Photo-Me has now released its interim results for the year ending 2017.

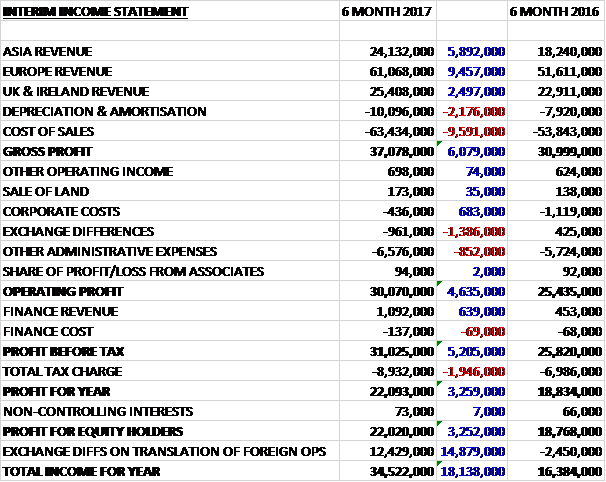

Revenues increased when compared to the first half of last year, mainly as a result of currency movements, with a £9.5M growth in European revenue, a £5.9M increase in Asian revenue and a £2.5M growth in UK & Ireland revenue. Depreciation was up £2.2M and other cost of sales increased by £9.6M to give a gross profit £6.1M above that of last time. Corporate costs reduced by £683K but there was a £1.4M negative shift due to forex movements and other admin expenses were up £852K so that the operating profit increased by £4.6M. The group also increased finance revenue by £639K but tax charges were up £1.9M to give a profit for the period of £22M, a growth of £3.3M year on year.

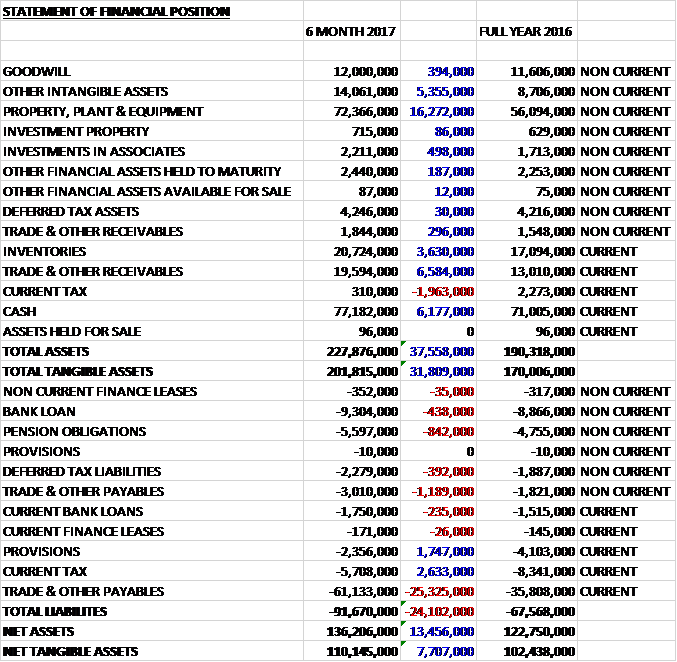

When compared to the end point of last year, total assets increased by £37.6M driven by a £16.3M growth in property, plant and equipment, at least partially related to forex movements; a £6.6M increase in receivables, a £6.2M growth in cash, a £5.4M increase in intangible assets and a £3.6M growth in inventories, partially offset by a £2M fall in current tax assets. Total liabilities also increased during the period as a £26.5M growth in payables was only partially offset by a £2.6M decline in current tax liabilities and a £1.7M fall in provisions. The end result was a net tangible asset level of £110.1M, a growth of £7.7M over the past six months.

