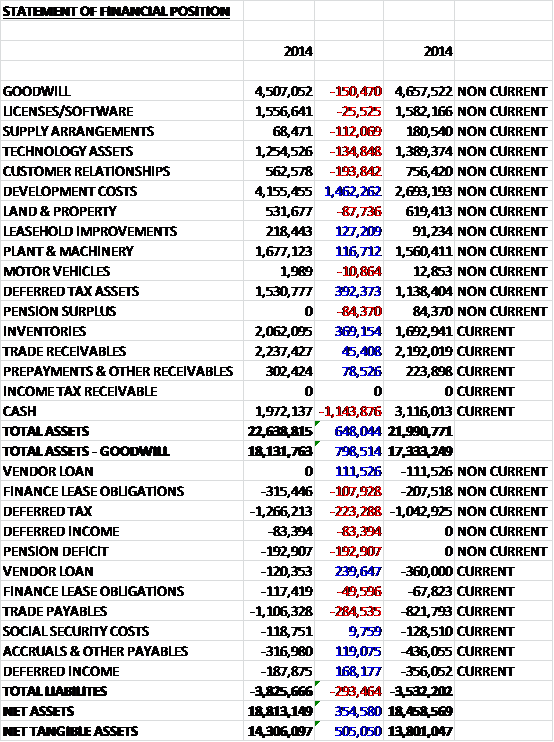

When compared to the end point of last year, total assets increased by £648K driven by an £846K growth in intangibles, a £392K increase in deferred tax assets, a £369K growth in inventories and a £145K increase in property, plant and equipment, partially offset by a £1.1M decline in cash. Liabilities also increased during the year as a £223K increase in deferred tax liabilities, a £193K increase in the pension deficit and a £156K growth in payables was partially offset by a £194K fall in borrowings and a £168K decline in deferred income. The end result is a £491K fall in net tangible assets to £6.7M.

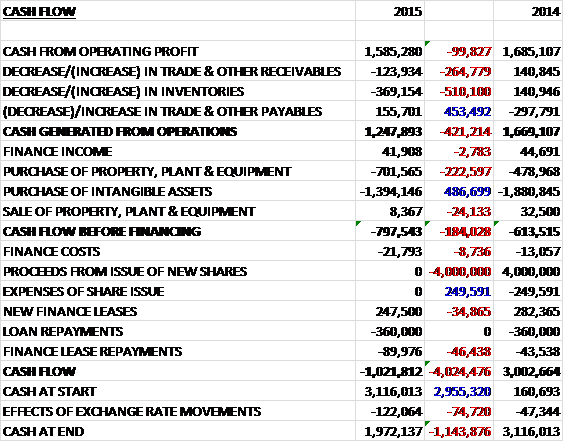

Before movements in working capital, cash profits fell by £100K to £1.6M. This was eroded by an increase in receivables and inventories, due to the intentional decision to lock in and hold key raw materials for the CD4 test (worth £300K) partially offset by a growth in payables to give a cash from operations of £1.2M, a £421K decline year on year. Unfortunately this did not cover £1.4M worth of intangible asset acquisition, probably related to development costs and certainly not cover the £702K in property, plant and equipment purchases so that before financing, the cash outflow stood at £798K, a £184K deterioration. We then see £360K of loan repayments and £90K in finance lease repayments, partially offset by £248K worth of new finance leases to give a cash outflow of £1M for the year and a cash pile at the year end of £2M (there is also a £1M overdraft facility). This is not too inspiring to be honest.

.Of the £700K worth of capital expenditure on fixed assets, the group spent £300K in Scotland on expanding the Visitect CD4 manufacturing assembly facility, in India £100K was paid on account to the contractor responsible for the fit out of the new manufacturing facility and £200K was invested in Genesis/CNS to ensure it keeps pace with the growth experienced in the food intolerance business.

Following a three batch validation in February the Visitect CD4 test underwent pilot studies in India and Kenya, the results from the Indian study showed acceptable performance whereas the results from Kenya were suboptimal. In order to determine the cause behind the Kenyan results, further batches were made which demonstrated unacceptable levels of batch to batch variability. At this point, the group brought the previously outsourced manufacturing process in-house and engaged with experts in lateral flow device development who were able to investigate the issues with the co-inventors.

During the second half of the year, the group manufactured the test using the same methods as developed by the Burnet institute. They have been able to make thousands of devices and have moved to a period of verification and validation, concentrating their efforts on overcoming the stability issue that became evident as described below. Once resolved, the group will restart the earlier field trials.

