Trifast has now released its interim results for the year ending 2017.

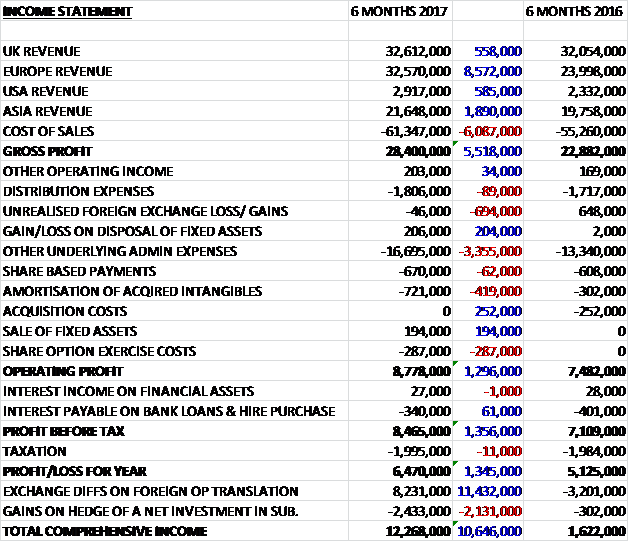

Revenues increased when compared to the first half of last year with an £8.6M growth in European revenue, a £1.9M increase in Asian revenue, a £585K growth in US revenue and a £558K increase in UK revenue. Cost of sales also increased to give a gross profit £5.5M above that of last time. There was a £694K detrimental movement to exchange losses and other underlying admin expenses increased by £3.4M. We also see a £419K growth in the amortisation of acquired intangibles and a £287K share option exercise costs, partially offset by the lack of £252K of acquisition costs and £194K from the sale of fixed assets which meant that the operating profit grew by £1.3M. Interest costs reduced slightly and taxation was broadly flat so the profit for the half year came in at £6.5M, a growth of £1.3M year on year.

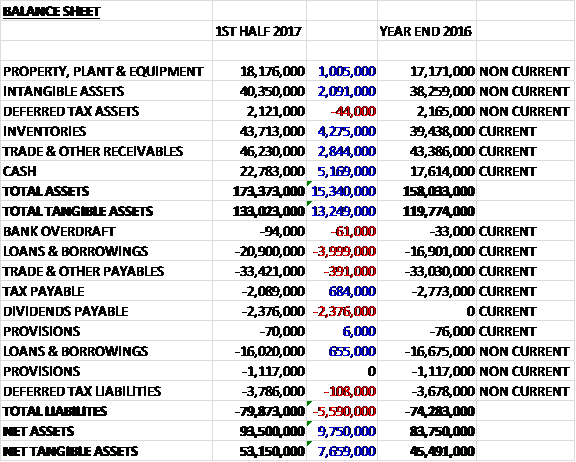

When compared to the end point of last year, total assets increased by £15.3M driven by a £5.2M growth in cash, a £4.3M increase in inventories, a £2.8M growth in receivables, a £2.1M increase in intangible assets and a £1M growth in property, plant and equipment. Total liabilities also increased during the period due to a £3.3M growth in borrowings and a £2.4M increase in dividends payable. The end result was a net tangible asset level of £53.2M, a growth of £7.7M over the past six months.

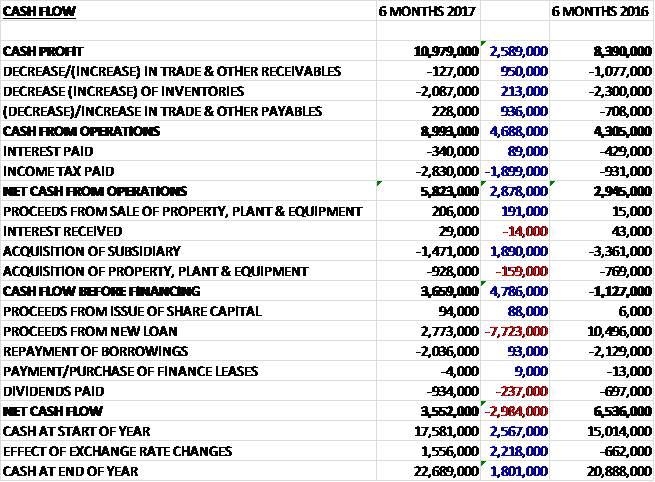

Before movements in working capital, cash profits increased by £2.6M to £11M. There was a cash outflow from working capital but this was less than last year but tax payments increased by £1.9M to give a net cash from operations of £5.8M, a growth of £2.9M year on year. The group spent £928K on property, plant and equipment (expected to increase in the second half) along with £1.5M on acquisitions which represented the final deferred payment for Kuhlmann, which meant that the free cash flow was £3.7M. Of this, £934K was spent on dividends but a growth in loans meant that the cash flow for the period came in at £3.6M to give a cash level of £22.7M – could another acquisition be on the cards?

Overall forex tailwinds brought an additional £1M to underlying pre-tax profit. Despite negative media predictions of both UK and global economic malaise, the group has sustained its trading dynamics in most geographic sectors. The one exception is the reduced domestic automotive output in Malaysia which has affected Power Steel and Electro Plating Works. That is currently being addressed by promoting its unutilised capacity to the Tier 1 automotive customers in the EU and US. Meanwhile all the other businesses are maintaining organic growth.

Over recent years there has been a trend for high volume assembly operations to migrate to new countries to preserve competitive advantages. It is this transience that helped to drive the group’s international expansion by following customers to new production sites, the latest step seeing them open a new logistics centre in Barcelona. Trading from this greenfield site is expected to start early next calendar year and responds to customer requests to provide technical and logistics support locally in Spain.

