Paypoint has now released its interim results for the year ending 2015.

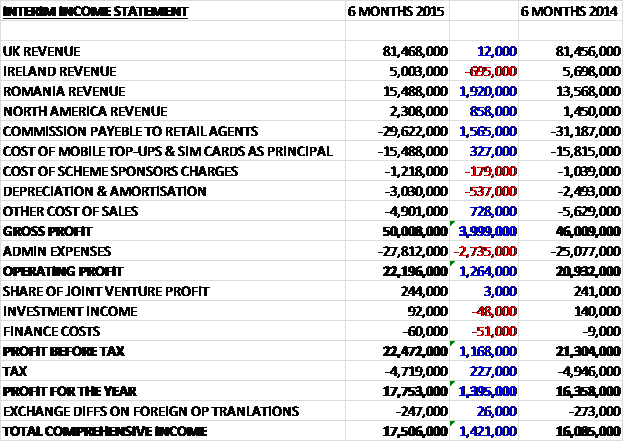

When compared to the first half of last year, revenues increased as a £695K fall in Irish sales was more than offset by a £1.9M increase in Romanian revenue and an £858K growth in North American revenue with UK sales flat year on year. The commission paid to retail agents fell by $1.6M due to lower mobile top-ups and other falls in cost of sales were counteracted by increased depreciation as a consequence of greater capital expenditure and a small growth in the cost of scheme sponsor charges, all of which gave a gross profit some £4M higher than last time. Admin expenses increased during the period, which is a situation that management expects to reverse in the second half of the year and finance costs increased slightly before a £227K reduction in tax helped give a profit for the half year of £17.8M, a growth of £1.4M when compared to the first six months of 2014.

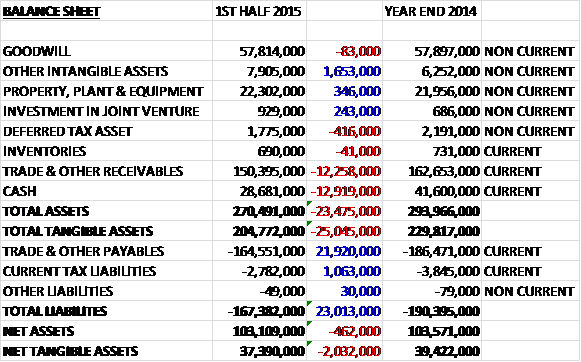

When compared to the end of last year, total assets fell by £23.5M, driven by a £12.3M fall in receivables and a £12.9M decline in cash levels, only partially offset by a £1.7M increase in intangible assets. Liabilities also fell during the period as payables declined by £21.9M and current tax liabilities declined by £1.1M. The end result is a net tangible asset level of £37.4M, a decline of £2M when compared to the end point of 2014.

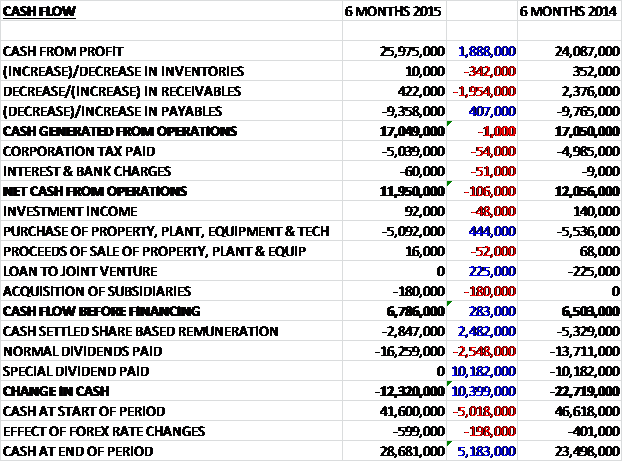

Before movements in working capital, the cash profits were £1.9M higher than in the first half of last year at £26M. This was taken down by a large decrease in payables to give cash generated from operations of £17M, flat on last time which became £12M after tax was paid. This cash was enough to pay for the £5.1M of capital expenditure, relating to IT infrastructure developments, terminals, ATMs and prepaid energy card and key readers; the £180K relating to the Adaptis acquisition that took place last year and the £2.8M in share based remuneration settled in cash which gives a free cash flow of about £4M. This was clearly not enough to pay for the £16.3M spent on dividends so that the cash outflow for the half year was £12.3M to give a cash pile of £26.7M at the half year point which was actually more than this time last year but included £3.8M relating to monies collected on behalf of clients and £7.2M in Romanian client settlement funds.

Bill and general transactions were ahead of the same period of last year as a result of a 53% increase in Romanian bill payment transactions. UK and Irish bill and general transactions were down nearly 2% year on year due to lower gas consumption because of warmer weather, which has continued into the second half of the year. The strong growth in Romania was the result of increasing market share to 19% (from 14%) and the addition of new clients, including the launch of road tax payment at the group’s sites. Net revenue grew by 6% to £25.9M as a richer transaction mix from clients was offset by a reduction in Simple Payment set up fees.

Top up transactions fell from last year as a result of the continued decline in mobile top-up volumes in the UK and Ireland, partially offset by an increase in other top-up transactions and Romanian mobile top-ups where the impact of a larger network has offset market decline. Despite this decline, net revenue increased by 4% to £11.7M due to the increase in Romania and an increase in requests for early client settlement, for which the group charges fees.

Retail service transaction volumes increased across all products except for SIM card sales. ATM transactions increased by 28%, credit and debit transactions were up 28%, money transfers increased by 52% and parcels were up 49%. A higher average ATM transaction value drove an increase in total transaction value in excess of transaction volumes. Net revenue grew by 17% to £13M driven by the increases in parcels, ATM transactions, credit and debit and income from broadband that enabled faster terminal transactions. Collect+ transactions grew substantially despite lower consumer send transactions, where there has been significant price competition which, together with an increase in logistics costs as the business moves towards dedicated use of transport, has reduced margins which resulted in profits up by just 1% to £487K.

