Gem Diamonds is a diamond miner listed on AIM. They have two assets – the 100% owned Ghaghoo mine in Botswana that is yet to be fully operational but has a massive total resource of 20.5M carats; and the Letseng Mine in Lesotho, 30% owned by the Lesotho government with a total resource of 5M carats. The Letseng diamonds are much more valuable, however, with $10.4BN of value in situ compared to just $4.9BN at Ghaghoo. The group has now released its final results for the year ending 2014.

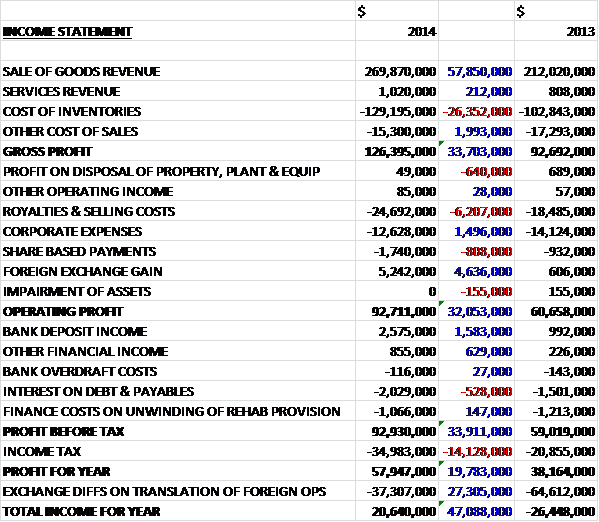

Overall revenues increased by $58M to $270M, driven by 12% higher volumes and 24% higher prices achieved, and with cost of inventories also increasing, partially due to increased waste stripping costs, the gross profit was some $33.7M higher than last year. Royalties and selling costs increased by $6.2M but this was partially offset by a $1.5M decline in corporate costs and a $4.6M foreign exchange gain to give an operating profit $32.1M higher at $92.7M. The various finance costs and expenses broadly cancel each other out with an improving bank deposit income meaning that the profit before tax was $33.9M higher at $92.9M before a big increase in the tax bill took this down to a profit for the year of $58M, a $19.8M improvement on the outcome in 2013.

When compared to the end point of last year, total assets increased by $42.3M. This increase was driven by a $39.6M growth in cash levels and a $29.7M increase in exploration and development assets, partially offset by a $7.4M fall in the value of plant & equipment due predominantly to exchange rate differences, a $9.4M decline in the stripping activity asset, a $7.4M fall in mining assets and a $5.1M fall in decommissioning assets. Liabilities also increased during the year due to $37.1M hike in the value of loans and borrowings, a $6.8M growth in tax liabilities (despite a decline in deferred tax due to a fall in the value of property, plant and equipment) and a $5.2M increase in accruals, partially offset by a $3.6M fall in rehabilitation provisions to give a net asset base some $3.1M lower than last year at $347.6M.

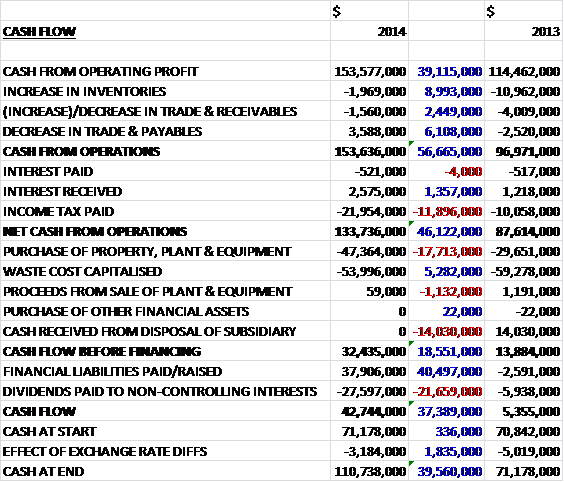

Before movements in working capital, cash profits increased by $39.1M to $153.6M and with working capital changes fairly neutral this year, the cash from operations was still $153.6M, albeit some $56.7M higher than last year. After the effect of income tax, this was reduced to $133.7M. The bulk of this cash was then spent on waste processing ($54M) and the purchase of property, plant and equipment ($47.4M) which included $11.3M spent on the Coarse Recovery plant, the plant 2 phase 1 upgrade and additional resource extension drilling at Letseng; and $35.1M spent at Ghaghoo representing the remaining phase 1 capital project costs together with six months operational costs during the commissioning phase that have been capitalised, so that before financing the cash flow was $32.4M. Most of this was then given to the non-controlling interest so that free cash flow was just $4.8M. Strangely the group then took out a net $37.9M in loans to give a cash flow for the year of $42.7M and a cash pile at the end of 2014 standing at $110.7M.