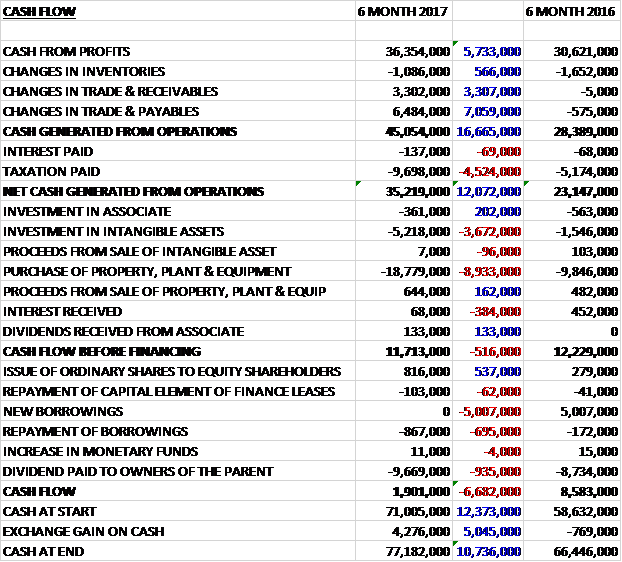

Before movements in working capital, cash profits increased by £5.7M to £36.4M. There was a cash inflow from working capital compared to a small outflow last time but tax payments increased by £4.5M to give a net cash from operations of £35.2M, a growth of £12.1M year on year. The group spent £18.8M on property, plant and equipment, along with £5.2M on intangible assets to give a free cash flow of £11.7M. Of this, £9.7M was spent on dividends which meant that the cash flow for the period was £1.9M and the cash level at the period-end stood at £77.2M.

The operating profit in the Asia business was £3.8M, a growth of £292K year on year. Japan, the largest territory in the region, was weaker in comparison with a strong first half of last year. This was primarily due to the delay to the My Number Programme, the new ID card system, and the group currently considers it prudent not to expect any contribution from this programme in the current year. Photobooth numbers have increased by some 7% in preparation for the launch of the programme which is expected to recommence at some stage in 2017. Good progress continues to be made in China where both revenues and profits increased by over 30% on a constant currency basis.

The operating profit in the European business was £22M, an increase of £4.4M when compared to the first half of last year with a 6.8% rise on constant currency basis, driven by the laundry division. The group took the decision this year to slow down the roll-out of the European photobooth estate in order to focus on upgrading its booths in terms of payments systems as well as new digital security features, particularly in France. In February they announced that they had obtained the first agreement with ANTS to allow the delivery of a digitised e-photo and e-signature for the purposes of driving licence applications enabling these documents to be sent from the booths via a secure server. They have invested in the upgrade of all their 7,800 units in France.

They have taken a cautious attitude to price increases in the photobooth estate in recent years, but increases from €5 to €6 in Holland and from CHF8 to CHF10 in Switzerland were implemented towards the end of the period.

The roll-out of the laundry product, predominantly using the same sites as the photobooth estate, continues to progress well and the group now has laundry operated units in ten countries. At the end of the half-year, across the group, the total number of laundry operated units increased by 51%. The results from the units in operation in France, Ireland and Portugal remain encouraging with monthly sales per unit of the more machines of €1,400 during the period. In the first half, laundry business takings increased by 79% to £9.9M.

The group now also has 34 laundrettes in towns across France, Belgium and Spain, and is targeting towns where there is no large supermarket nearby and limited competition. A new design for the shops has been created and it is now being rolled out starting with new locations. Results from these launderettes are solid. The ambition remains to expand this concept rapidly and reach a sizeable base of locations by 2020. Total sales of laundry equipment across the group increased by 77% to £2.3M.

Production of the Revolution 2 unit has recently started. Like the current units, it comprises two machines and a dryer but it has a footprint half the size of the current model. This smaller unit is expected to enable more rapid deployment for the product in its core markets and is likely to be more attractive in Far Eastern markets.

The group operates nearly 5,000 digital printing kiosks in Europe, mostly in France and Switzerland, an increase of 3.5% year on year. In response to growing consumer demand, they last year introduced a new kiosk designed by Starck which is fully integrated with major social media networks and enable easy photo printing from smartphones. Initial results from the Speedlab Cube and Speedlab Bio have been promising and these have been gradually rolled out during the first half.

The operating profit in the UK & Ireland business was £4.7M, a decline of £736K when compared to the first half of 2016 due to the acquired Asda photo division start-up costs, increased depreciation and slightly higher machine management costs in the core photo booth estate. The laundry business in Ireland continued to perform well and Fowler, the commercial laundry and catering equipment business acquired last year made good progress and contributed nearly £2M of revenue in the period.