With meaningful manufacturing capacity expansion projects underway in Italy and Singapore, the UK management team is reviewing the cost benefits of how they collect, store and access the group’s purchase logistics and sales data by means of more interactive systems that will improve processing efficiency. This is a long-term project with the benefits expected by the end of 2018.

The underlying profit from the UK business was £3M, a decline of 52K year on year with marginal growth in revenue.

The underlying profit from the European business was £5.3M, a growth of £2.4M when compared to the first half of last year with £600K of that coming from Kuhlmann. The most recent acquisition, Kuhlmann in Germany, is performing well and has enlarged its sales force to add more resource to its domestic growth opportunities that have been identified by the team. Along with the contribution from Kulmann, there was strong organic growth in the domestic appliances business in Italy, electronics in Hungary and automotive across the Netherlands and Sweden.

The underlying profit from the US business was £166K, a decrease of £80K when compared to the first half of 2016 despite revenues increasing. This decline in margin is due to investment in US resourcing levels ahead of the curve to support expected revenue growth. As these revenue streams continue to increase, the margin should improve.

The underlying profit from the Asian business was £3.3M, a decline of £441K year on year with much of this decrease as a result of forex movements, particularly in China. There was growth in the Singapore and Chinese businesses but this was offset by lower sales in Malaysia.

The group announced that having been involved in the business for over 35 years and as executive chairman since 2009, Malcolm Diamond announced that he was relinquishing his executive duties and the end of the year to become non-executive Chairman.

There are some macroeconomic factors that the group can’t fully mitigate, including the ongoing volatility in forex movements and raw materials markets, as well as the wider potential implications of Brexit on the business and the UK economy. The group are already starting to see some purchase price challenges in the UK business from the ongoing weakness in Sterling and they expect these pressures to increase over time if that weakness persists. As in international business with over 70% of revenues being generated outside the UK, however, the board remain confident they have the flexibility to meet these challenges head on as and when they arise.

Europe remains the key area for organic growth. They have investment projects already underway to increase their manufacturing capacity in Italy and their new greenfield site in Spain is already providing opportunities to better access the multinational OEMs operating in the region. Additional investments are being made across the world, in both their global and local sales resources and supporting teams, as well as to improve the digital and integrated business management systems.

At the current share price the shares are trading on a PE ratio of 22.3 but this reduces to 12.8 on the full year consensus forecast. After the interim dividend was increased, the shares are yielding 1.6% which remains the same on the full year forecast. At the period-end the net debt positon was £14.2M compared to £16.3M at the same point last year and £16M at the year-end.

Overall then this has been a pretty solid year for the group. The profits increased but this seems to be attributable to the Kuhlmann acquisition and favourable forex movements – like for like profits seem a bit flat. The net assets increased and the operating cash flow improved too with a decent amount of free cash being generated. Profits in the UK were flat so the growth all came from Europe with a good contribution from Kuhlmann and improvements in Italian domestic appliances, Hungarian electronics and Dutch/Swedish automotive, aided by the weakness of Sterling.

Elsewhere, the US saw a modest decline in profits due to increased costs before future revenues come on stream, and Asia saw a larger decline due to less favourable currency movements and a reduction in automotive output in Malaysia. The Brexit vote could impact on the group and they are already seeing some purchase price challenges in the UK but this should be offset to some extent by more revenue from Europe as the Euro continues to strengthen against Sterling. The forward PE ratio of 12.8 does not look too taxing but the yield of 1.6% is nothing to write home about. Overall these shares remain a hold for me.

On the 16th February the group released a trading update covering Q3. On a constant currency basis they are continuing to report a strong performance. The Asia business returned to growth as it began to benefit from the recovery in demand during the second half and the UK and US operations are continuing to produce results in line with management expectations. In Europe the business overall has performed solidly, delivering growth, although they are seeing a slight change in product mix – there has also been an encouraging start at their newest greenfield operation in Barcelona.

Since the end of the first half, the sustained weakness in Sterling has had a further positive translation impact on profit. In the shorter term, if this weakness persists they expect there to be an additional positive effect on profits but in the longer term they may start to experience some challenges in the UK business in terms of input costs.

Given trading in Q3 and the further forex tailwinds, the group’s performance for the full year is expected to be slightly ahead of previous expectations. This all seems decent enough to me and I continue to hold.

On the 20th April the group released a trading update covering the year. On a constant currency basis, the year finished strongly with the group’s main markets all contributing to trading results ahead of management expectations reflecting the compelling underlying organic growth from the key sectors they operate in.

In Asia, the TR business continued its return to growth building on the profitable return achieved in H1 and benefiting from the recovery in demand both in the domestic and export markets from their key sectors of industrials, electronics and automotive. In the UK they have experienced good growth coming through from both their OEM and distributor export businesses. They US operations, albeit from a small base, have produced double digit growth with trading results in line with expectations. In Mainland Europe the business overall has performed well delivering year on year growth. In the German business they have benefited from both organic and cross-referral opportunities from around the group.

The capital investment programme during the year totalled £3M which has provided additional capacity in Asia and Europe. Last time the board reported that they experienced translational forex tailwinds of about £1M and in the second half the sustained weakness of sterling has had an additional positive translational impact of £1.4M.

Looking ahead the board have already started seeing some purchase price challenges in their UK business from the ongoing weakness in Sterling and they remain mindful that if this weakness persists, these pressures may increase over time. Nonetheless as they enter the new financial year they remain confident in their prospects.