Before we get on to the operational performance, it should be noted that in the last few days it has been determined that that there is a stability issue with the Visitect CD4 final product that manifests after five weeks of storage at room temperature. The group are currently undertaking further investigation to determine a route cause. They will not put the product back into field evaluation until they have addressed the issue and the product meets the needs of the target market.

This year Food Intolerance sales increased by 15% to £5.95M. Sales of Food Detective grew by 23% during the year to £2.08M with impressive growth in Poland, Brazil and China. Total volumes achieved were just over 163,000 units compared to 106,000 units last year and excluding component sales to China, the average selling price per kit was £20.66, a reduction from the £22.55 last year reflecting promotional activities in Poland. Sales of the Genarrayt Foodprint reagents grew by 19% to £2.52M with strong performances in Spain, France, Canada and Brazil. Spain and France were the largest markets, exceeding half a million pounds of sales each.

The group also sold a further 18 instruments in the year, taking the cumulative number of installations up to 150 and excluding Spain (why?) revenue per instrument increased by 4% to £14,354 with the relatively low growth reflecting investments being made into newer Far Eastern markets. The CNS lab service achieved a modest increase of 3% in sales to £650K with 8,241 patient reports produced at an average price of £79.33 per report (down from £79.55). The profit before tax at the food intolerance division was £2.1M, an increase of £500K year on year.

Sales in the Allergy and Autoimmune division comprised of Allergy sales of £3.08M and sales of autoimmune products of £530K compared to £3.52M and £450K last year. The Allergy sales are derived from the Omega business in Germany which has experienced a reduction in sales due to continued reimbursement restriction which was exacerbated by the weakening Euro against Sterling. The loss before tax at the allergy and autoimmune division was £299K, an increase of £162K when compared to 2014. The strategy remains to focus on retaining customer relationships through training, service and education. The modest growth in the Autoimmune sales reverses a recent downward trend due to growth in the Middle East.

Steady progress has been made towards the commercial launch of the Allersys Allergy programme with 32 allergens having been optimised and showing equivalent performance to the market leader. With external site evaluations still to be concluded there is still some work ahead but there is confidence that when the platform is launched, it will be well accepted. The strategic aim remains to launch a panel of 40 allergens on the automated IDS/Allersys system followed by a programme of menu extensions to achieve a number two market position. During the year optimisation work was transferred from the external contractor to a newly recruited in-house team. In total there are six IDS instruments across two sites supporting the work programmes.

Following a successful pilot study in June comparing the performance of eight Allersys allergens with the predicate device, ThermoFisher’s ImmunoCAP system, and when the results were presented at the annual EAACI meeting they generated a lot of follow-on interest. They now have a fully validated in-house manufacturing system with finished kits for 27 allergens available on the shelf. All of these kits have recently begun external evaluations at sites in Spain and Italy and will provide performance data for the technical file needed to support CE marking. Commercialisation discussions continue, both with IDS in markets where it has a direct presence, and with their partners in other areas.

Infectious disease sales increased by 4% to £2.55M due in part to the recovery in business fortunes of a UK customer that experienced financial difficulties in the prior year and in part due to improved product mix in Africa and Asia mitigating some reductions in the Middle East. The loss before tax at the infectious disease division was £289K, an increase of £178K when compared to last year.

The production facility in India is taking shape and is expected to be complete within the next six months which will provide the group with a capacity of two million tests per annum in addition to the 2.5 million tests able to be produced in a single shift in the UK facility.

If it can be commercially produced to a satisfactory standard, the Visitect CD4 device is planned to be initially introduced and implemented in 13 countries in Sub Saharan Africa through working with major NGO networks. As part of the commercialisation process there are certain regulatory hurdles to overcome in addition to gaining the CE mark approval for the test itself. The group are already engaged with the WHO to gain prequalification for the test but the timescale for achieving this is likely to be in excess of one year. In the absence of WHO approval there is also the Expert Review for Diagnostics which aims to provide guidance to procurement agencies for diagnostic products that have not yet undergone assessment by WHO. The short term goal is to obtain ERPD approval for the product well in advance of WHO PQ which will allow the earliest procurement of the device.