Mobile and online transactions increased by 11% with payment transactions up 5% and parking transactions up 33%. Payment transaction growth was driven by adding new merchants and organic growth. Parking transaction growth was driven by the continued increase in consumer adoption in existing clients. There was a decline in transaction value due to a change in mix and the weakening of the US and Canadian dollars against Sterling. Net revenues were broadly flat when compared to the first half of last year at £7.4M reflecting strong growth in parking revenue offset by a decline in payment revenues due to larger merchants enjoying lower pricing.

The group have continued to add parking contracts with councils and parking authorities and the business rolled out the first phase of parking payment services in Paris during the period which will help mitigate the loss of the Westminster contract. In payments, the first sales have been achieved of two new licenses products. Cashier enables enterprise merchants to offer a customised payment experience for their online or mobile customers, hosted by Paypoint and also allows customers to store multiple cards. Cardlock reduces the complication and cost of payment card industry compliance for merchants by removing card data from their websites and apps as soon as it has been entered, and securing it remotely within Paypoint systems.

The group are combining both online and mobile under one new brand. Continued expenditure in technology, product development, sales and marketing are necessary to take the venture forward and as a consequence of this expenditure, this business is currently loss making and management expects it to remain loss making in the second half of the year. The group are also expanding into consumer applications beyond parking and the mobile app and online capability for smart meter energy payments is in an advanced stage of development and work has started on a portfolio to cover other sectors too.

As far as the network is concerned, retail sites increased by 1,157 to 36,753 with a growth of 755 in the UK and Ireland with the average retail yield per site also increasing. The number of sites offering Collect+ parcels grew by just 35 to 5,617, a number that has risen to over 5,800 sites since the end of the period. In Romania, the network increased by 402 sites during the period and the number of internet merchants fell by 205 due to the churn of smaller merchants.

Going forward the group expects the retail networks in the UK and Romania to continue to deliver profitable growth and they will continue to invest in network expansion, innovative retail technology and new services to improve retail network quality further. The integration of the mobile and online business under one brand and investment in product development is expected to unlock better growth opportunities for the group. Trading so far in the second half of the year has been in line with expectations.

Overall then, this is a fairly decent update. Profits were up but net assets declined somewhat, driven by the outflow of cash as the free cash flow doesn’t cover the value of dividends, although it seems that the business is much more cash generative in the second half of the year. Romanian bill payments seem to be expanding quickly with new clients and services being added which more than offset a small fall in UK bill payments due to the lower gas consumption during the warm winter. Top ups fell in the UK as mobile operators continue to promote contract services over prepay but the Romanian top-ups seem more resilient. Retail services are doing very well, increasing across all sectors but collect+ profits were flat as an increase in the number of transactions was offset by higher costs and more price competition. The online and mobile sector will remain loss making in the second half of the year as the group continues to invest in the division.

The shares pay a 4.4% dividend yield over the year which seems like a decent amount and the medium term story here looks exciting so I think I might look for a sensible entry point and invest here.

On the 29th January the group released an interim management statement covering Q3. Overall transactions processed increased by 5% quarter on quarter to 217M. Revenues of £58M were up 2% and net revenues of £32M increased by 4% with continued strong growth in retail services offset by declines in top-ups and Mobile & Online with Bill and general net revenue being slightly higher than last year as Romanian bill payments continued to grow strongly. UK energy payments were held back, despite further growth in prepayment meters and increased market share as utilities reported significantly reduced gas consumption. UK and Irish bill and general transactions were up 1% on last year and Retail services transactions grew substantially, up 29% on last year. Mobile top-ups continued to decrease but the fall was mitigated by an increase in other top-ups and UK and Irish retail sites increased by 295 to 28,292.

In Romania, profitable growth continued and the group processed 13.8M bill payments in the period, an increase of 27% with terminal numbers increasing by 268 sites in the quarter to 9,024 with new clients added. Collect+ volumes grew by 37% to over 5.8M transactions in the quarter and a record number during the Christmas week. The network also continued to expand, with an extra 205 sites added. Mobile and Online transactions increased by 9% to 36.5M with parking transactions up 17% to 9.6M despite the loss of the Westminster contract, and online transactions up 7% to 26.9M. Progress in the aggregation of the business continued but net revenues were lower than in the same quarter last year. At the end of the quarter, net cash was £28M compared to £25M at the end of H1 despite the payment of the interim dividend of £8.4M.

After the end of the quarter, HMRC issued a ruling rendering some services partially exempt for VAT which at current business levels, would cost the group between £1M and £2M in annual irrecoverable VAT. Going forward, the group expects to deliver results for the full year within the range of market expectations despite the lower than expected energy volumes in Q3.

A look at the chart reveals that not is not the time to invest here and I will be looking for prices to stabilise before I take the plunge.

On the 2nd April it was announced that non-executive director Eric Anstee will stand down at the next AGM after spending seven years at the company.

On the 8th April it was announced that Invesco had sold 1,480,615 shares at an approximate value of £12.6M to give them 13.76% of the total equity of the company. This is a big sale but they are still heavily invested in PAY.

On the 8th April it was announced that Mawer Investment Management had purchased 1,194,103 shares in the company at a value of about £10M to give them a 5.77% stake in the company – it looks like they might have taken some of Invesco’s shares off their hands.

On the 8th May the group announced that Warren Tucker decided to step down as Chairman and he will be replaced by Nick Wiles who has served on the group’s board for over five years.