Photobooth unit numbers were stable year on year and there was a continued reduction in the amusement machines and kids rides which generate minimal revenue and perform below group profitability standards due to increasing maintenance costs. They more than doubled the number of digital printing kiosks, however, by replacing 265 existing units in Morrisons with their own units.

Leveraging the secure technology developed for the ANTS solution, photobooths are being rolled out in Ireland in conjunction with the Ministry of Foreign Affairs and Trade in order to enable secure online passport applications. Initial results and testing have been very positive and in November, a memorandum of understanding was concluded between both parties sealing the five year arrangement.

In October the group acquired the photo division of Asda for a total consideration of £3.8M, of which £2.3M was deferred. They have already started the reconfiguration of layouts and equipment upgrades that are necessary to increase the appeal for customers and expand the profit going forward.

In addition to ID secure systems, the group has developed solutions for the transmission of secure payments and the automated distribution of high-value prepaid gift cards.

The group’s performance for the first half was ahead of board expectations, aided by favourable currency movements. The board now expect the group’s profits will significantly exceed current market expectations for the year as a whole.

At the current share price the shares are trading on a PE ratio of 21.3 which reduces to 17.9 on the full year consensus forecast. At the period-end the group had a net cash position of £68M compared to £62.4M at the year-end. Given this, I still don’t understand why the group feels the need to take out a loan. After the interim dividend was increased by 20% and a special dividend was paid during the year, the shares are yielding 5.6% which falls back to 4.2% on the full year forecast, presumably as the special dividend is not expected to be repeated.

Overall then this has been a decent half year for the group. Profits are up, along with net assets and the operating cash flow, although how much of this is due to favourable currency movements I am not sure. The performance in Asia has been OK but the delays to the Japanese ID cards are disappointing. Europe seems to be performing well with the laundry units starting to contribute but the UK saw a decline in profits due to higher photo booth costs and start-up costs related to Asda Photo.

The French digitised e-photo project looks like a good template for further similar schemes and the full year results are expected to be above expectations, again likely predominantly due to favourable forex movements. The forward PE of 17.9 doesn’t look great value but there is a lot of net cash on the balance sheet (assuming it is all really there – always a concern of mine when cash rich companies take out new loans) and the dividend yield of 4.2% is worth having. I am happy to hold here.

On the 23rd the group released a statement following the announcement that UK authorities would accept mobile phone photos for ID pictures. They confirmed they had continued to trade in line with their expectations since the interim results. They believe their latest technology represents a major growth opportunity as the most secure photo ID solutions available and that accepting photos from mobile phones for official documents is incompatible with developing security requirements.

Their solutions have been adopted in France as well as in Ireland where trials are underway for photobooth secure online passport applications. Furthermore it is currently in ongoing discussions with HM passport office in order to equip its photobooths in the UK with the technology used in France.

I have mixed feelings about this. Clearly this is not a good development as it will be much easier to use digital photos now. It seems unlikely to affect the group in the near term but longer term it could be an issue. I will not panic yet but this is not quite as strong a hold as it once was for me.

On the 7th March the group announced the sale of their head office for a consideration of £2.5M. The book value of the land being sold is £100K so there will be a profit on sale of £2.4M. The disposal is part of the group’s review of its property portfolio in order to group the activities of the head office and UK operations into one location.

On the 30th March the group announced that it was launching a rollout of their encrypted photo ID technology across Ireland in partnership with the Irish Government. The launch will see their secure digital upload system rolled out to over 150 photobooths, growing to 300 throughout the country by the end of 2017.

On the 2nd June the group released a trading update covering the whole year. The photo ID and laundry business continued to perform well. In France the vast majority of photo booths have been upgraded for ANTS to enable direct transmission of ID photos and data to the government database. In Ireland, the group’s encrypted photo ID upload technology, launched in partnership with the Irish Government for the new online passport application service, will be rolled out to 300 secure digital upload enabled photo booths by the end of 2017. They have now also started the roll out of the ANTS booths in Germany.

The expansion of the laundry business in Europe has continued with consistent expansion of estate owned and operated laundry units in operation, primarily located in France, Ireland, Belgium and Portugal. During the second half of the year they started deploying the Revolution laundry units in the UK with some 100 units now deployed. The first laundry shop opened in Japan in the last quarter and is proving to be successful. The board expects the year as a whole to be in line with market expectations with profits up about 20% compared to the prior year.