During the year concerns regarding continued liquidity constraints in the market and the tightening of lending criteria by a number of prominent diamond banks, including the announcement of the closure of the Antwerp Diamond bank in October, negatively affected diamond prices and trading activity during the second half of the year as buyers adopted a more cautious approach, further fuelled by a disappointing Hong Kong jewellery show in September. The high value rough diamonds of Letseng remained fairly resilient, however, with a total of $2,799 achieved per carat in December compared to an average of $2,540 for the year. It is likely, though, that this issue will filter through to Letseng eventually and it will certainly be affecting any sales of Ghaghoo products.

In the short term there is a relative balance between the demand and supply of diamonds but in the medium term, demand is expected to outstrip supply as ageing mines become depleted and not many new mines are brought online. The slowdown in GDP growth in China is likely to have a negative impact on prices but this has been partially offset by the recovery seen in the US economy with diamonds used in the production of jewellery remaining the primary driver of demand. In the market as a whole, Gem Diamonds is a small player, producing 119K carats compared to a world estimate of 131M carats, although the commissioning of the Ghaghoo mine should add another 220K to the group’s total.

At Letseng, a solid year of operations saw an improvement over last year’s production total and improved blasting techniques, plant enhancements and a greater access to ore from the higher grade satellite orebody resulted in an improvement in the grade, size and quality of diamonds produced. During the year, a revised resource statement was released, reflecting a significant increase in the indicated resource category which had been extended in depth to approximately 350 metres below the current mine pits on both the main and satellite pipe orebodies. As a result of this increase, the entire 22 year life of the mine has now been classified as reserves.

The improvement in the Letseng mine focused on relatively low capital expenditure projects during the year. The new Coarse Recovery Plant remains on track to be completed at the end of Q2 2015 which will optimise the treatment of the coarse fraction ore using X-ray transmissive technology that will improve the recovery of the high value Type 2 diamonds. Implementation of the Plant 2 Phase 1 upgrade project started in Q3 2014 and is on track to be completed in early 2015 at a capital cost of $4.7M. This project should increase treatment capacity to 250,000 tonnes per annum and further reduce diamond damage. Subsequent upgrades to the plant will be considered once the current projects are completed and the performance has been fully evaluated.

The mine produced 108,569 carats, a 14% increase on the previous year due to the increased contribution from the higher grade Satellite pipe (31% compared to 16% last year) and the higher than expected performance of the reserve grade. Total direct cash costs at Letseng were LSL884.6M compared to LSL801.1M last year resulting in unit costs per tonne of LSL137.75 compared to LSL128.68 in 2013. This increase is primarily as a result of general inflation increases, increased fuel and power costs, additional costs relating to back up power facilities and diamond reduction initiatives, partially offset by savings achieved through the new mining contracts. Waste stripping activities continued apace in line with the mine plan and the requirement to access the higher grade satellite ore in higher proportions and overall nearly 20M tonnes were moved. The mining contractor delivered larger mining equipment that included five new 100 tonne dump trucks and two new excavators which improved the waste mining efficiency.

Significant improvements in sidewall control and blasting of the pit slopes allowed to the slope angles of the mine to be increased which will result in lower stripping ratios, significantly reducing the total cost of mining over the life of the mine. The group renegotiated its contract with the mining contractor a year ahead of the expiry of the last one which resulted in improved unit costs for the next eight years, starting at the beginning of 2014. They also embarked on a number of initiatives to reduce diamond damage at the mine with changes to mine blasting practices resulting in improved fragmentation of the ore for the treatment plants which contributes to reduced damage and this, plus some of the initiatives embarked on last year have resulted in a reduced breakage trend for the valuable type 2 diamonds.

