Telecom Plus has now released their final results for the year ended 2017.

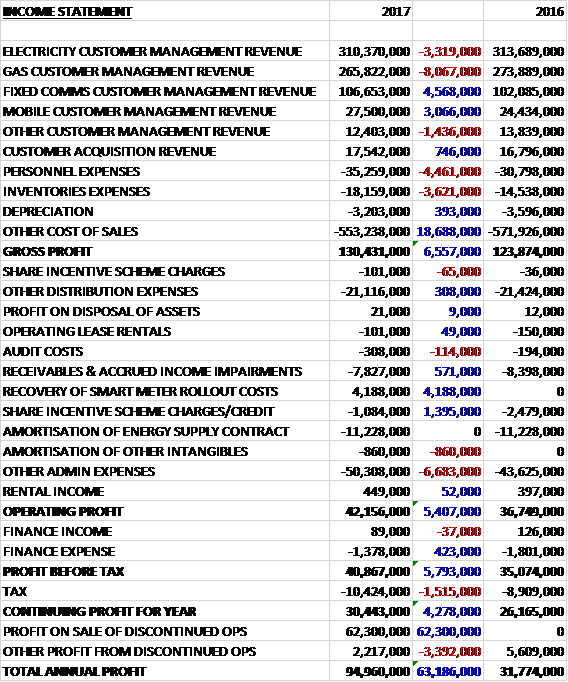

Revenues fell when compared to last year as a £4.6M growth in fixed communications and a £3.1M increase in mobile revenues were more than offset by an £8.1M decrease in gas revenues a £3.3M fall in electricity revenue due to lower energy prices and a reduction in average energy usage, and a £1.4M decline in other customer management revenue. Personnel expense were up £4.5M and inventory costs increased by £3.6M but other cost of sales declined by £18.7M to give a gross profit £6.6M above that of last year. Distribution expenses saw a modest decline but the group received £4.2M in smart meter rollout cost recoveries and the share incentive scheme cost declined by £1.4M, offset by a £6.7M growth in other admin expenses due to investment in staff and higher IT charges, to give an operating profit £5.4M higher. Finance costs decreased by £423K but tax charges grew by £1.5M which meant that the profit from continuing business for the year came in at £30.4M, a growth of £4.3M year on year.

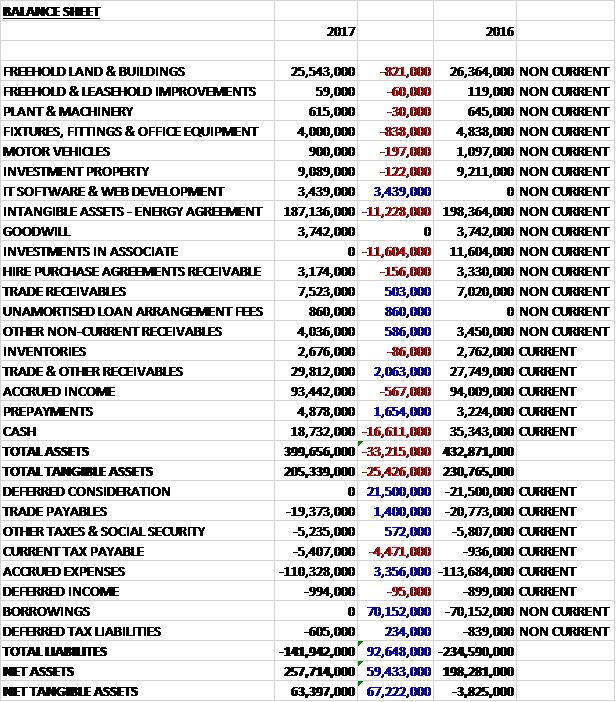

When compared to the end point of last year, total assets declined by £33.2M driven by a £16.6M fall in cash, an £11.6M reduction in the investment in the associate and an £11.2M decrease in the energy agreement intangible asset, partially offset by a £3.4M growth in IT software assets and a £2.1M increase in receivables. Total liabilities also declined during the year as a £4.5M growth in current tax payables was more than offset by a £70.2M reduction in borrowings, a £21.5M fall in deferred consideration and a £3.4M decline in accrued expenses. The end result was a net tangible asset level of £63.4M, a growth of £67.2M and much more healthy than last time.

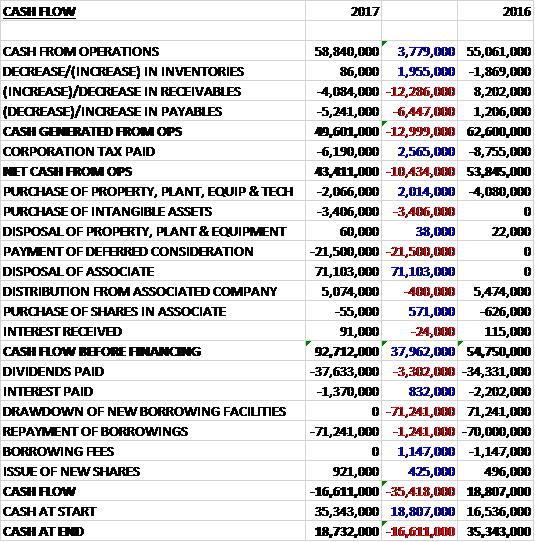

Before movements in working capital, cash profits increased by £3.8M to £58.8M. There was a cash outflow from working capital, however, and even after tax payments declined by £2.6M the net cash from operations came in at £43.4M, a decline of £10.4M year on year. The group spent £2.1M on property, plant and equipment; £3.4M on intangible assets and £21.5M on deferred consideration but received £71.1M from the sale of an associate and £5.1M in distributions from the associate to give a cash flow of £92.7M before financing. This allowed the group to spend £71.2M on loan repayments and £37.6M on dividends to five a cash outflow of £16.6M for the year and a cash level of £18.7M at the year-end.

