Keller has now released its interim results for the year ending 2016.

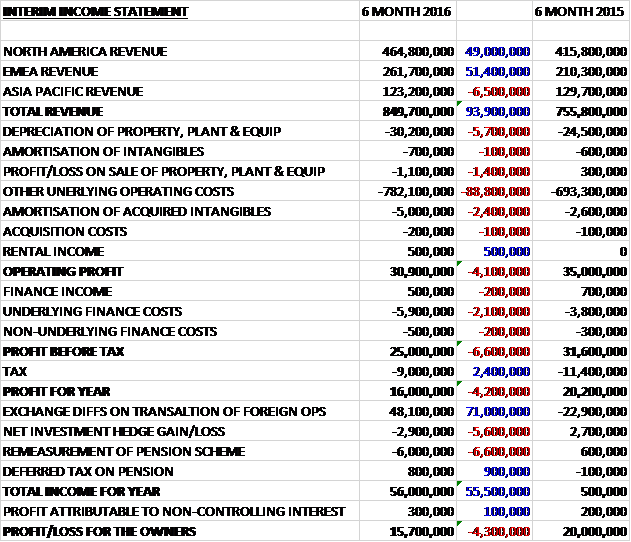

Revenues increased when compared to the first half of last year as a £6.5M reduction in Asia Pacific revenue was more than offset by a £49M growth in North America revenue and a £51.4M increase in EMEA revenue. Depreciation was up £5.7M, there was a £1.4M detrimental swing to a loss on the sale of fixed assets, and other underlying operating costs increased by £88.8M. We also see a £2.4M increase in the amortisation of acquired intangibles to give an operating profit £4.1M below that of last time. Finance costs increased by £2.5M but tax charges were down £2.4M which meant that the profit for the period came in at £15.7M, a decline of £4.3M year on year.

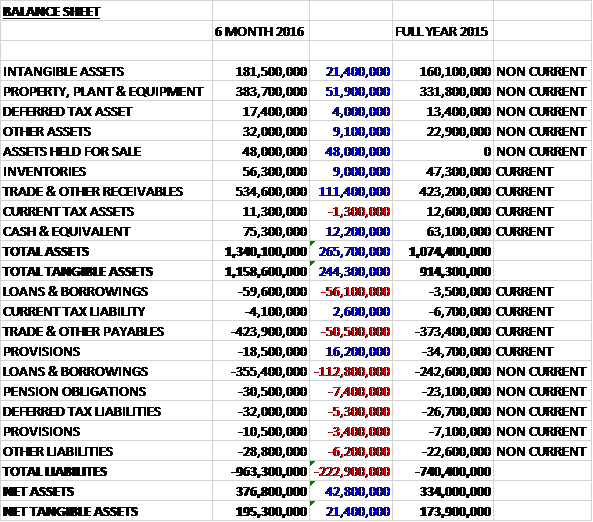

When compared to the end point of last year, total assets increased by £265.7M driven by a £111.4M growth in receivables, a £51.9M increase in property, plant & equipment, a £48M growth in assets held for sale, a £21.4M increase in intangible assets and a £12.2M growth in cash. Total liabilities also increased during the period as a £168.9M increase in borrowings and a £50.5M growth in payables was partially offset by a £12.8M decline in provisions. The end result was a net tangible asset level of £195.3M, a growth of £21.4M over the last six months.

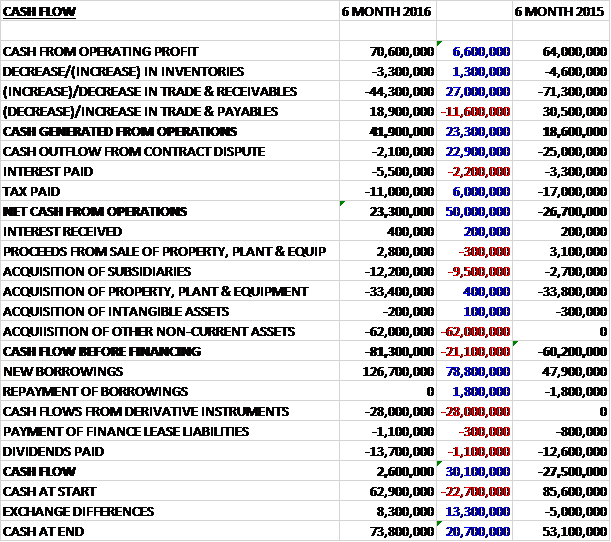

Before movements in working capital, cash profits increased by £6.6M to £70.6M. There was a cash outflow from working capital but this was less than last time due to a lower increase in receivables and after a £2.2M increase in interest payments was offset by a £6M decline in tax charges and a £22.9M reduction in cash outflows from the contract dispute, the net cash from operations came in at £23.3M, a positive movement of £50M year on year. The group spent £33.4M on fixed tangible assets and £12.2M on acquisitions but we also see £62M spent on other non-current assets relating to the freehold purchased in Bristol which meant that there was a cash outflow of £81.3M before financing. On top of this there was a £28M cash outflow from derivative instruments (I am not exactly sure what that relates to) and £13.7M spent on dividends which meant the group had to take out £126.7M of new loans to give a cash flow for the period of £2.6M and a cash level at the end of the half year of £73.8M.