The Ghaghoo mine is being developed in a phased approach. The first phase is aimed at confirming diamond grades and prices, as well as testing different mining and processing techniques with subsequent phases increasing production. The mine is currently in its first phase with the capital project complete and commissioning progressing well. It has completed the phase 1 capital project which entailed developing an access decline through 80 metres of sand overburden and three production tunnels in the first level of mining. The tunnels in the old sampling level were intersected in August and they were dewatered and inspected and found to be stable. Two ventilation holes were drilled with one being equipped as an emergency escape route.

So far, 48,023 tonnes of ore has been treated with 10,167 carats recovered including a 20 carat white diamond, a 17 carat white diamond and a 3 carat orange diamond which confirm the presence of the valuable coloured gemstones. After the year end a 35 carat diamond was recovered, which is the largest found at the mine to date. The mine averaged a grade of 21 carats per tonne which was below the expected 27 carats per tonne, partially due to the highly diluted ore from the margins of the pipe and plant inefficiencies during early commissioning. The grade improved as the year went on after an optimisation process at the treatment plant and it is expected that reserve grades will be achieved as both the plant and mining operations reach steady production levels.

The first tender of 10,167 carats was held in February 2015 and achieved just $210 per carat (compared to more than 10 times that at Letseng) but it will apparently take at least six months of tender sales and the subsequent sale of the polished diamonds by clients in order for a reliable price to emerge. About 60,000 tonnes per months is expected to be achieved at the mine by mid-2015 as part of the phase one plan. Progress at Ghagho has not been without its problems as during the year a significant ingress of water was encountered following the intersection of a fissure in the basalt rock, which has now been overcome but led to a delay in the planned ramp up of production

During the year, Letseng recovered seven 100+ carat diamonds with the largest being a massive 299 carat yellow diamond which was sold into a partnership arrangement in early 2015, where the mine will further share in 50% of the uplift from the eventual polished sale value. During the year the mine sold 108,963 carats at an average price of $2,540 per carat compared to $2,043 the previous year.

The manufacturing operation in Antwerp contributed $3.9M to EBITDA with $5.1M of diamonds sold and $15M remaining in inventory, which relates to a much larger amount unsold than last year.

It is worth noting that the group has a lot of operating leases with the contract of Letseng equipment relating to $323M over eight years. There was also nearly $16M of capital expenditure approved, mostly relating to the new Coarse Recovery Plant and the Plant 2 Phase 1 upgrade at Letseng. In addition there are possible tax disputes of $4.9M lurking in the background.

The Lesotho government certainly gets their cut of the diamond revenues with royalties of $22.1M paid this year and a further $27.6M in dividends relating to their 30% ownership of the Lesotho mine also being paid out this year, $6.5M of which related to the withholding tax. During the year the country did suffer some political unrest but the mine, which is located four hours away from the capital, was not affected. The country has since stabilised with elections having taken place in February 2015 but this is something that I will have to keep an eye on.

As can be seen, despite the healthy cash pile the group has taken out a number of new loans. There is a LSL140M three year unsecured project debt facility signed with Standard Lesotho Bank and Nedbank for the total funding of the new Course Recovery Plant. The loan is for $12.1M repayable in ten quarterly payments starting at the end of March 2015 with a final payment in June 2017. The loan has a fairly hefty interest rate of 11%. The other loan is a nine month unsecured $25M facility signed with Nedbank Capital in January 2014 for the remaining spend on the Ghaghoo Phase 1 development. The loans have been refinanced into a six year secured project debt facility which will expire at the end of 2020 with an interest rate of 2.6%. Total interest for the year has been $1.1M and there remains $41.6M undrawn on these facilities.

Clearly there are a number of risks facing the group with them being susceptible to the price of diamonds which have showed some weakness towards the end of the year and is, in turn, partly affected by global economic conditions. There is also a foreign exchange risk particularly with the Lesotho loti, South African Rand and Botswana pula while the group’s sales are denominated in US dollars, which is not the functional currency of the mining operations. The group is also susceptible to potential political unrest as the disruptions preceding the Lesotho elections this year had shown, although it is probably fair to say that Lesotho and Botswana are two of the more stable African countries.

Despite a weakening of prices in Q4 the long term outlook for the diamond market remains strong and the group expects a firming in the market after banks in Dubai stepped in to offer the liquidity lost after the bank in Antwerp reduced funding. The Chairman therefore expects diamond prices to begin trending upwards in the second half of 2015. The focus next year will be on converting the Ghaghoo mine from a development project into sustained operational activities and achieving steady state production by the end of the first half of 2015 with the aim of generating a positive contribution to EBITDA.