The percentage of new members taking the double gold bundle is increasing. The Q4 figure of 55.1% is significantly higher than the 47.7% achieved in Q4 last year. The average revenue per member, however, has fallen from £1,226 last year to £1,191 in 2017. All the core services the group provides grew during the year with the highlight being a 19% rise in the number of mobile services, reaching a penetration in the residential club of 35% as the board made a strategic decision to place mobile at the heart of their retail position and to improve its competitive position.

The small decrease in revenue during the year has been driven mainly by lower average energy prices as a result of retail gas price reductions in 2016, and reduced average energy usage due to the continuing impact of energy efficiency measures across the industry combined with a steadily increasing number of LED light bulbs installed due to project daffodil. This was partly offset by an increase in telephony revenues resulting from an increasing penetration of fibre broadband and some higher fixed monthly charges, and the overall increase in the number of services provided to members.

The record gap between standard variable energy tariffs and aggressively prices introductory deals started to narrow during the autumn but this happened too late to provide any positive impact on Q3. At the beginning of Q4 the group responded to this by making a change to their partner compensation plan and this, combine with the more competitive market position, led to an increase in partner activity as the quarter progressed and services increased by more than 107,000 in the year as a whole.

The 20% stake in Opus Energy was sold in February, resulting in the receipt of £71.1M in cash and an exceptional profit from the sale of £62.3M. The business is a decent provider of profit to the group, however, so this revenue stream will be missed.

The group had previously announced their intention to carry out a tender offer under which they would return to shareholders the cash they received from sale of their stake in Opus. They have now decided to reduce the maximum size of this offer to £25M.

The board are encouraged by the results from the soft launch of their home insurance service. They expect volumes will start to improve from their current low levels as they start marketing the new service more proactively, and remain confident that insurance has the potential to make a material contribution to the financial performance in due course.

Project Daffodil, the free LED lightbulb service, has gathered momentum and have now been provided in over 40,000 households. This has been a major factor behind the improvement in the quality of new members joining the club as well as encouraging existing members to add additional services in order to take advantage of this benefit.

The mobile app that was launched a year ago has gained widespread acceptance, with around 65,000 members using it each month to submit meter readings, top up their mobile, track their mobile usage and find their nearest cashback retail outlets. More functionality will be added in due course, including being able to manage their insurance cover.

The smart meter rollout programme has been hampered by the persistent failure of one of the meter operators to meet the agreed service levels. In addition to slowing their rollout programme, this also affected their ability to install pre-payment meters in a significant part of the country during the second half of the year, leading to a small rise in delinquency levels. They have now appointed a new meter operator to take over this work and have now installed over 100,000 meters to about 10% of the current base.

The group experienced a reduction in the number of registered partners, largely due to their decision last autumn to provide automatic refunds to many of those who join the business but find themselves unable to build a secure part-time additional income. These early refunds, combined with the natural underlying level of cancellations led to a larger reduction in the total number of registered partners than would have otherwise been the case.

Based on recent levels of partner activity, the board expect the number of service they supply will increase by between 5% and 10% over the coming year. The modest growth in the number of services added over the past few years combined with higher customer acquisition costs and an increasing investment in IT meant that profits for the coming year are likely to be at a similar level to the year just ended. The benefit from faster organic growth will, if current trends continue, be reflected in the results for the following year.

After taking off the smart meter roll out cost recovery the shares are trading on a PE ratio of 33.8 which falls to 20.3 on next year’s consensus forecast. After a 4.3% increase in the total dividend the shares are yielding 4.4% which increases to 4.5% on next year’s forecast. At the year-end the group had a net cash position of £18.7M.

Overall then this has been a bit of a flat year for the group. Excluding the recovery of smart meter costs, profit was broadly flat, net assets improved considerably due to the Opus sale but operating cash flow declined due to working capital movements – cash profits grew and there was a decent amount of free cash generated. Operationally, there has been increased activity but there was a lower average revenue per customer due to reduced energy prices and usage. The home insurance initiative looks interesting but will not benefit the group in the coming year.

The Opus sale is a bit of a shame. It has really improved the balance sheet but Opus was a decent, profitable part of the business so the income from there will be lost. Next year is likely to be flat with regards profits and the forward PE of 20.3 does not look that cheap. The yield of 4.5% is better, and it does look just about sustainable so the shares might be an income play. Not too excited but might keep a watch for a lower entry price.