Omega Diagnostics has now released its interim results for the year ending 2017.

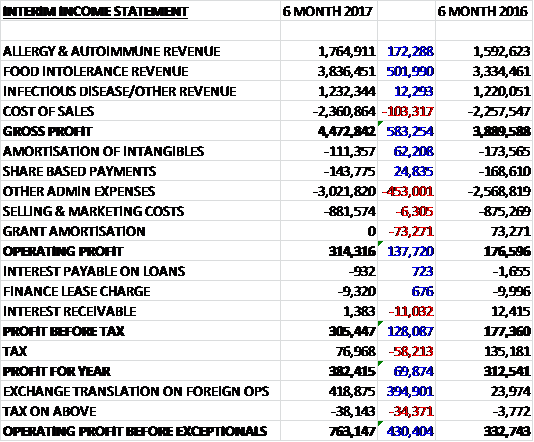

Revenues increased when compared to the first half of last year, £500K of which was due to favourable currency movements, with a £502K growth in food intolerance revenue, a £172K increase in allergy revenue and a broadly flat infectious disease revenue. Cost of sales saw a modest increase and gross profit grew by £583K. Amortisation and share based payments saw small declines but other admin expenses were up £453K and there was no grant amortisation which saw an income of £73K last time. This meant that the operating profit increased by £138K. There was an £11K decline in interest receivable and a £58K fall in tax receipts due to a reduced tax credit so the profit for the period came in at £382K, a growth of £70K year on year.

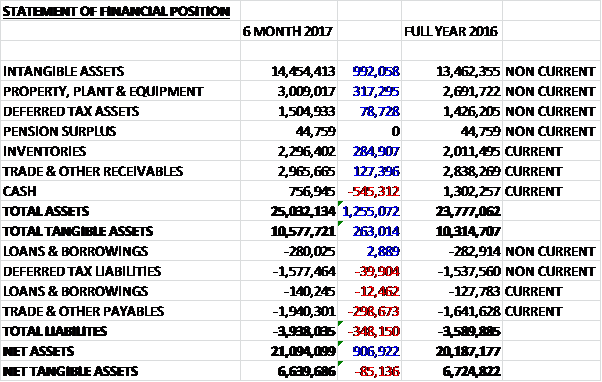

When compared to the end point of last year, total assets increased by £1.3M driven by a £992K growth in intangible assets, a £317K increase in property, plant & equipment, a £285K growth in inventories and a £127K increase in receivables, partially offset by a £545K reduction in cash. Total liabilities also increased during the period due to a £299K growth in payables. The end result was a net tangible asset level of £6.6M, a decline of £85K over the period.

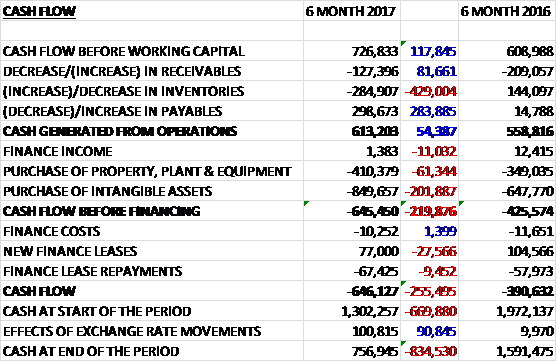

Before movements in working capital, cash profits increased by £118K to £727K. There was a cash outflow from working capital due to a growth in inventory and receivables to give an operating cash flow of £613K, a growth of £54K year on year. The group spent £410K on property, plant & equipment; and £850K on intangibles to give a cash outflow of £645K before financing. New finance leases offset finance costs and there was a cash outflow of £646K for the period to give a cash level of £757K at the end of the half.

The loss in the Allergy and Autoimmune division was £96K, an improvement of £59K year on year with revenue up 11%, mainly due to a favourable currency impact from the domestic German allergy business. In constant currency terms, revenue was stable in Germany, halting the recent history of decline due to reimbursement pressures.

The pre-tax profit in the Food Intolerance business was £1.6M, a growth of £509K when compared to the first half of last year. The microarray-based Foodprint system has achieved particularly good growth with revenue increasing by 46% to £2.2M, including one account win in North America, a market which is seen as increasingly important for longer term growth. Food Detective revenue fell by 22% to £930K as the group took a decision to reduce pipeline stocking in two of their key markets.

The pre-tax loss in the Infectious Disease business was £147K, an improvement of £56K when compared to the first half of 2016 with gains in some regions being oddest by reductions elsewhere. The modest increase in revenue was due to favourable currency movements.

With the point of care tests, the group have confirmed they have eliminated an ambient temperature effect when tested on over 100 HIV+ samples in a UK hospital. They also have data on a further 400 samples and results overall indicate they are meeting their design goals of sensitivity and specificity. They are now in a period of formal design control which means they now have the device format which they expect to take to market. The remaining work they plan to do will be undertaken to confirm this is the case. They have now manufactured all the components necessary to assemble a scaled-up batch size of 10,000 devices which will be used in external trials and for assay robustness studies.