At the current share price, the shares trade on a cheap looking P/E ratio of 9.7 which falls slightly to 9.6 on next year’s consensus forecasts. After the maiden dividend was announced, the shares yield 2.1%, falling slightly to 2% on the 2015 forecast. The policy going forward will be to determine the appropriate dividend each year based on consideration of the company’s cash resources, the level of free cash flow and earnings generated during the year. They are expected to be delivered annually with the full year results. There was a net cash position of $73.6M at the end of the year which seems pretty healthy.

Overall then, this seems to be a generally positive set of results, tinged with a bit of uncertainty. Profits increased substantially but net assets remained fairly with and the group achieving a modest level of free cash flow, which is nearly enough to cover the recently introduced dividend. One issue has been the softening in diamond prices during the final quarter of the year. This has been blamed on lower liquidity from the diamond banks but I suspect, as the disappointing Hong Kong jewellery show suggests, that the slow-down in the Chinese economy may be taking its toll. The board expects diamond prices to improve again in the second half of the year which coincidentally is when they expect the Ghaghoo mine to start contributing to profits. That mine, however, did provide rather disappointing figures for grade and price per carat but this should improve when production is ramped up next year.

The Letseng mine seems to be in a good shape. After the investments the breakage should be reduced going forward but the improved costs from the signing of a new contract with the equipment provider loos to be offset by increased input prices at the mine. Finally, although tensions have reduced following the elections, any further unrest in Lesotho could be a very big issue. The shares now look very cheap on P/E terms and the new dividend should underpin prices to some extent and I have decided to tentatively buy back in here.

The chart here does not look that great and the falling diamond prices seem to have taken their toll. Given the downtrend in force here I will have to watch my investment closely and apply a suitable stop loss.

On the 23rd March the group announced that The Capital Group Companies had sold about 2M shares at a value of about £2.9M. They now have 3.5% of the total share capital but this is quite a hefty sale.

On the 24th March it was revealed that the Capital Group Companies have continued selling down their holding and sold another 1.2M shares at a value of about £1.7M. They now own below 3% so we are not going to hear whether they sell the rest of their holding.

On the 31st March it was announced that two non-executive directors were retiring from the board. Dave Elzas leaves after nine years, being with the company since its listing and Richard Williams has taken up a full time executive roll in Canada after being with the company since 2008.

On the 2nd April it was announced that FMR LLC had sold 398,718 shares in the company at a value of about £560,000. After the sale they still hold 4.79% of the company’s shares so it seems another large shareholder is selling down their holding.

On the 21st May the group released an update for the year to date. During the period, diamond traders continued the cautious approach they have adopted since Q3 2014 as increased liquidity constraints following the closure of the Antwerp Diamond Bank, together with tighter credit terms imposed by other banks put pressure on the rough diamond market. Additionally traders in polished diamonds wait for improved demand that was not stoked by the recent Basel Watch and Jewellery show. The prices achieved for Letseng’s high quality stones did remain robust throughout the period, however.

During the first four months of the year the Letseng mine recovered some 31,369 carats at a grade of 1.58 cpht, this compares unfavourably to the 34,205 carats at a grade of 1.63 cpht that was achieved during the same period last year. The shortfall is mainly due to the planned 19 day shutdown of Plant 2 as the phase 1 upgrade was completed. Following this upgrade, plant 2 is operating well and is on track to achieve its target of an extra 250KT of ore processed per annum. During the period, a 314 carat type 2 white diamond was recovered and sold into a partnership arrangement, which is good to see. At the first three tenders of the year, some 35,940 carats were sold at a value of $77.1M compared to 31,614 at $67.7M during the last quarter. This means that the sales achieved $2,146 per carat compared to $2,140 per carat, although the 12 month rolling figure is $2,397 per carat which shows that the last two quarters have underperformed compared to the two before.

The coarse recovery plant remains on track for completion by the end of Q2 and is forecasted to be completed within the budget of $12.5M. All major equipment has been delivered to the site and construction is well advanced with commissioning having commenced during May. In Botswana, good progress was made on developing production area 1 on level 1 with the first long hole rings being blasted. Before these blasts, ore availability had been confined to limited areas on level 0 in the development tunnels. With more ore available, the plant has been able to treat more material with 67,330 tonnes of ore being treated during the period with 16.174 carats recovered. Following optimisation initiatives on the plant, and the increased steady state feed, the ore from the newly opened areas has yielded grades above the disappointing reserve grade with an average of 29 cpht in May so far. The mine is on track to ramp up to full production during the second half of the year as planned.

