Goodwin has now released its interim results for the year ending 2017.

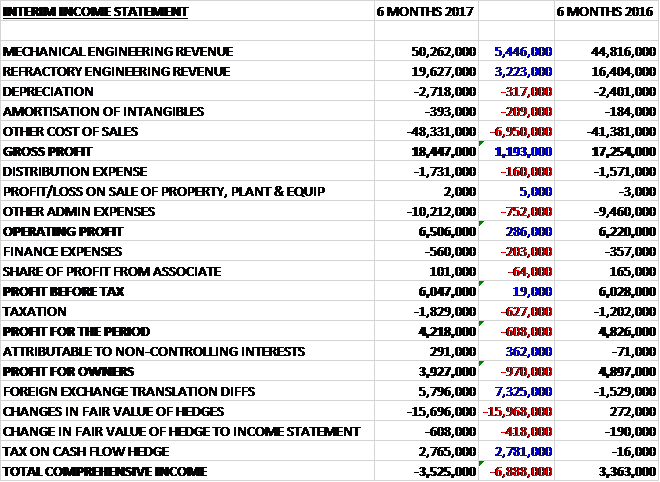

Revenues increased when compared to the first half of last year with a £5.4M growth in mechanical engineering revenue and a £3.2M increase in refractory engineering revenue. Depreciation was up £317K, amortisation grew £209K and other cost of sales increased by £7M to give a gross profit £1.2M above that of last time. Distribution expenses increased by £160K and admin costs were up £752K which meant that the operating profit grew by £286K. We then see a £203K increase in finance expenses, a £64K reduction in profits from the associate and a £627K increase in tax payments, all of which meant that the profit for the period was £3.9M, a reduction of £970K year on year.

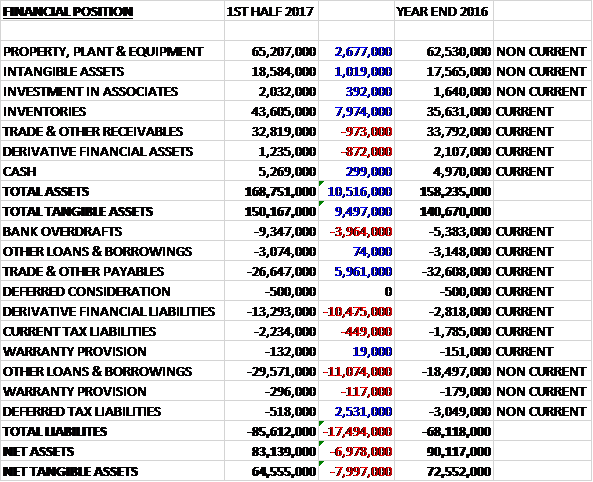

When compared to the end point of last year, total assets increased by £10.5M driven by an £8M growth in inventories, a £2.7M increase in property, plant and equipment due to forex movements and a £1M growth in intangible assets (again due to forex movements), partially offset by a £973K decline in receivables and an £872K fall in derivative financial assets. Total liabilities also increased during the period was a £6M decline in payables and a £2.5M fall in deferred tax liabilities were more than offset by a £10.5M increase in derivative financial liabilities, an £11.1M growth in loans and a £4M increase in the overdraft. The end result was a net tangible asset level of £64.6M, a decline of £8M over the past six months.

