RM has now released its interim results for the year ending 2015.

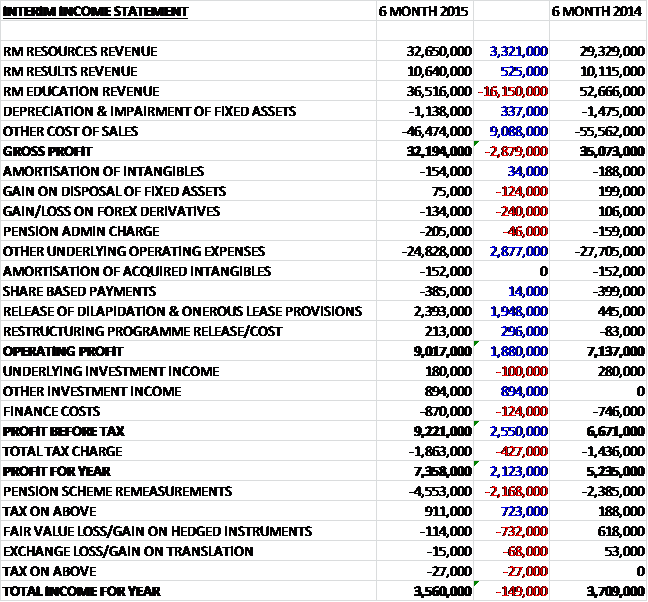

Overall revenues fell year on year as a £3.3M increase in Resources revenue and a £525K growth in Results revenue was more than offset by a £16.2M decline in Education revenue. Cost of sales also fell to give a gross profit some £2.9M lower than in the first half of last year. Underlying admin costs fell year on year but there was a smaller gain on the disposal of property, plant and equipment, there was a loss on foreign exchange derivatives and the pension charge was slightly higher. The group then benefited from a £1.9M increase in the release of onerous lease provisions as the group managed to sublease its old premises to South Oxon District council for three years, there was also a £213K restructuring release to give an operating profit £1.9M higher than last time. After an £894K “other” investment income relating to the sale of the group’s interests in Newham Learning Partnership and a £427K increase in tax the profit for the half year stood at £7.4M, an increase of £2.1M although this does seem to have been driven by the release of the provision and restructuring gain.

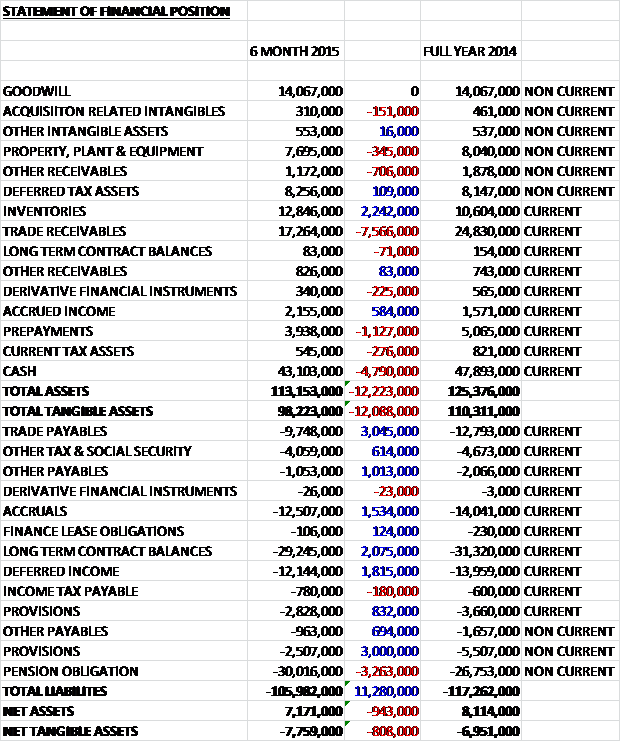

When compared to the end point of last year, total assets fell by £12.2M driven by a £7.6M fall in trade receivables, a £4.8M decline in cash and a £1.1M decrease in prepayments, partially offset by a £2.2M increase in the value of inventories. Liabilities also decreased during the period as a £3M fall in trade payables, a £3.8M decline in provisions, a £1.8M fall in deferred income, a £1.7M fall in other payables and a £1.5M decrease in accruals was only partially offset by a further £3.3M growth in pension obligations. The end result is an £808K fall in net tangible assets to a negative £7.8M.