On the 30th July the group released a trading and production update covering H1 2015. During the period the overall diamond market experienced high inventory levels and continued liquidity concerns. This, combined with global macro-economic uncertainties has continued to place pressure on both rough and polished diamond prices. Letseng’s large high value stones have so far remained resilient to these pressures but the current market conditions have had a negative effect on the pricing achieved for the smaller Ghaghoo diamonds.

At Letseng, 27,547 carats were mined during Q2 which made the H1 output come in at 50,019, a 7% fall year on year. The decline was due to the plant 2 upgrade which was completed in budget and on schedule. The shutdown for the changeover occurred for 19 days which reduced the amount mined during February and March. Following the upgrade, plant 2 is operating well and is on track to achieve its increased head feed target of an additional 250,000 tonnes on an annualised basis. Although the power supply situation in Lesotho continues to be unreliable with frequent power outages, the impact on the operations at Letseng has been minimal due to the additional on-site back up power generating capacity installed last year.

During the period Letseng held four tenders, selling 46,961 carats at a value of $106.3M. The average price per carat stood at $2,264, a decline of 3% when compared to the second half of last year. During the period, 237 carats were extracted for manufacturing at a rough value of $3M with $6.9M remaining in polished inventory at the end of the period. At the mine, an outstanding quality 357 carat type iia white diamond was recovered that will be sold in Q3 and a further four diamonds over 100 carats each were sold in the period, including a top quality 108 carat type iia rough diamond which sold for over $7M!

The construction of the course recovery plat was completed on schedule and within the budget of $11.7M and commissioning continues with the first diamonds having been recovered from run of mine ore.

At Ghaghoo, 132,135 tonnes of ore was treated, sourced mainly from level 0, whilst work continued in establishing the production section on the first production level and ramping up to steady state production. After June, all ore has been sourced from level 1. Five tunnels on level 1 have now been fully developed to the northern orebody-country rock contact, with development having been started on the next two tunnels. Slot developing and opening has progressed more slowly than anticipated due to localised difficult ground conditions, but has now been completed from tunnel 1 to tunnel 5 which will allow the retreat of the production faces back along these tunnels. The slower than anticipated progress in the slot opening has constrained the production ramp-up.

Development of the decline down to level 2 progressed to a point, but was then halted just short of the same main water fissure that was intersected on level 1. Both the decline and the rim tunnel on level 1 need to advance through the fissure in order for development to continue and allow access to the second production section. Specialists have been deployed to ensure the fissure is fully sealed prior to the tunnels advancing and work is progressing slowly and carefully to avoid any further major ingress of water.

The processing plant will continue to ramp up to the capacity of 60,000 tonnes per month. In both May and June, over 32,000 tonnes of ore per month were treated, with recovered grades in excess of the modelled reserve grade of 27 cpht being consistently achieved, resulting in a total recovery of 35,283 carats in the period. During the half-year, eight diamonds larger than 10.8 carats were recovered, including a 41 carat and a 35 carat diamond. In July a 48 carat diamond was recovered, which was the largest stone found to date. There have also been a number of coloured diamonds found at the mine, although these were in the smaller sieve sizes.

The second sale of Ghaghoo commissioning production took place in July, achieving a total value of $4.9M at just $165 per carat, substantially lower than the $210 per carat achieved at the first sale, although the quality was not comparable to that sale which, together with the declining market for these goods, had a negative effect on the price achieved. It is expected that the next Ghaghoo sale will take place before the end of the year and will include a higher proportion of diamonds from the main body of the VKSE phase of the kimberlite ore.

The group has a net cash position of $49.6M at the period end with some $83.8M cash on hand.

Overall then, this is a very mixed update. Things at Letseng seem to be going quite well. These larger quality diamonds are holding their value fairly well and the group continued to find some outstanding gems at the mine. Things are not progressing so well at Ghaghoo, however, where the development of the mine is progressing slower than planned and the falling diamond prices are taking their toll on the smaller, lower quality diamonds produced there. At these prices, I am not convinced this mine is going to do that well in the short term and until the prices for these gems improve I think I will stay out of the shares for now.