The field trials of the Android smartphone app to record and transmit Visitect CD4 test results have also been delayed during the CD4 investigation phase but will be capable of being recommenced once the results from India and Kenya show that the test device itself works in the field. NGOs and global health organisations are apparently enthusiastic as the app/device combination offers a complete information solution from test site to management HQ. The group’s activities with the Groupe Speciale Mobile Association (GSMA) continues to attract attention from major players in Africa such as mining companies which operate across the continent and in areas which are remote and have poor healthcare facilities along with a high HIV burden.

Total investment in R&D was £1.81M, an increase of £200K year on year. Expenditure continues to be focused on the group’s two major strategic opportunities. Expenditure on the Allersys project increased to £980K from £930K with the marginal increase reflecting additional staff costs. Expenditure on the Visitect CD4 project increased from £430K to £480K as the group progressed and completed the internal investigation phase. A total of £1.5M of this expenditure was capitalised into intangible assets with a total of £3.1M now capitalised to date on the iSYS project and £1.1M on the CD4 project.

During the year it was announced that Colin King was to join the board as COO from the Elere group. In addition CEO Andrew Shepherd has been given responsibility for identifying new product opportunities in global health with a focus on achieving new product launches. It has become clear that the group needs to make some internal changes to the way they work after the disappointment with the CD4 product. All technical activity will ow fall under the control of the R&D director Dr. Edward Valente. They have also developed a new division, Global Health, reporting directly to the CEO which encompasses all aspects of the CD4 product roll-out and promotion along with assessment and development of new product opportunities. It also includes market development and promotional activities for the schistosomiasis and syphilis POC products. In January 205, Dr. Nigel Abraham was appointed as group Science Director for Food Intolerance. He joins from Genova Diagnostics where he was Scientific director and a board member.

Going forward the board foresee growth opportunities in Food Intolerance which will mitigate the ongoing pressures of reimbursement for the allergy business in Germany. At the current share price, the shares trade on a PE ratio of 27.1 which seems rather expensive and so far I have not seen any updated forecast for EPS going forward so I do not have a forward P/E ratio at this time.

Overall then, these annual results are all about the further setback with the Visitect CD4 device which is apparently unstable after five weeks in a room temperature environment which doesn’t inspire confidence for the African field where it will be deployed. From the restructuring being undertaken and the WHO hurdles that need to me met, it doesn’t sound as though this will be quick fix and for this reason I have decided to sell up and wait for another entry point further down the line. Operationally the food intolerance business is doing very well, increasing profitability year on year but the allergy and infectious disease business both became increasingly loss making in part due to adverse exchange movements and the continued reimbursement restrictions in Germany.

Understandably the market has reacted poorly to the further delay, what a shame.

Omega Diagnostics has now released their annual report with a bit more supporting detail.

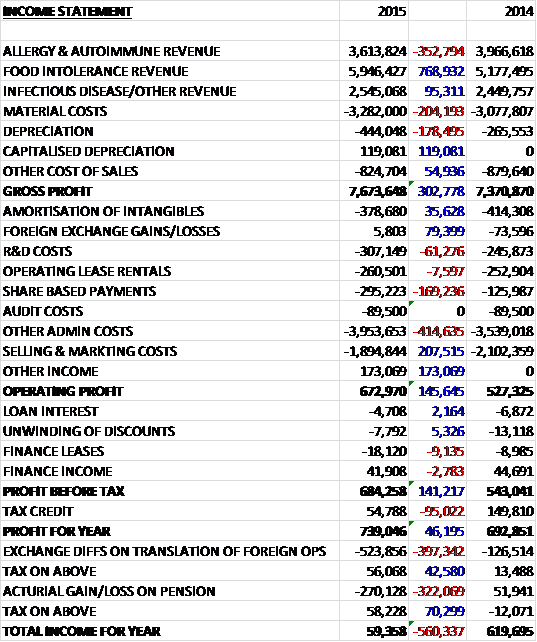

The only extra information of any interest here is the £204K increase in material costs and a £61K increase in R&D expenses, partially offset by a £79K favourable exchange rate movement.

As far as non-current assets are concerned in intangible assets we can see that a £1.5M increase in development costs was partially offset by smaller declines in the other intangibles. Most of the tangible fixed assets increased modestly and there was also a small growth in trade receivables and prepayments. In payables, the increase was driven by a £285K growth in trade payables.