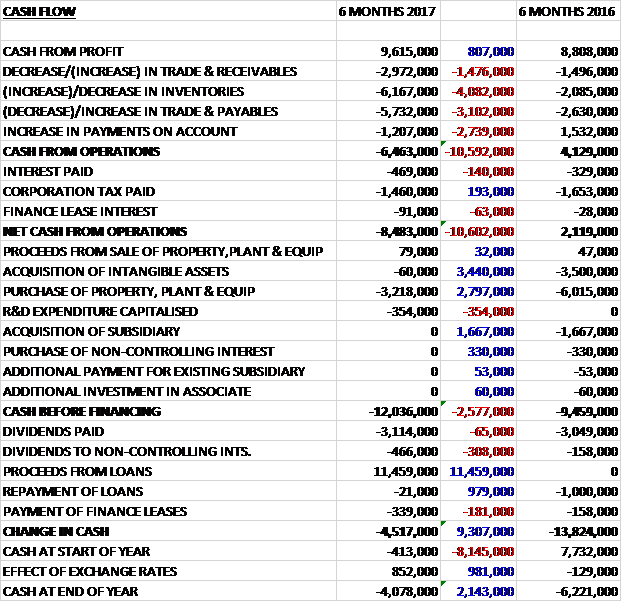

Before movements in working capital, cash profits increased by £807K to £9.6M. There was a huge increase in working capital cash outflows, however, and after an increase in interest payments broadly cancelled out a decline in tax payments, the net cash outflow from operations was £8.5M, a detrimental movement of £10.6M year on year. The group spent £3.2M on property, plant and equipment along with £354K on R&D and £60K on other intangible assets to give a cash outflow of £12M before financing. The group therefore took out £11.5M in more loans but paid out £3.5M in dividends so there was a cash outflow of £4.5M during the period and a cash level of -£4.1M at the period-end.

The profit in the Mechanical Engineering division was £4.8M, a decline of £557K year on year. The further depressed state of capex on oil, gas and mining projects will be a challenge to the division in 2017. The profit in the Refractory Engineering division was £2.2M, a growth of £625K when compared to the first half of last year with markets as a whole remaining stable.

The current workload stands at £84M and sales orders dispatched up to the period end were £69.9M but the margins are lower due to the increased competition in the tighter market. Growth areas in the refractory engineering products continue to provide good opportunity whilst a better base load within the longer term defence work has given some reassurance in comparison to the continued low new project and procurement activity in the oil, gas and mining industries.

The group’s capex is very much reduced, other than customer project financed development, they are restricting expenditure. With the likely continued low oil and gas and metal ore prices it would be unrealistic to expect any significant recovery in pre-tax profitability until after 2018.

The group have brought some new products to market such as their axial piston shut off and control valves, their new range of duplex and high impact resistant carbon steels and products that use their AVD vermiculite dispersions such as fire extinguishers, lithium battery transport bags and fire resistant paints. For all these products they have patents applied for and they should provide the group with a sound base to start growing again.

Following the Brexit vote, Sterling has depreciated against most major currencies. At the period-end the cash flow hedge reserve is significantly negative which reflects the marked to market values of currencies sold to/ purchased from the banks in relation to the group’s underlying currency sales and purchase requirements. Judging the future relationship of the major currency pairs apparently continues to be a challenge.

The mechanical engineering division companies with the exception of Easat Radar Systems are seeing their order backlog go down as it is likely to continue to do so during 2017. Goodwin International, which had the highest activity level in the oil and gas industry, has in part mitigated the severe purchasing activity decline in this sector by winning significant levels of business in the nuclear engineering sector, which has business to place for the next ten years. The hardest hit business is the foundry, Goodwin Steel Castings. Whilst over the past three years it has done better than most other competitive foundries it is now short of order input and as such is looking to ramp up new business for submarines in the UK and US following their recent approval to produce HY80 cast material.

At the current share price the shares are trading on a PE ratio of 14 but there are no forecasts for this company. As usual, no interim dividend was announced so the shares still yield 2.5%.

Overall then this was a difficult period for the group. Profits declined, not helped by increased tax charges, and net assets decreased. The operating cash outflow was a bit of a disaster but this seems to have been as a result of working capital movements and cash profits actually grew in the period. The refractory engineering business seems to be doing fine but the mechanical engineering business is really struggling in the face of reduced investment from the oil and gas industry. Management are not expecting a pick-up until 2018 at the latest so I don’t think the PE of 14 and yield of 2.5% fully reflect this.

On the 10th March the group released a trading update covering Q3. In the first nine months of the year revenue increased by £17.5M but pre-tax profit was down £800K to £8.2M due to much fiercer competition for the lower level of orders being placed in the oil and gas industry. The market remains very quiet and order input for the group as a whole is 10% lower than in Q3 last year. The refractory engineering businesses are still increasing sales volumes and profit, however.