For the rapid test manufacturing, the group intend to complete all stages of the BSI Quality Management System review for their facility in Pune and remain on course to achieve CE-marked malaria and pregnancy tests available for sale in Q4.

In allergy automation they CE-marked their allergy launch panel comprising 41 allergens which are capable of being run on the IDS-iSYS instrument and whose performance matches that of the market-leading product. They are also finalising a long-term supply contract with their first customer in Germany. They have initiated recruitment of skilled project managers and leaders into the scientific team that is responsible for delivering menu expansion, beyond the initial launch panel.

After the period-end, the group have been approached by their Allersys licensor with a view to changing the nature of the commercial relationship with the company which could extend to the acquisition of all or part of the Allergy business. Under the terms of the agreement, the license can be terminated by IDS should they wish to do so. The board believe that it is in both parties’ interests to explore all the possibilities of a new commercial relationship and to avoid a situation whereby there are no winners should IDS exercise their right to terminate the contract. That’s as clear as mud.

The approach from IDS notwithstanding, the outlook for the rest of the year is encouraging within the core business with revenue and adjusted profit expected to be at the higher end of market expectation due, in part, to favourable currency movements.

The company is not exactly a value play, at the current share price the shares trade on a PE ratio of 35.2 which falls to 16.4 on the full year forecast.

Overall then this has been a solid period of progress for the group. Profits were up, as was operating cash flow but there was no free cash generated. Net tangible assets were broadly flat during the period. Both the allergy and infectious disease businesses posted slightly improving losses with currency movements likely the reason. The group continues to be carried by the food intolerance business where Foodprint drove growing profits in the division.

Going forward, it seems real progress is being made on the infectious disease tests and the allergy tests seem ready to go, although the approach from IDS injects some uncertainty here so it would be good to find out what they are intending to do. With a forward PE of 16.4 these shares are not cheap but I think they show enough promise to carry on holding.

On the 27th January the group released an update on negotiations with IDS. They have confirmed that their preferred course of action is to pursue an enlarged distribution relationship with the group. Currently they have contractual rights to be appointed exclusive distributor in the UK, France, Germany, Austria, Switzerland, Scandinavia and the USA. The ongoing discussions will focus on how Omega can attain a more global reach for its Allersys tests in a structure that benefits both companies. Currently they have 41 tests which can run on the automated instrument.

On the 29th March the group announced that it has CE-marked its VISITECT range of Malaria tests. The completion of the validation programme means these tests are available for general sale through the business to business channels in those countries that do not require individual product registration. The group anticipate achieving additional regulatory approvals within the next 12 months to enable them to participate in higher volume tender business.

In addition, they confirm that their manufacturing facility in India has undergone an annual inspection from the Indian FDA, confirming the facility is compliant with the GMP processes for manufacturing, testing, storage and QA processes and that its manufacturing license is valid until the start of 2021. Whilst the board expect relatively modest sales during 2018, they anticipate generating significant demand from the subsequent financial year onwards.

On the 25th April the group announced that results for 2017 will be in line with market expectations. Revenues are expected to be £14.3M, 3% ahead of last year on constant currency terms and 12% ahead of last year’s result on an actual basis. Food intolerance is expected to rise 13%, allergy and autoimmune up 14% and infectious disease up 5%. Adjusted pre-tax profit is expected to be £1.1M.

In Allergy, the group continue to have discussions with IDS on how best to commercialise their Allersys range or reagents and believe they can achieve an outcome that will benefit both parties. They have continued to develop the allergen range and they have now optimised a further nine allergens in addition to the 41 allergens which are CE market for use on the IDS instrument.

In Infectious disease, they have now attained formal design freeze with their VISITECT CD4 test following the successful manufacture of three pilot batches. Devices from these batches were tested at three UK hospital sites, on sufficient numbers of patient samples to demonstrate that they now have a method for manufacturing devices which consistently meet their design goal specifications.

Achieving this milestone means that the group have now progressed into the formal verification and validation phase. They will use the chosen design to manufacture three validation batches which will be sent for field trial evaluation at selected sites in the UK and India. The field trial results, combined with a number of planned internal experiments to support product claims will, if successful, enable them to CE-Mark the test after the conclusion of these activities.

The group have also achieved full operational capability with their manufacturing facility in India which should achieve modest sales of their Malaria range of tests this year. Going forward, the food intolerance division continues to grow and the board are reviewing initiatives as to how they may grow this business in North America. The allergy business in Germany achieved a 3% increase in Euro denominated turnover, reversing the declining trend.

Things seem to be ticking along OK but the major uncertainty remains the discussions with IDS over the Allersys range.