There is an interesting part in the annual report where the group outlines prospects in various regions. In the Americas the group has achieved a growth of 79% in food intolerance products in Brazil and Canada and going forward there is expected to be continued growth in Latin America, an expansion of the strong food intolerance market position in Canada and they are exploring longer-term options for US entry, although the regulatory requirements are rather onerous. In Europe the business is slowly declining in Germany but food intolerance continues to grow from its strong base in Southern Europe. The group plan to introduce large allergen panel on Allergodip and grow export business out of Germany to mitigate the internal decline and continue to grow the food intolerance business.

In the Middle East and Africa region the group have launched Foodprint Arabia in Gulf countries with Food Detective also being launched in Saudi Arabia. There was also strong growth in Iran and Nigeria. Going forward the group are looking to continue the growth of food intolerance in the Gulf countries and reverse the declining trend in infectious diseases through Visitect. In Asia the group have continue their growth in India despite currency devaluation, experienced strong growth in China and found new food intolerance partners in Hong Kong and the Philippines. Going forward the group are looking to diversify the portfolio in India, focusing on tier two and three cities, implement the manufacturing facility in India to reduce production costs and continue growth in food intolerance in India, China and SE Asia.

We can also see that the group increased the value of outstanding operating leases by £439K to £1.7M and while this is not a particularly large amount, the increase is noticeable for a company of this size.

On the 30th September the group announced the grant of options to new COO Colin King. They have granted 1,200,000 options at an exercise price of 13p. Half of them can only be exercised when the share price has hit 50p or more on at least one occasion over the three year vesting period. The other half will be exercisable if the company’s adjusted EPS show a 10% cumulative growth rate over the three year period beginning April 2016.

I have been critical of director options in the past but this is an example of exactly how it should be done in my opinion. The targets look tough, which is great, and they are definitely in line with shareholder interests.

On the 26th October the group released a trading update covering the first half of the year. Turnover is expected to be £6.15M, 8% ahead of the first half of last year. An increase in gross profit has covered a rise in management costs so that pre-tax profit is expected to be similar to that achieved last time (£560K) and overall trading is in line with management expectations.

Within food intolerance, the group continue to see significant gains in business throughout the Americas and the Middle East plus a number of markets in Asia and the Far East. This is driven by increased use of both the Food Detective and the microarray-based Foodprint. The allergy division continues to be affected by the results for the German business where revenue was impacted by a further weakening of the Euro and the influence of reimbursement budget caps resulting in a slow decline in testing activity within the doctor’s office segment. The infections disease segment has produced encouraging results, helped in part by the recovery of the stained bacterial suspension product line in the UK and growth across the product range in some African countries.

They have continued to make good progress in the period with the allergy development programme. Since the last update, a further four allergens have been optimised, taking the total number whose performance matches the market leading product to 36. Of these, 26 have now completed claim support work and a further six are just about to enter the claim support phase. The in-house team will focus on delivering a menu expansion beyond the initial launch panel of 40 allergens.

An external evaluation in Spain completed in July. The principle investigator selected ten allergens to test over 400 patient samples. A strong positive linear relationship between the Allersys assay and the market leading product was reported and it was concluded that the reagents on the IDS iSYS analyser provided a technology which was quick and easy to use for allergy testing in the lab. Over 500 samples have been collected for the planned Italian evaluation which is due to start at the end of the month. Further evaluations will also be conducted in Germany and France, each with over 300 samples, with an expected start date towards the end of the year.

With regards CD4, since the last update the group have concentrated efforts to resolve a stability issue which manifested after five weeks storage at ambient temperature. They have recently discovered an ambient temperature effect which manifests as a change in test line signal, with no corresponding change in reference line signal. They have identified the step responsible for this temperature effect and their immediate focus now is to complete the testing needed to determine which component from this step causes it. Once it is identified and replaced or adjusted, the verification and validation process will re-commence. They remain confident of resolving this, although the ultimate timing remains uncertain at this stage.

The company has recently completed the fit-out of 20,000 sq ft of lab and manufacturing space in Pune, India. As well as providing a second manufacturing site for CD4, the facility, which is being installed with manufacturing equipment which is generic for most lateral flow rapid tests, will provide a low cost manufacturing base for a broader range of infectious disease test. They have selected a range of Malaria tests on which to work as soon as the equipment has completed validation.

Overall then, the slow progress on CD4 is disappointing and the German business is continuing to struggle but elsewhere, progress seems rather good with the new allergy tests coming along nicely. In all, I have decided to re-enter here but I am aware that until the problem with CD4 is sorted (if it is), this is quite a speculative investment.