The operating profit in the North American division was £33.6M, a growth of £5.2M year on year helped by the ongoing steady growth in US construction and beneficial currency movements. Bidding activity remains robust across the country and the group’s contract awards in the period were above the same period last year with the US order book at the period-end some 10% higher.

Howard Baker had a good first half across most sectors. Case and HJ Foundation also performed well, although HJ’s core Miami market is slowing after a very strong couple of years. Bencor has integrated well and is currently helping a number of group businesses outside the US in bidding D-wall work. Its $135M East Branch Dam job is on track and the business is just completing work on two major station boxes in San Francisco. Suncoast, which is mainly focused on residential construction, had an excellent first half, taking full advantage of the ongoing increase in housing starts. Whilst housing permits as a whole have flattened in recent months, those for single family homes which generate most of the business’ revenue continued to increase.

The Canadian business is operating in a very difficult market. It made a small loss in the seasonally weak first half, not helped by the delayed start of its major subway contract in Toronto. This $42M job was originally due to begin in April but is now not expected to start until November. Results will improve in the second half as revenues pick up, operating conditions ease and the business benefits from cost reductions made in the first half.

The operating profit in the EMEA division was £13.6M, an increase of £6.6M when compared to the first half of last year. Whilst a number of markets remain challenging, the group’s most significant European businesses in the UK, Germany, Austria and Poland have all had a good period and all of them enter the second half with strong order books and good prospects although the UK may be adversely impacted by a Brexit-related slowdown in Q4.

Elsewhere, the group made good progress on the major contract in the Caspian region. They have recently been awarded further work on this contract and expect more to be awarded in the second half which would extend the job well into 2017. Whilst some projects have been delayed in the Middle East as a result of the low oil price, construction activity has not abated and the order book is healthy. The market continues to slow in South Africa but there remain good opportunities in sub-Saharan Africa.

The operating loss in the Asia Pacific division was £9.6M, a detrimental movement of £14.4M when compared to the first half of 2015 with a very difficult period being driven by market conditions and project delays. About two thirds of the decline occurred in Australia, due in a large part to the non-recurrence of Wheatstone profits. The Asia and Australia divisions have been combined which has realised £3M of annualised cost savings through the rationalisation and the group expect to deliver a further £3M in operational efficiencies over the next year.

In Australia, dollar revenue was 28% down, in part due to delays to the start dates of the two largest projects and the business made a loss of around £6M as a result of the volume reduction and the deterioration of the pricing environment. In Asia, revenue was broadly flat but the Asian operations also recorded a loss in the period, largely as a result of the piling business in Singapore which suffered from very low volumes and some one-off costs relating to prior years. It is being restructured under a new management team.

Elsewhere in Asia, the large ground improvement contract at Changi airport has performed well and the Indian business had a good first half after a slow start to the year. Looking forward, despite the cancellation of the major Pluit City contract in Indonesia, which was due to start in September, the division’s order book is 10% ahead of the same period last year and revenue will improve significantly in the second half, particularly in Australia as its major projects pick up speed. The board expect the division to return to profitability in the second half of the year.

In February the group acquired Tecnogeo, a Brazilian business, for an initial cash consideration of £11.8M and contingent consideration of up to £12.3M, only £500K of which is currently provided for. In the period since the acquisition the business generated profit of £100K and the transaction generated goodwill of £5.4M. In April the group acquired Smithsbridge, a marine construction business based in Brisbane, for an initial cash consideration of £1.8M which reflects the fair value of net assets acquired. Early integration of both businesses is proceeding well, although the market in Brazil is currently tough.

In May the group acquired the freehold of a processing and warehouse facility in Bristol for a consideration of £62M. The group’s final liability with regards the historic contract dispute involving the property is in part dependent on the value of the property after some remedial works. In order to maximise its value, the group decided to acquire the property with a view to marketing it to third parties. During the period, £500K of exceptional income was received relating to rent at the property. This was offset by £500K of finance costs incurred to fund the acquisition.

Roy Franklin retired as Chairman in July after being in the role for seven years and was replaced by Peter Hill.