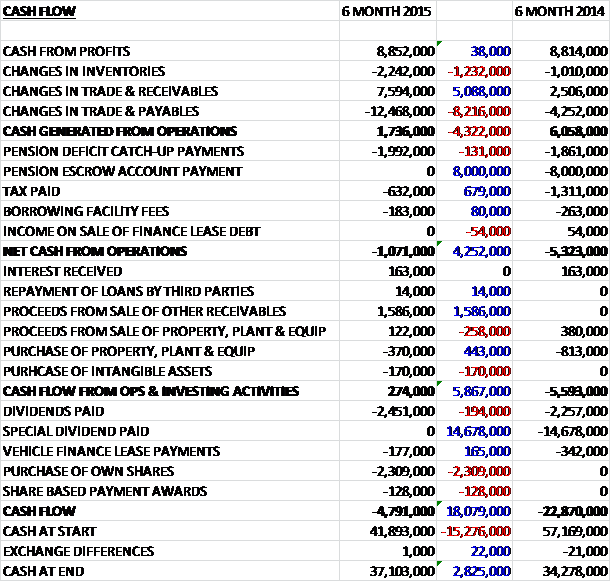

Before movements in working capital cash profits were fairly flat, increasing by just £38K to £8.9M. This was eroded by a large decline in payables, however, to give an operating cash flow of £1.7M, a fall of £4.3M year on year. This was not enough to cover the £2M pension deficit payments, however, and after tax is taken off, there was a net cash outflow of £1.1M at the operating level. There was fairly modest capital expenditure – just £370K on tangibles and £170K on intangibles and the group benefited from £1.6M worth of proceeds from the sale of other receivables relating to the sale of the group’s interests in Newham Learning Partnership. The group then spent £2.5M on dividends and £2.3M on its own share purchases which meant that there was a £5M cash outflow for the half year to give a cash level of £37.1M at the period end.

The operating profit at the RM Resources division was £4.5M, an increase of £700K year on year. TTS represents over 90% of the segment’s revenue and is a value added distribution business offering a wide range of curriculum products and materials to schools. The direct catalogue and online revenue rose by 13% benefiting from strong curriculum focused propositions. International revenue grew 17% and represented 13% of the businesses’ sales in the period. Adjusted operating margins increased from 13.1% to 13.9%.

The operating profit at the RM Results division was £1.6M, a decline of £400K when compared the first half of last year despite a 5% increase in revenues. This decline occurred because the comparison last year was flattered by the cumulative impact of an improvement in the forecast lifetime profitability on an estimated long-term contract. In February the division signed a new three year contract to provide the education charity AQA with e-marketing services alongside DRS, their existing supplier. The division has also been selected as preferred supplier to provide e-assessment services to a world leading professional membership organisation, ICAEW, an existing customer for e-marking.

The operating profit at the RM Education division was £2.6M, a decline of £700K year on year although due to the decision to discontinue the sale of personal computing devices and operating margins improved from 6.4% to 7%. This division includes services subject to long-term project accounting and like last year, profits were positively affected by good operational performance and cost control in completing BSF contracts. Good progress was made in the period with respect to pursuing the priority areas in software and services. Positive engagement with major Multi Academy Trusts has resulted in a wide ranging framework agreement being signed with one trust and with the division being awarded preferred bidder status on another. The vast majority of maintained primary schools in Derbyshire have contracted to transfer to RM Integris, the division’s cloud-based School Management Systems platform and a new internet connectivity contract was signed with West Berkshire.

The pension scheme is continuing to be an issue for the group. The deficit increased somewhat year on year and there is an agreement to pay £3.6M per annum in deficit catch up payments which is a material amount for a company of this size. So far in trading in the year is running in line with board expectations and they are confident that the group will return to revenue growth in 2016 with all three divisions growing by 2017. The cash position at the year-end is likely to be ahead of current market expectations.

After a 25% increase in the interim dividend, at the current share price the shares have a dividend yield of 2.6% which is expected to increase to 2.9% for the full year. Net cash at the period end stood at £43.1M compared to £47.9M at the end of last year.

Overall then this was a steady update from the group. Profits did increase year on year but this was due to one-off gains – mainly the provision release after the old property was sublet. Net tangible assets are currently negative and fell during the period as that pension deficit continued to take its toll. Underlying operating cash flows were broadly flat but an increase in payables meant that actual cash from operations was not enough to cover the pension deficit payments, although there remains a good cash level. Operationally, resources seems to be doing well but the other two divisions saw profits fall year on year, although the new contracts look promising. The forward dividend yield of 2.9% is decent enough but I don’t really see enough here to really see that much progress is being made.

It does seem as though the shares might be on a bit of an upward trajectory at the moment as the fifty day moving average moves above the 200 day MA but I am still not sure about this one.

On the 21st July it was announced that Andy Wilson sold 57,000 shares at a value of £96K. He now owns 35,184 shares in the company.

In the 6th August it was announced that some 640,000 share options had been awarded for the board at an exercise price of zero. Vesting of the shares will be based on the relative total shareholder return performance up to 2018. There are no indications of what the thresholds for vesting are. So, yet another zero price share option awards for a lot of shares in this case – I find it a shame that directors in the company need motivating in this way.

On the 5th October it was announced that a further 160,000 share options had been awarded to CFO Neil Martin, again for an exercise price of zero. The options are exercisable in the period from October 2018 to September 2025 based on the relative Total Shareholder Return from 2015 to 2018. The TSR must be at least at the medium ranking of each of the members of the FTSE small cap index in order for the options to be exercisable.

On the 16th December the group released a trading update for the full year. They expect the results to be in line with expectations with cash levels at £48.3M. Earlier in the month, an agreement was reached with the trustee of the pension scheme with regards the triennial valuation with the deficit agreed at £41.8M compared to £53.4M in 2012, at the last valuation. The recovery plan comprises an initial cash contribution of £4M to the scheme and £4M into the escrow account established previously, together with deficit recovery payments remaining at £3.6M per annum until 2024. The revaluation of the scheme is welcome but I don’t really seem anything here that is encouraging me to buy the shares.