The UK Brexit vote is expected to lead to a period of prolonged economic and political uncertainty in the country. Whilst this is likely to impact the group’s operations in the UK, this business represents less than 4% of group revenue. Since the vote, Sterling has weakened considerably against most currencies. Most of the group’s earnings and all of its debt are in foreign currencies, mostly the US dollar. As a result, should sterling weakness persist, there will be a beneficial effect on the group’s profits but has increased the reported level of their net debt by nearly £40M since the end of the year.

Whilst conditions in a number of markets remain difficult, the US and most of the major European markets are healthy. On a constant currency basis, the order book for work to be undertaken over the coming year at the end of June was up 10% year on year. For 2016 as a whole, the board expects the underlying combined performance of the two largest divisions to outperform its original expectation. Asia Pacific has had a very difficult period but they expect it to return to profitability in the second half of the year but overall they expect the full year results to be at the lower end of board expectations.

At the current share price the shares trade on a PE ratio of 11.1 which falls to 9.3 on the full year consensus forecast. At the period-end, net debt stood at £339.7M compared to £183M at the start of the year. After a 5% increase in the interim dividend, the shares are currently yielding 3.1% which increases to 3.3% on the full year forecast.

Overall then this was a mixed period for the group. Profits were down but net assets increased. The operating cash flow also grew but the group was unable to make any free cash and there was a cash outflow before financing, not to mention the big loss from derivatives. The performance in North America and EMEA was good, benefiting from a strong US construction market and a good performance from the core European markets.

The performance of the group has been dragged down by the Asia Pacific businesses, however, which made a big loss in the period. This was mainly due to the Australian business which continues to struggle, suffering from delays to projects and strong competition driving down prices. The other poor performer was the Singapore piling business which suffered from low volumes, although the board do state that they expect the Asia Pacific performance to improve in the second half.

The other concern is the ongoing contract dispute which has now resulted in the group actually acquiring the warehouse building at the centre of the row! The profit for the year is likely to come in at the lower end of expectations but with a forward PE of 9.3 and dividend yield of 3.3% this is now priced in. I am tempted to re-enter here but it is not without risk and I am starting to get a little concerned over the ballooning debt and lack of free cash flow.

On the 9th August the group announced it had been awarded a major contract in Abu Dhabi. The work comprises ground improvement works and will be conducted in a 50/50 consortium. The total contract is valued at around £50M and the work is expected to start imminently to be completed by Q3 2017.

On the 11th October the group announced that it had been awarded a major contract in Egypt. The contract for ground improvement works forms part of the development by the Egyptian Government of the eastern shore of Port Said along the newly created navigation channels of the Suez Canal. The contract is for a value of around £60M with work expected to start imminently and to be completed by Q3 2017. This is the group’s second recent major award following the £50M contract in Abu Dhabi announced in August.

On the 20th October the group released a trading update covering Q3. The two largest divisions, North America and EMEA, have delivered steady results. In particular, trading in the US and Europe remained strong with expectations for the full year unchanged. Elsewhere the results were somewhat disappointing, notably in Canada and Africa where market conditions remain depressed and they have undertaken further restructuring.

In Asia Pacific, the continuation of the very difficult market conditions in the main markets has meant that the division incurred further operating losses in the quarter. They continue to experience some contract softness and the pricing environment remains challenging. The recovery in this division is likely to be more gradual than previously thought and it is expected to record a loss for H2, albeit with an improving trend in its performance.

As a result, the board now expects full year results to be around 15% below current market expectations, mainly due to the underperformance in Asia Pacific. In addition, second half results will include an exceptional restructuring charge in connection with further downsizing actions which is expected to be around £10M, much of which is non-cash. More positively, the quarter has seen a good order intake and like for like order book work for the next year is at an all-time high and 15% above that of last year. Looking further ahead, the strength of the order book and steadily growing construction markets in the US and Europe, together with actions already taken, mean that the group is well placed for 2017.

Things are certainly tough here and I am not rushing in just yet.

On the 22nd November the group announced that it had been awarded a major ground improvement contract in Durban, South Africa with the total contract being valued at over £40M. They will design and construct the complete ground improvement solution for over 350,000 square metres of warehouses and ancillary offices as part of the Clairwood Logistics Park development situated at the old Clairwood racecourse in Durban. The work will be executed over the next three years.

On the 9th December the group announced that Chairman Peter Hill acquired 6,000 shares at a value of £48K; CEO Alain Michaelis acquired 13,500 shares at a value of £107K; and Finance Director James Hind purchased 12,500 shares at a value of £99K. This is strong buying and I think I might go in for a few too.